Trending Assets

Top investors this month

Trending Assets

Top investors this month

$28.6MFollowers

$SPOT - Tipping the power scale

Spotify is a uniquely fascinating business to study competitive advantages. They were founded 15 years ago and their profit margins have struggled to break free of the industry's powerful grip. However, that is changing!

This newsletter takes you through the journey of Spotify's path to power.

Introduction

Spotify is a household name and one of the most commonly used applications every day. Spotify is mixed into my daily activities: exercise, commute to work, tasks around the house, listening while working, hosting people, and more. I can switch from a podcast to a nostalgic playlist from the 2000s to a new music discovery playlist unique to my style. Few companies generate the daily usage equivalent to Spotify.

Most people know Spotify is special, but what about their business durability? The company was founded in 2006 and has yet to turn a profitable year. Why should we believe that that will change? Competitive advantages need to translate into sustainable profits. If they don’t, then it is likely not a competitive advantage. So is there a strategy for scaling without near-term profitability?

Brief business overview

Spotify has two distinct product offerings, Spotify and Spotify Premium. Spotify Premium members pay a monthly subscription fee but don’t have to listen to advertisements and can access their playlists offline on multiple devices. Spotify offers a free version with advertisements as a customer acquisition tool. In fact, 60% of Spotify’s paying users first start out using the ad-supported freemium option.

It's no secret that Spotify is trying to become more than just a music streaming platform. In recent years, the company has spent almost $1 billion on podcast-related investments in an attempt to diversify its offering into all things audio, including music, podcasts, live conversations, audiobooks, and more.

The narrative around Spotify is becoming clearer to people as Spotify expands into podcasts and more audio than just streaming music. However, there are still misconceptions on what’s truly important to their long-term competitive advantage and where that value actually lies with these strategic moves.

Industry history

To understand Spotify’s competitive advantages, you first need to understand the backdrop of the music industry.

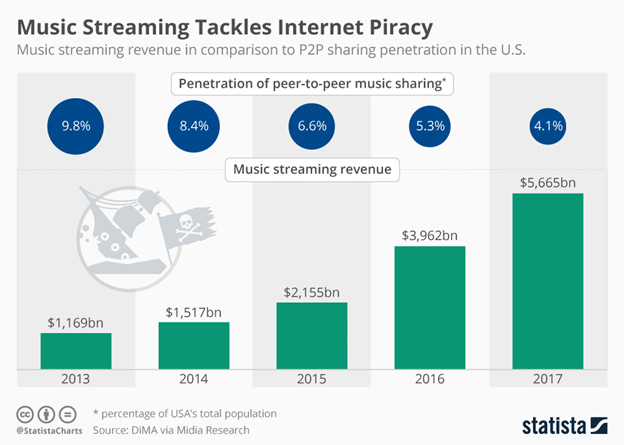

The age of the internet and digitalization completely changed the music industry. Reference the chart below to see the timeline and effects of the monumental changes for revenue generated in the music industry. The music industry was at its peak revenue, with CD sales as the main pillar by the time the internet became popular. However, the industry didn’t adopt the internet fast enough. Napster then steps into the story and launches in 1999, giving access to people across the world to download free music. It was a free service of almost every song you could think of, even songs you didn’t know existed. It sounds a lot like Spotify now; however, Napster was illegal and infringed on copyrights. In 2001, Napster was sued and closed its peer-to-peer network, but the cat was out of the bag by that point. Millions of people were used to getting music for free.

iTunes launched in 2001 and became one of the premier marketplaces for music, but iTunes was just a compromise and not a long-term solution. Consumers were given a digital experience, and labels/artists could still make CD-like revenue per song or album, but only for people willing to pay. iTunes never solved consumer behavior for pirating music. Buying a single song for $.99 or an album for $9.99 was too expensive when you compare it to $0 (FREE!). Now Spotify comes into the picture with its revolutionary business model that changed and revitalized the music industry.

Source: RIAA, Moatology

"We founded Spotify to give consumers something they couldn’t get — music anytime, anywhere, and at the right price. Along the way, we broke the grip piracy had on our industry and restored the growth of global music through paid on-demand streaming." – Daniel Ek, CEO

Spotify was a large step function increase in value for both consumers and suppliers. Consumers could access millions of songs for free or cheap for the premium version, legally, and with a massive increase in convenience and consumer experience by having everything on one app. The value proposition was exponentially better than what iTunes offered and even better than pirating music. Spotify made a better version of free music – that’s hard to beat! Artists and labels were able to start monetizing the consumers that were otherwise downloading songs illegally. As you can see in the chart below, revenue increased as music piracy decreased.

Source: Statista

Counter-Positioning

Brands, network effects, and other competitive advantages can take years, if not decades, for a company to build. But what about younger companies and companies that are still building moats? Counter-positioning is often the period of time the company is digging its moats to fend off competitors for the long term.

Counter-positioning is when a newcomer adopts a new superior business model, and the incumbent does not mimic due to avoiding the damage of their existing business. Counter-positioning was Spotify’s launchpad. At the time that Spotify launched, music revenues were dominated by CDs and iTunes. Spotify introduced a profoundly new business model superior to CDs, iTunes, and even pirating music for free. There are two reasons why counter-positioning contributed to Spotfiy’s success and pushed them to scale rapidly while other competitors in the industry sat back and watched.

First: Damage Aversion

You might have wondered why a powerhouse like Apple didn’t adapt their model quicker and squash Spotify. For Apple, the music streaming model was not compelling enough at the time compared to selling music on iTunes for $.99/song and $9.99/album. iTunes was making 30% of the revenue generated from selling songs and albums.

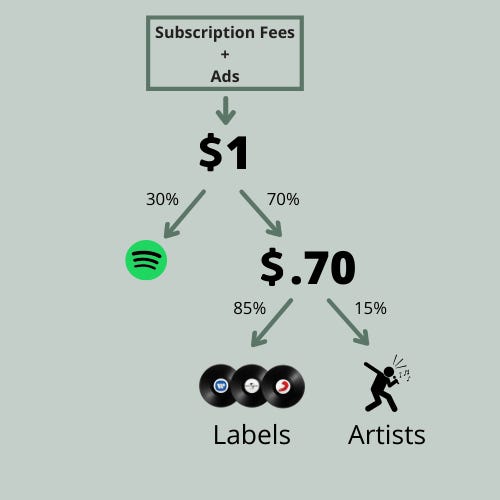

Spotify royalties are distributed from the revenue Spotify collects from ads and premium subscription fees. When Spotify pays artists and music labels, they tally the total number of streams for each artist's songs and distribute the revenue earned based on their share of streams out of the total number of streams. The diagram below illustrates how $1 of Spotify’s revenue is distributed to each party. The important difference from Apple’s model is that it requires subscription or ad revenue, which Apple did not have at the time, so they would’ve started from 0.

The decision Apple (and other incumbents) had to make was either to keep selling songs on iTunes for a profit or start over with a new business model that would initially be losing money. Apple would be starting with 0 subscribers; however, they have a large ecosystem to cross-sell. Of course, Apple decided to milk their profits from iTunes until it was absolutely necessary to switch to the newer, superior streaming model. This dynamic is what gave Spotify breathing room to grow.

Counter-positioning: From a competitor’s standpoint, the new business model had a lower net present value; therefore, they intentionally ignored Spotify to avoid destroying their current value.

Second: Commoditize your complements

Many people think Spotify is a broken business model because music is now a commodity; however, music becoming a commodity contributed to some of Spotify’s greatest powers because it led to higher demand and therefore scale! Spotify’s business model made music extremely accessible for anyone, anywhere, for an extremely low price; the result was commoditizing music distribution. Today, distributing music is not unique to any one company. I can listen to the same songs on Spotify, Apple Music, Amazon Music, or most other music platforms. From Apple’s perspective, they realized that the industry economics for Spotify’s model did not support a long-term competitive advantage because there would be no differentiation. Back to the point above, Apple milked iTunes profits as long as possible because they were in no hurry to join a commodity business. Apple, Amazon, and others eventually adopted the streaming model because it was accretive to bundle several other products to add value to their overall ecosystems.

By the time Spotify launched, the music industry’s revenue was nearly cut in half and the iTunes model was never going to revitalize the industry because it restricted demand. Discovering music on iTunes was limited because of the cost to purchase new songs. On the other hand, Spotify made music so cheap and so accessible, demand for music rose. Spotify allowed people to listen to music that they might not have paid $0.99 to buy. That turns out to be extremely valuable because the number of people listening to music and engagement rates have never been higher.

Microsoft used a similar strategy to sell their high margin software:

"Microsoft’s goal was to commoditize the PC market. Very soon the PC itself was basically a commodity, with ever decreasing prices, consistently increasing power, and fierce margins that make it extremely hard to make a profit. The low prices, of course, increase demand. Increased demand for PCs meant increased demand for their complement, MS-DOS. All else being equal, the greater the demand for a product, the more money it makes for you. Commoditize your complements." - Joel Spolsky

Microsoft successfully built demand for the PC market and pivoted to selling higher-margin software, a differentiated product that would yield a greater competitive advantage.

Music played an important role in propelling Spotify’s scale, but music is now just a complement to its overall strategy. Building competitive advantages is about competing to be unique, which may seem dreary for Spotify’s core business, music, because it lacks differentiation. However, increasing demand for Spotify’s music also means increased demand for their other audio content on their platform. Also, by rearranging commoditized content into personalized and popular playlists with continual updating, Spotify is in its own way creating a form of original content.

Counter-positioning: Incumbent competitors realized the new business model offered no support for differentiation because music distribution would be a commodity; therefore, they ignored Spotify.

Scale = network effects, two-sided marketplace

Daniel Ek talked about the effects of globalization, automation, and digitization:

"You have to either play for being a niche, which could be incredibly profitable if you do it well, or you have to go for scale. And that scale has been completely redefined to a much larger scale than most people would have ever imagined was even possible." - Daniel Ek, CEO

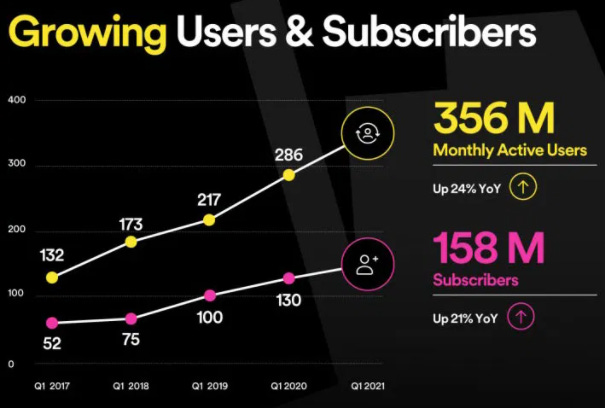

Global-scale is quite clearly Spotify’s goal. Ek has mentioned their addressable market is 2-3 billion users, and they recently reported 356 million active users (158 million premium subscribers), implying a long runway of growth. Scale is the cornerstone on which Spotify is building its competitive advantages, so it is important to understand how they scaled and why.

Source: Spotify

How did Spotify scale?

Spotify achieved mass scale and continues to grow its user base because of a few reasons: 1) Most importantly, as I mentioned earlier, counter-positioning created space from competitors for Spotify to scale. 2) Music is a universal language that is listened to across borders allowing Spotify to reach a global audience. For instance, a Korean pop band like BTS can sell-out concerts in America. 3) Spotify’s user experience (UX) and user interface (UI) were superior to competitors.

Why did Spotify choose to scale?

I briefly touched on the economics of Spotify generating $1 of revenue, but here’s a refresher:

- Spotify keeps about 30% of the revenue.

- The music labels, the biggest of which are Universal Music Group, Sony Music Entertainment, and Warner Music Group, take about 60%.

- Lastly, the artists take about 10% of the revenue generated.

The problem, which has been widely discussed amongst investors, is that Spotify has a marginal cost problem. For every additional user Spotify attracts and additional revenue they make, they still payout 70% of their revenue to the labels and artists. As their revenues increase, their costs increase in a synchronized manner. This is why investors have balked when realizing Spotify has been growing for 15 years yet hasn’t turned a profit. At a smaller size, Spotify has no power to change its current profit structure.

Two-Sided Marketplace

There are two sides to a marketplace — the demand side and the supply side. When music or podcasts are posted to Spotify, it creates supply. When a person is looking for music or a podcast to listen to, it creates demand. Spotify needs to convince the supply side that it is worth it to post on Spotify because there needs to be an assurance that it will be met with a large demand of people wanting to listen. Spotify also needs to convince the demand side that they should sign up with Spotify because they supply users with high-quality content and has a greater variety.

As you can see, a two-sided marketplace has a chicken and the egg problem. It is a delicate process of deliberately scaling while balancing supply and demand to create a functional ecosystem. In the beginning, Spotify agreed to unfavorable terms with the music labels because they needed their large back catalog of music rights, which would bring the supply onto the platform. The labels agreed to terms because they were searching for ways to overcome the piracy issue. Spotify made the supply side of music labels’ distribution a commodity (cheap and available to everyone), which greatly increased demand. Thus, creating a symbiotic two-sided marketplace of supply and demand.

Now Spotify sits in the middle with control of two sides of the market and 356 million users. However, for Spotify to break away from the music industry’s grasp of its business margins, it needs a differentiated value proposition for its buyers and suppliers.

Demand Differentiation: Podcasts & Other Audio

Within the last couple of years, Spotify allocated a lot of capital towards building its podcast ecosystem, especially focusing on exclusive podcasts only on their platform. They acquired companies that give people the tools to create podcasts and signed deals with podcast superstars, such as Joe Rogan. But why didn’t Spotify get into podcasts earlier?

For podcast creators to see the value in exclusively offering content to a platform like Spotify, the platform must have a large audience. This was the key to commoditizing music and building a large-scale audience. Spotify will offer other forms of audio, such as live audio, similar to Clubhouse. The dynamics of network effects will be present in all forms of user-generated audio content: podcasts, live audio, etc. With Spotify’s strategy of investing in new audio content, they gain unique and exclusive audio content that offers a differentiated value proposition to consumers. The more people on Spotify, the more valuable the platform becomes because it will attract more supply (audio content). The more supply on Spotify, the greater the demand (users), which creates a perpetual cycle of increased supply and demand.

Spotify sits in the middle, tasked with tearing down the friction between connecting the supply and demand. The easier Spotify makes it to search for new audio content and to experience the content, then it will add fuel to the virtuous marketplace cycle.

Supply Differentiation: Advertisements

Continuing on the benefits of scale and the network effects of an online marketplace, advertisement dollars follow highly engaged and large markets. As Spotify’s users grow, the value proposition for placing ads on Spotify will increase.

Back in 2019, Spotify tried to play their hand in owning music rights to improve their margins, but Spotify's role was to increase the supply-sides value proposition and realized it is better to become great partners for the labels and artists. They also needed the music labels because of their valuable back catalog of songs. The labels supply is what feeds the machine of the two-sided marketplace.

Spotify released Marquee, which the labels can use to promote songs and albums. Even though Spotify still pays out 70% because of music royalties, they effectively increase their profit share because labels will funnel more money into advertising their music catalog.

Finally, after 15 years, Spotify will start to break away from the industry's stranglehold on their margins because ads sold on Spotify will be a higher contribution margin than music streaming.

Spotify’s two-sided marketplace is a moat because it’s hard to disrupt. A competitor needs a greater value proposition for both the supply-side and the demand-side. Scaling has and will continue to strengthen Spotify’s position of power.

Pricing Power

Pricing power is often an indication of a moat. Customers tend to be more price-sensitive when the product is undifferentiated. That is why up until now, the price for customers has not increased and most of the economics go to the music suppliers.

If a company has a moat, then it’ll be able to sustain a lower cost structure or command a higher price. A company can sustain a premium price only if it offers something that is both unique and valuable to its customers. Spotify’s customers are its consumers and suppliers.

Pricing power - consumers:

Spotify increased the price of many of its subscriptions across the UK and parts of Europe, with the US only seeing a hike to its family plans. However, pricing power isn’t just when a company raises prices. Raising prices can often mean that the company realizes they’re capped out in terms of its addressable market. The reason Spotify has pricing power is because Spotify’s plan is to reach 2-3 billion people and they are currently at 356 million. They are at a fraction of their goal, yet they are still raising prices. Scale, as I talked about throughout this newsletter, is the name of the game for Spotify. They would not jeopardize that strategy for the sake of increasing prices unless they are confident they can still sustain their growth.

Pricing power - suppliers:

Marquee, their advertisement product for music labels, demonstrates pricing power because it effectively lowers Spotify’s cost structure.

Narrow Moats & Mistaken moats

Data:

- Defensibility is not inherent to data itself, and the value of incremental data decreases over time. Data is undoubtedly essential to Spotify because it gives Spotify greater insight into curating playlists, ad placement, and several other key components to improving its product and monetization. However, I’m often wary of investors saying, “data is the moat because more data means better song recommendations, which means more users and then more data, and so on…” Claiming Spotify has a data moat misrepresents their true competitive advantages.

- Data is at the heart of most digital companies now. Every company needs to gather and use data as part of its strategy to compete on the internet. It is now a minimum threshold. With enough critical scale, a new company can get a decent dataset to compete.

Subscribe:

Already have an account?