Trending Assets

Top investors this month

Trending Assets

Top investors this month

Telecom Sector in a Downturn: Opportunity for Bargain Hunting?

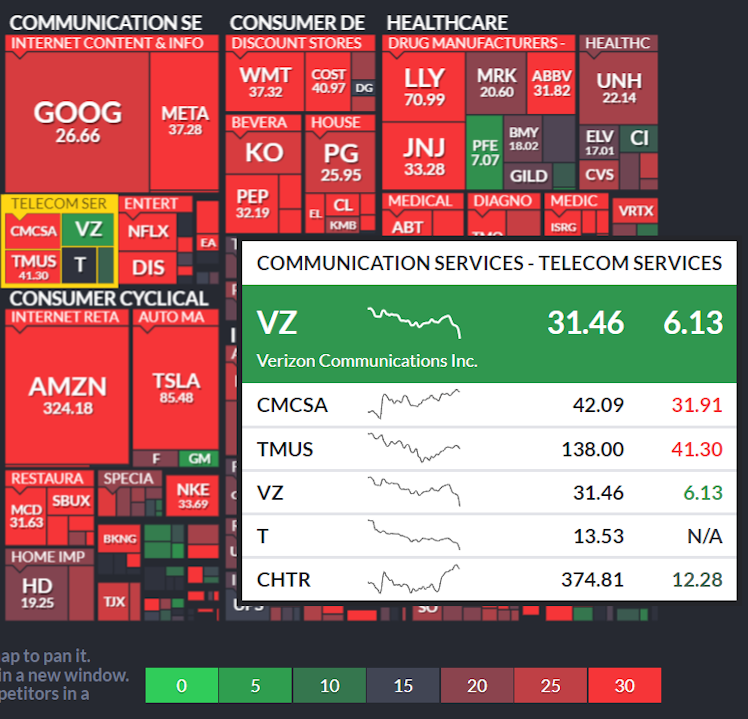

The telecom sector experienced a significant decline on July 17th, with stocks like $T and $VZ dropping approximately 6.7% and 7.5% respectively, making them among the worst-performing companies in $SPY.

The catalyst for this downturn was the recent downgrade of $T's rating by $JPM due to concerns about its wireless and broadband business progress.

According to recent discussions by management, the expectations for wireless (reduced in May and June) and broadband (in June) have been lowered. AT&T is facing modest pressure in its mobile business (from Verizon, T-Mobile, and cable TV), consumer wireline business (from cable TV and fixed wireless access), and ongoing pressure in its business wireline segment.

The projected growth rate for mobile communications is expected to decline from 4.7% in 2021 and 3.5% in 2022 to just 2.5% in 2023. Prepaid gross add share has declined from 32% in 2022 to an estimated 30% this year.

In late June, AT&T's CFO reported that new mobile subscribers were around 300,000, significantly lower than the Wall Street analyst forecast of 476,000.

Regarding its broadband fiber business, AT&T is expected to regain some market share for its cable TV companies but is also facing rising bandwidth costs. The company is preparing to cut expenses to repay debt.

While AT&T continues to generate "substantial" free cash flow, the amount available for debt repayment or share buybacks is limited. Cash generation from DirecTV will continue to decline, with half of the approximately $8 billion in free cash flow being used to pay dividends, further diminishing its appeal to shareholders.

With the upcoming $2.4 billion C-Band payment at the end of 2023 and higher taxes, the company's balance sheet repair funds will be quite limited.

As a result, even though companies in this industry are currently undervalued, at historical lows, and still offer decent dividends, investors remain uninterested.

Already have an account?