Trending Assets

Top investors this month

Trending Assets

Top investors this month

$12.9MFollowers

Buy The Dip On This Chip Stock- $AMD (Entry for July Idea Competition)

I've written about $AMD previously here, but as the pitching competition came about, I thought I'd flesh out this idea into a fuller thesis.

Motivation

While I hold positions in several tech stocks, recent market moves have resulted in a prominent dip in AMD along with all semiconductor stocks on the waning of anticipated macro demand and a probable recession. This dip is a buying opportunity, one that I believe would lead the stock to reverse course in the next 12 months as AMD's fundamentals prove to hold strong amidst a weak macro environment. To put it simply, I believe the market has mistaken AMD's core fundamental drivers as those tied to the broader macro environment. They're tied to market share gains instead.

I've been long $AMD for years now, but I see the price as an opportunity to accumulate.

An Introduction to $AMD

Source: Unsplash, Public Domain

For those who're not aware of the semiconductors world, AMD (Advanced Micro Devices) makes microprocessors (chips), more specifically CPUs or Central Processing Units. These CPUs are built on a common architecture that's been standardised for decades - the "x86" architecture. It's the same one being used in most laptops and PCs right now. These architectures are also used in data centres, servers, gaming consoles, and a whole load of other places. Today, Intel and AMD are the only two notable players that design chips for this architecture. Intel both designs and manufactures most of its chips. AMD, however, only designs their chips but gets them manufactured from other companies before selling them to customers. This "design only" model is called "fabless". The "fab" (or fabrication) here is carried out by third-party manufacturers, most prominently Taiwan Semiconductor Manufacturing ($TSM), that focuses on pushing the bounds and output of manufacturing technology with a dedicated focus. As a neutral manufacturer, they hold contracts from global chip designers - Apple ($AAPL), Qualcomm ($QCOM), AMD, Nvidia ($NVDA), Marvell ($MRVL), etc.

AMD also sells GPUs (graphics processing units) and recently bought out Xilinx, a maker of field-programmable chips. That said, the core business and financials are still dominated by CPUs so that's what we'll focus on.

AMD By The Numbers

Last Twelve Month (LTM) Figures:

- Revenues of $18.9B

- Revenue growth of 65.6% YoY, >50% YoY in organic growth

- Gross Margin of ~50%

- Net Income of $3.4B, at an 18% margin

- Free Cash Flow (FCF) of $3.3B, at $17.4% margin

- Guided growth of 60% YoY for FY22 (current year)

Other Metrics

- Enterprise Value (EV) of $127B

- Market Cap of $131B

- 52-week High-Low of $162-$73

Source: Data from Koyfin, AMD Investor Relations

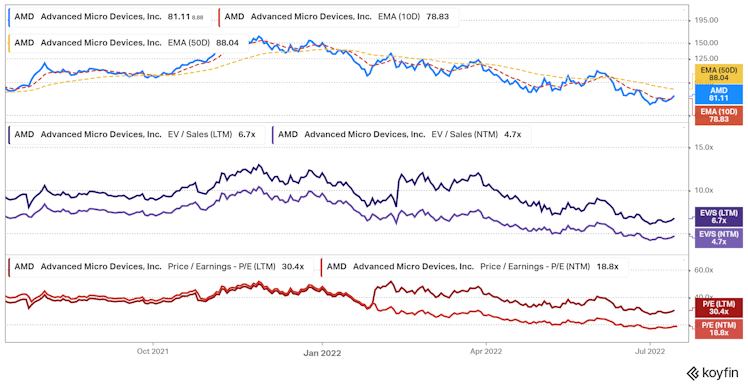

Over the last two years, sales and margins have been on an expansionary trend. The following chart shows price action and common valuation multiples:

Source: Koyfin

AMD vs Intel; The Evolution Of The x86 Game

Compute power demand is on a secular trend up. The cloud, automotive, AI/ML, big data... etc. More computing power is needed now than ever before across various global factions, and microprocessor manufacturers such as AMD have benefitted as the guys that build the chips that execute all those computations.

At the competitive x86 level, there have been some very different market dynamics. AMD has won on account of the excellent business execution by way of superior chip performance - notably the performance/watt and performance/price they have on hand. The product portfolio performs relatively very well compared to previous AMD iterations and Intel's current lineup. This wasn't the case a few years ago when Intel could build outright superior chips, especially in the high-end where margins are fat. Intel, over the past few years, has still done alright but has faltered on its manufacturing technology that has not been keeping pace with Taiwan Semi. While Intel was the undisputed king in 2016, AMD has been eating into the market meaningfully over the past 2-3 years.

To add to complications at Intel, the company has seen two CEOs resign - one in 2018, and another in 2021. The latter served as CFO before CEO and didn't offer a technical background. The current CEO Pat Gelsinger (technical, and ex-CEO of VMWare) has put forth a turnaround strategy for re-vitalizing in-house Intel manufacturing. He also happened to work previously at Intel, under the legendary CEO Andy Grove, serving once as CTO. On paper, he looks like the right man for the job. That said, large ships take long to steer a new course, and new factories are expected to come into fruition later rather than sooner. Meanwhile, AMD has been taking market share and winning with growth in sales and profits.

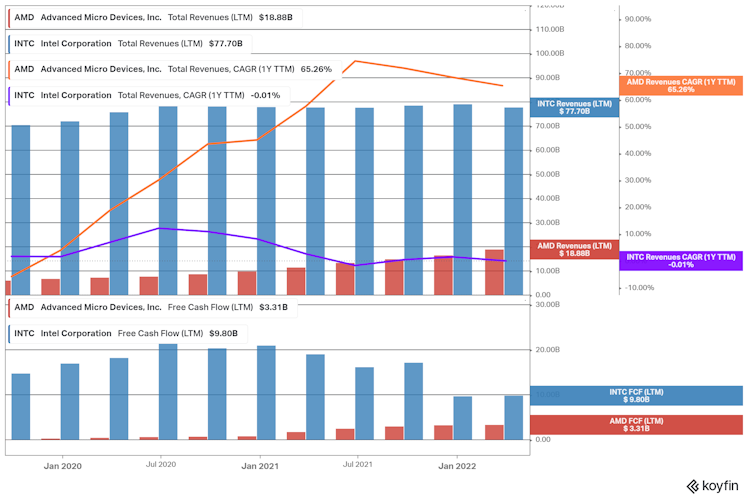

The following graph shows the changes in revenues and Free Cash Flow of the two businesses across the past 10 quarters.

Source: Koyfin

The above graph aggregates the Last Twelve Months' data every quarter for Revenues, Revenue Growth, and Free Cash Flow for both stocks.

- Intel Revenues have been stagnant, slightly declining on an LTM basis, while AMD has recorded high growth at 65% YoY, still about 50%+ excluding the Xilinx acquisition

- Intel's FCF margins have relatively declined, while AMD's have increased. This marks the shift in pricing power from Intel to AMD, which has been exercising its moat built on tech excellence, especially in the high-end product range where margins are strong.

- In the scheme of things, Intel remains a giant, while AMD is still small but growing fast and taking share.

Market Share Gains & The Long-Term Opportunity

From just the above financials, it is obvious to state that AMD has been eating into the Intel pie, building pricing power with a strong product portfolio and competent business execution. Some of it was helped by Intel's lack of sufficient innovation in recent times. But to AMD's credit, Lisa Su, the current AMD CEO, is responsible for turning the company around from a $2 share stock in 2016 facing bankruptcy to a now virtually debt-free enterprise going toe to toe with Intel. She remains at the helm, with an ambitious strategy and a phenomenal operating track record.

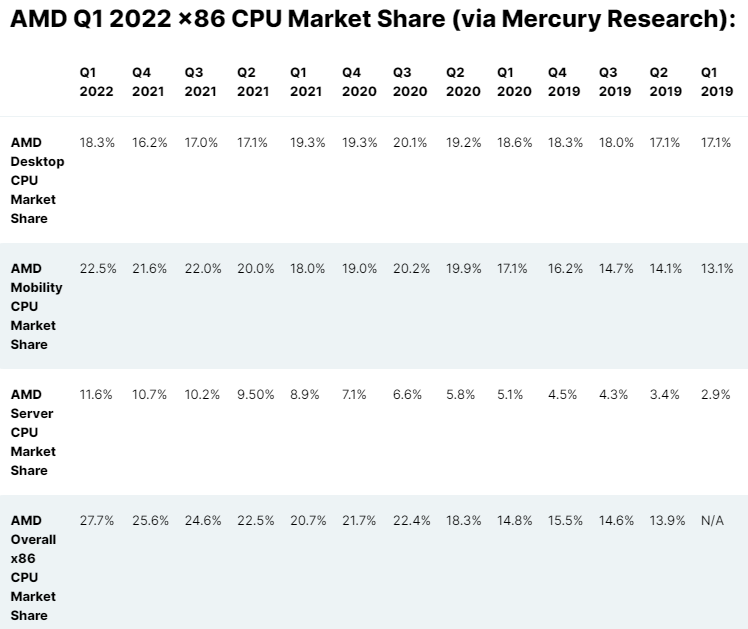

For more granular data on CPU gains, the third-party Mercury Research illustrates the recent share gains in x86. Assume the rest is controlled by Intel as other players are virtually negligible.

Source: WCCF Tech, Mercury Research

AMD has roughly doubled its market share in the x86 market since mid-2019 across the board. It still, however, remains a tiny business on financials compared to the giant Intel, which holds the rest. If one assumes an extrapolated trajectory, there's a lot more business to come, against a huge addressable market.

Up until now, I have three key inferences from the above information:

- A large proportion of fundamental growth for AMD is attributable to market share gains, more so than the macro environment and the recent Xilinx acquisition

- AMD, should it execute, is on a trajectory for substantially more market capture against a long growth runway (+ going beyond the x86 architecture with Xilinx into new markets)

- AMD has particularly grown fast in the Server and Data-center CPU markets, which were historically Intel's stronghold territory and offer an enormous growth opportunity (see below)

Source: AMD Investor Presentation

Supply/Demand/Macro Forces

Demand has been strong in recent quarters. Supply has kept up. All commentary in recent earnings points to AMD being relatively supply constrained. So why is that the case?

Microprocessors are hard items and are extremely complicated to manufacture. Companies like TSM have to invest billions to build the technology, push through CapEx, and make the machines that can fabricate these chips. Very techy stuff; they're trying to find a way to print more transistors, nanometers apart, on silicon wafers in increasingly dense configurations. So when a superior chip comes about like AMD's, it takes time to launch up and allocate capacity even if sudden demand is there. Supply chains on the semiconductor side are rather inelastic due to the complexity involved in ramping and changing production. And AMD, going by its several earnings transcripts, has been supply constrained after its products turned thoroughly competitive against Intel in 2019. The company allocated over $1B in investments to secure and ramp up capacity in 2021, expanding with their demand trajectory that was exploding onto the scene.

Taiwan Semis, on the manufacturing end, has also struggled to keep up with the EV auto revolution, accelerated digital transformation, big data, AI etc. during and post COVID. Those in tech would know how rapid the financials of several internet and software companies were launched upwards during COVID. All of it required chips and computing power. This is a theme that persists in 2022. The semi shortage was more prominent in 2021, though the supply chain has relatively worked itself out to improve and meet demand since then. Along with these trends, so has AMD. Enterprise verticals have accelerated their purchases of AMD only recently in 2021 and the data centre applications have doubled YoY.

Given this information and the parts above on market share gains, there seems to be a prominent disconnect between macro forces, and AMD's individual financial drivers.

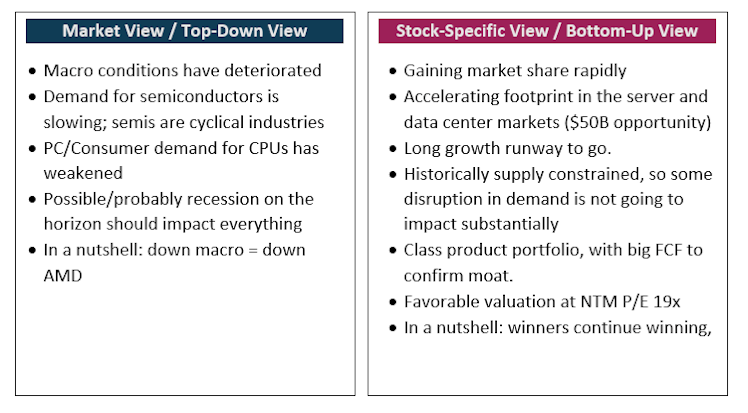

What does Mr Market think vs. What I Think - Why BUY the DIP NOW?

Source: Author, Summary of opposing views

The broad conversations surrounding the semiconductor industry are of anticipated weakening demand, particularly in the consumer-heavy Personal Computing market. This was signalled by Micron's earnings earlier this month which came in weak and led to a market-wide selloff in semiconductors on an anticipated recession.

In the case of AMD, this is where I would disagree. The tough macro is a first-order effect. The second order effect here is that while macro demand fades, the supply-constrained AMD ought to continue to meet its still growing demand, particularly in the data-centre, server, and all-around enterprise market. Furthermore, the specific machines in TSM that make AMD chips are often shared with other contracts from other clients vying for capacity. Should those other contracts be hit by a tough macro, AMD could seek excess capacity and favourable terms with TSM.

All this comes to sales drivers though. AMD's story has been driven predominantly by market share gains. If a $100B opportunity contracts by 10-15% in the next year, AMD might see some weakness but it should logically continue to gain market share, thereby growing revenues too. This is an apt extension of the trends we've seen in the Intel vs AMD sales chart above.

Data centre and servers, and the enterprise faction of AMD's client portfolio, has only gained momentum in recent times. The end opportunity remains multiples higher. Only 11% share in the server market especially leaves so much more room to grow.

So at the moment, with the current valuation of Next Twelve Month P/E of 18.8x, AMD is ripe for purchase, in my opinion as a contrarian position. The valuation offers sufficient risk/reward, that it's worth buying the dip at this price. With recent macro fears, I also posit that the above thesis may not be commonly shared in the semiconductor investment community and it would be worth betting on before August 2nd on Q2 earnings should the bull thesis strengthen. Great opportunities whisper, they don't yell out.

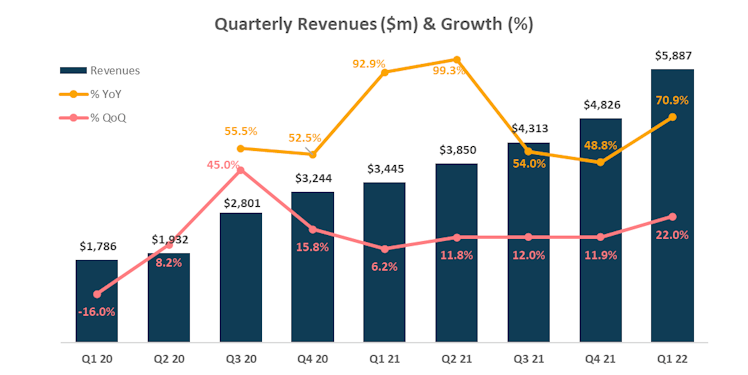

Strong Financials: A Combination Of High Growth and Profitability

Source: Author, using data from AMD's Quarterly Results

Growth rates have been high throughout the past several quarters. The Xilinx acquisition boosted Q1 growth inorganically, but AMD confirmed 50%+ YoY growth ex-acquisition financials on an organic basis. This means that the core business of CPUs remains in high growth mode, showing acceleration. Management expects 60% YoY growth for FY22, which implies further sequential growth in the coming two quarters.

Since the total x86 market is pegged to grow at ~10% based on various sources, most of AMD's growth is driven by market share acquisition.

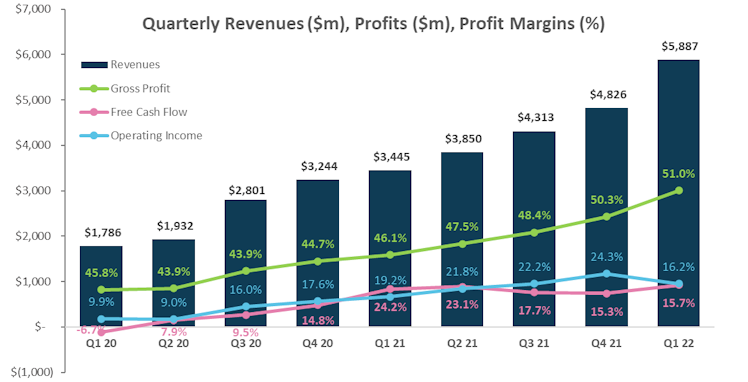

Source: Author, using data from AMD's Quarterly Results

As market share has been gained, AMD has been able to take higher margins, beginning in 2021 with enterprise applications, data centres, and servers recording high sales of the top-end chips. Economies of scale have helped AMD record improving gross margins too. Post-acquisition, operating margins have dipped slightly. This is not surprising as acquisition expenses were included that won't repeat again. The merged entity of AMD and XLNX should begin recording synergies in the upcoming quarters and years. In summation, these are robust financials. On the balance sheet, AMD has $6B in liquidity and $1.4B in long-term debt. In the scheme of the financials, the enterprise is practically debt free.

Cheap Valuation & A Track Record Of Earnings Outperformance

Source: Koyfin

The recent dip here was from $108 to $73. While we've seen some partial recovery, I reckon there's a lot more to go. Consensus analyst estimates, after factoring in the guided 60% YoY growth for FY22, indicate a P/E of 18.8x on a next twelve-month basis.

For a technology leader with its current growth and existing margins, the forward multiple is very reasonable if not outright cheap. Should my thesis of sustained business execution play out, and AMD's view in the market is strengthened against its long-growth runway of a $100B+ TAM, then we're in for a large upside. I believe a more appropriate exit multiple in twelve months would be 28x P/E with a growth run-rate of 20%+ YoY on sales by mid-2023.

In other words, I expect a 48% 12-month return toward my conservative fair value target. With beats and excess multiple compression, potential IRR would move higher up.

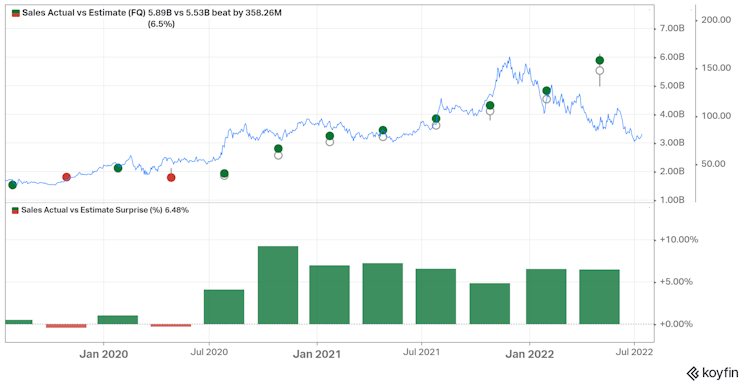

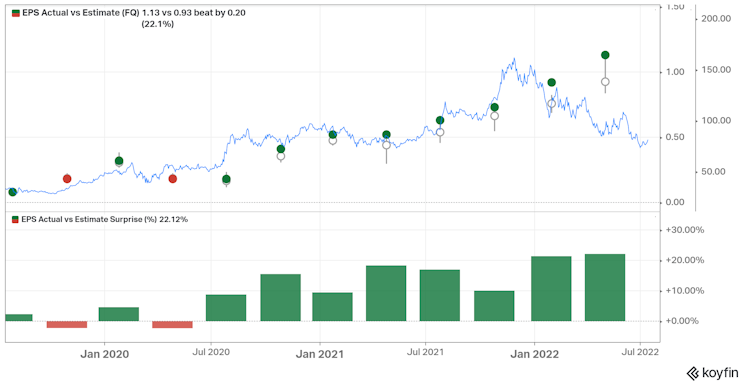

I'm currently basing this on modest expectations, mirrored by the management's guide and exactly on consensus analyst forecasts. As of last earnings, management also incorporated weak PC demand into this guide. Investors would also take comfort in noting that AMD has had a recent trend of under-promising and over-delivering on both sales and earnings. The last miss was Q2 2020, which was perfectly understandable considering the pandemic shock at the time. Even then, the misses were slight. When they've beaten, they've beaten by big surprises, to the tune of 5%+ on sales, and 15%+ on EPS. See the charts below on this record:

Source: Koyfin

Downside Risks

- Macro tends to be more severe, leading to much less demand than anticipated; enough to not fulfil the supply ambitions

- Intel's product offerings rise to compete more thoroughly against AMD

- Other technologies, including non-x86 products, surpass both Intel and AMD long run; such as ARM-based chips

- TSM and partners see greater capacity constraints than anticipated

- Pricing power erodes leading to less profitability and downward revisions in earnings - this could impact the price negatively

Conclusion

With the recent drawdown, $AMD is a compelling buy-the-dip opportunity. This opportunity has been created recently as macro factors have outweighed single stock fundamentals, resulting in a >25%+ drawdown from the recent $108 peak. While prevailing sentiment might be predicated on the drop in overall semiconductor sector demand, AMD should be less impacted by these macro trends as the financials have been driven by rapid market share gain instead. Furthermore, AMD has been somewhat supply-constrained, and some demand weakness shouldn't impact the net outcome on revenues. The prominent dip, therefore, seems like an overreaction. With sales acceleration in major verticals such as data-centre and servers and a broadly strong product portfolio, AMD's momentum should sustain through a down-cycle, even if slightly muted. I expect the business to continue to be driven by big market share gains, against a long-term growth opportunity that is realistically in the $50B+ sales range in a few years.

With a consensus next-twelve-month P/E of 18.8x, the risk-reward is now excellent in my view. If we win, we win big, if we lose, there isn't too much further to go on these valuations to perhaps a reasonable 13-15x P/E bottom. In the case my theory plays out, I expect the stock to reverse course towards $120 in the coming 12 months. Consensus and the market may move towards my thesis should the upcoming earnings calls induce confidence in the existing guide. I see earnings results as the likely catalysts for upside. All AMD has to do is execute as expected at these valuations to deliver compelling alpha.

Disclosure: I am long $AMD

I put some skin in the game with some of the higher valuation growth stocks I’ve added recently. I am excited to watch $AMD story and see if this growth is worth this valuation.

Source: Seeking Alpha

Source: Seeking Alpha

Already have an account?