Trending Assets

Top investors this month

Trending Assets

Top investors this month

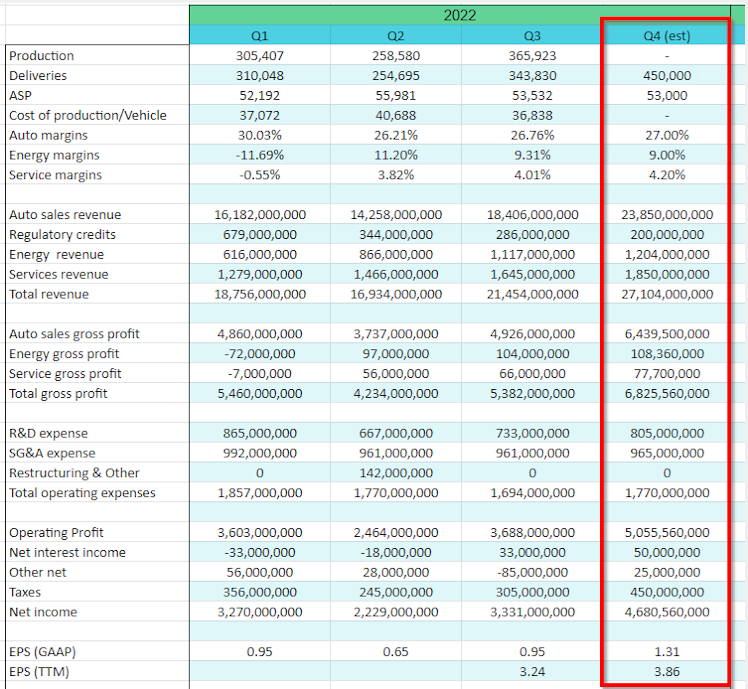

Predicting next quarter results for Tesla

After listening to $TSLA earnings call and going through the shareholder letter, I feel confident enough to estimate Q4 results. Main assumptions are slight margin improvement (Texas & Berlin ramps) and 450k deliveries using Zach's comments about Q4 volume. $TSLA trades at 64 P/E right now, after Q4 that would drop to 53 P/E (lower than Chipotle $CMG and half Amazon's $AMZN). The P/E will keep compressing until they execute the $10B buyback program next year.

Already have an account?