Trending Assets

Top investors this month

Trending Assets

Top investors this month

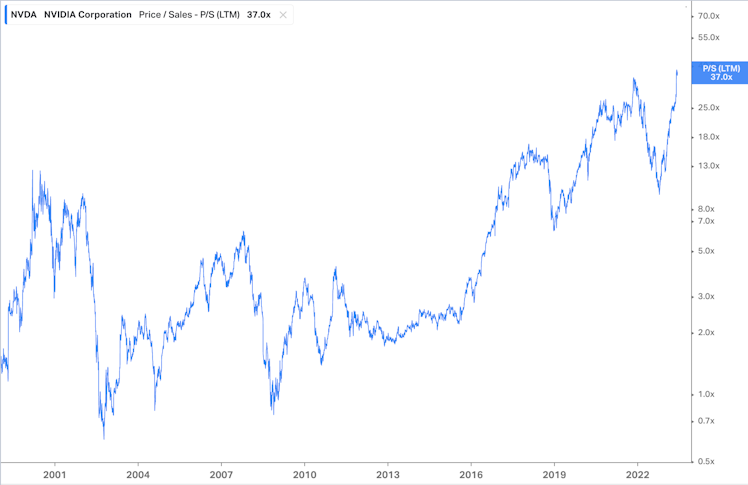

The Problem With Paying 37x Sales for Nvidia

Disruptive new uses cases pop up every day for Artificial intelligence, making it the topic of conversation in the stock market. This has had a dramatic impact on $NVDA, which specializes in processors that power new AI applications.

- Nvidia's share price has increased 161% so far this year.

- Its market cap briefly hit $1 trillion.

- Nvidia is trading for a whopping 37x sales, 153 times EBITDA, and 204x EPS.

In the past, I have speculated that other companies like $TSLA couldn't sustain growth, and I was wrong. So my opinion that $NVDA will disappoint probably isn't worth much.

Instead, I want to talk about how paying a premium multiple can be consistent with a value-oriented investment approach.

Many value investors focus exclusively on companies that are trading at a low multiple of sales or earnings. But you could look at it a different way;

Instead, simply look to buy businesses for less than they're worth.

Often, these businesses will be unknown or unloved and will therefore trade at low multiples. But sometimes, a stock can be a bargain, even if it trades at a lofty price relative to its current performance.

Consider a company like Costco $COST. Investors could have paid a healthy 40x trailing earnings for Costco at any point since 2002 and still earned at least a 10% compounded return. Or look at Amazon $AMZN and Booking Holdings $BKNG, where early investors could have paid 40 times sales and still achieved attractive long-term returns.

It's tempting to look at those success stories and conclude that quality is the only factor that matters for long-term investors. But these companies are the rare exception— not the rule. Amazon and Booking both endured brutal periods when their share prices plummeted more than 90%. And for every Amazon and Booking, there are dozens of examples in which paying a premium price produced poor performance.

One potential analog for Nvidia is Cisco Systems $CSCO, a company whose hardware enabled the creation of the internet. Like Nvidia, Cisco's valuation surged in a short period of time, ultimately reaching a peak of 36.8x trailing sales in early 2000. But demand for Cisco's networking products declined during the dot-com bust, and the company faced more competition than investors anticipated. Cisco has proven to be a strong and durable business that produces plenty of free cash flow, but its share price remains well below those dot-com-era levels even more than two decades later.

It's not sufficient for a business to have strong competitive advantages, sound financials, and a shareholder-friendly management team. Stocks must also be attractively priced relative to a conservative forecast of their future performance. You must invest with a margin of safety in order to limit losses when your investment thesis doesn't play out as you'd expect.

It's entirely possible that Nvidia will prove to be a market-beating investment from current prices. But buying a company at 37x sales requires quite a lot to go right for quite a while. Any slip-up in execution, increase in competition, or shift in geopolitical conditions, and the stock will likely get slammed. I'd rather be conservative in terms of both the modeling assumptions and the price.

Already have an account?