Trending Assets

Top investors this month

Trending Assets

Top investors this month

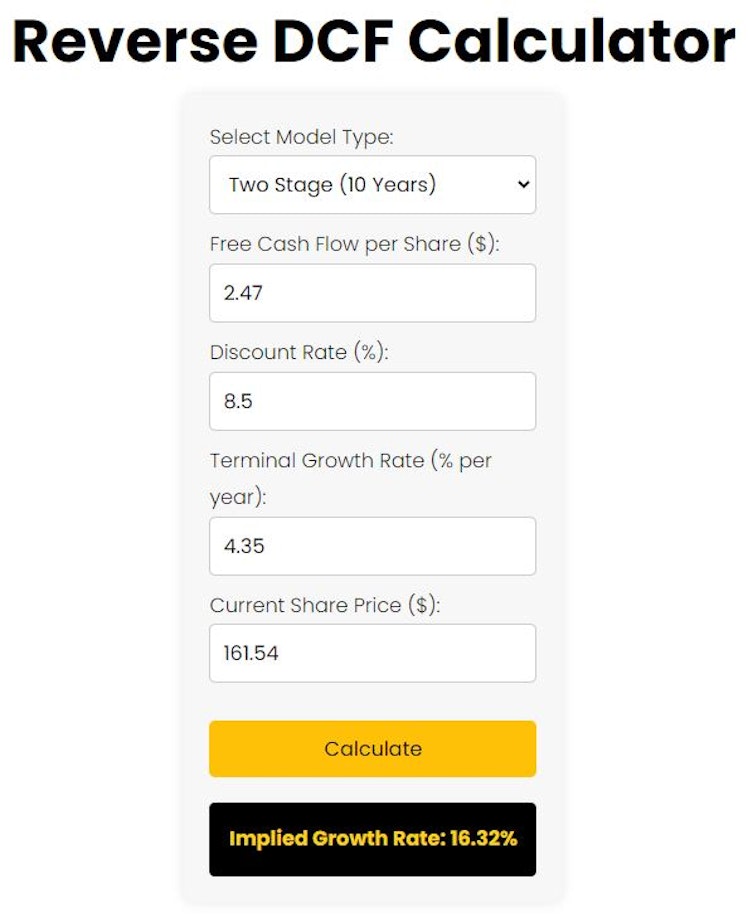

Is SNOW Stock Overvalued?

A reverse DCF calculation on $SNOW states that the market is pricing it at a 16.3% FCF CAGR over 10 years (discount rate taken from Finbox, terminal growth is 30-year yield)

The thing is, it doesn’t include SNOW’s stock-based compensation, which is currently more than FCF

Reverse dcf tool: https://investorscompass.com/reverse-dcf

Investor's Compass

Reverse DCF — Investor's Compass

Already have an account?