Trending Assets

Top investors this month

Trending Assets

Top investors this month

What Moves This Stock: Global-e Online

Cross-border, direct-to-consumer enabler $GLBE will report earnings next Tuesday, and it could be a particularly insightful call for two key reasons.

First, we should receive the first full quarter's worth of information regarding GLBE's partnership with $SHOP, which emerged from its pilot phase in April this year and is now available to most Shopify merchants.

As of fan of and investor in Shopify, I am curious to see how this collaboration progresses. It makes sense for SHOP's international expansion and seems like it could be a game-changer on Global-e, being the smaller of the two.

It also highlights what may be a powerful moat for GLBE, as SHOP has shown its preference to partner with and invest in the company -- rather than try to replicate GLBE's tedious operations within its own walls.

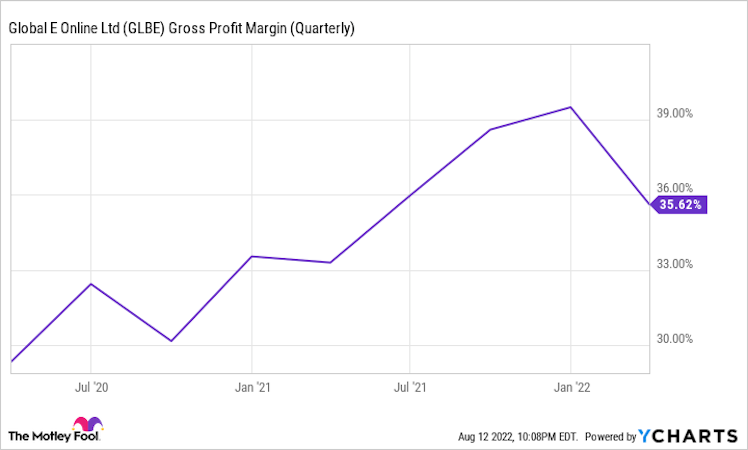

Second, Global-e's gross profit margin has been expanding beautifully over the last two years (aside from the standard drops following the holiday season in Q4).

With any luck, I would love to see these margins improve and turn GLBE into a rare, rapidly-growing, FCF-generating stock.

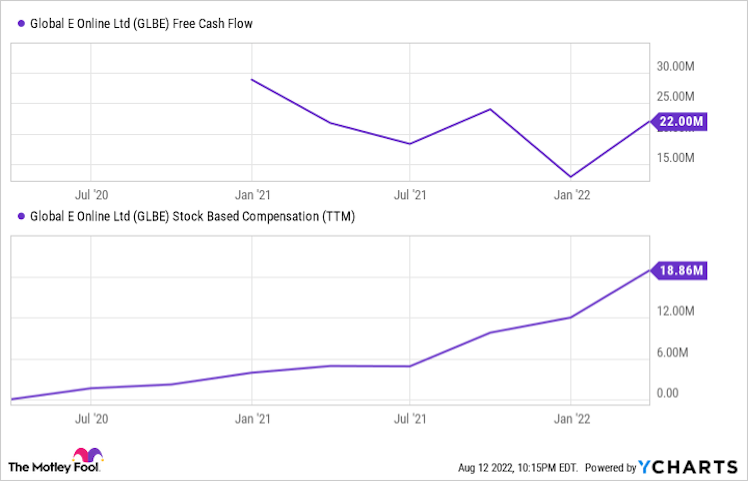

Already FCF-positive (although partially due to stock-based compensation), GLBE's cash generation abilities could become very promising as the business matures.

Having grown Q1 2022 revenue by 65% -- and guiding for 46% growth in Q2 -- this positive FCF is exciting at such an early chapter in the company's growth story.

What are your thoughts on Global-e Online and its worldwide DTC ambitions?

Will Global-E Online beat the S&P 500 over the next decade?

42%Yes

7%No

35%Would rather buy Shopify

14%Would rather buy Amazon

14 VotesPoll ended on: 8/16/2022

Already have an account?