Trending Assets

Top investors this month

Trending Assets

Top investors this month

$10.5MFollowers

Palantir - Thesis is drifting, but not dead

Hey everyone - I wanted to share some thoughts on Palantir, a name I've been invested in since the IPO. The company was one of the hottest listings in 2020, got caught up in the meme stock frenzy in 2021, and now sits slightly above offering price in 2022. Keep note that I am a Palantir shareholder, am subject to bias, and am not publishing this with any recommendations to buy nor sell.

Palantir $PLTR reported quarterly earnings earlier this month, August 8th, delivering 26% top line YoY growth and EPS of -0.01/share. Shares sold off steeply during the session as investors were clearly disappointed by decelerating growth (Prev. guidance was 30% annually) and an even softer guide into the back end of the year. As I write this, shares are trading just above IPO price, nearly 80% down from highs in 2021. As a shareholder, I am growing concerned about the original thesis on Palantir, which can be dumbed down to a few bullets:

- Government clientele provide steady, reliable revenue

- Leading AI software platform sold as a service (yielding +80% gross margins)

- Network effects from government segment to drive value prop in booming commercial segment

Palantir was able to command a significant premium on their valuation (PLTR traded ~19x Fwd sales as of 12/31/21) given that the company was compounding revenues at 30-40% annually, with commercial customer growth jumping 100-150% simultaneously. While Palantir is still grossing impressive customer growth figures (ex-government), revenue growth has slipped below management's initial estimates of 30% per year through '25, and guidance appears to be softening.

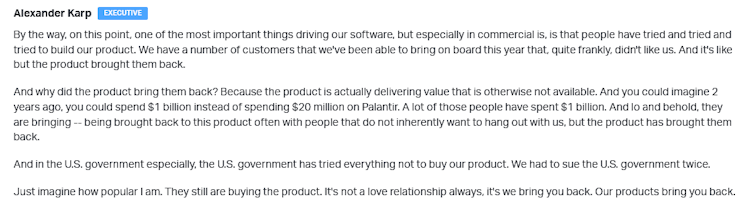

This is concerning from a few perspectives. First, this implies that Palantir's government segment is not as predictable as management seems to believe. On top of that, it doesn't appear like Palantir management has the best relationship with their government clients (pictured below). Generally speaking, government customers are expected to be slow, but typically come with large & reliable revenue streams. The comments below, coupled with a meager 13% bump in government sales last quarter, do not reinforce my waning confidence in management.

My second concern is that my initial characterization of Palantir as a SaaS company appears to be only partially true. I won't doubt that Foundry, Gotham, etc. are software. Rather, the concern lies in the fact that Palantir is a human capital intensive business, a point reinforced by the past three years of share-based compensation (albeit shrinking on a relative basis) and the wide fluctuations in operating margin. By that nature, it is uncertain to me that Palantir can exhibit zero marginal costs of distribution like other SaaS businesses. In that vein, it may make more sense to characterize Palantir as a consulting or services business.

H/T: Christopher Wan

All of that being said... I don't believe Palantir is dead in the water. In fact, their products continue to broaden the Overton window for data analytics in corporate environments. If their commercial segment were a Pre-IPO startup, it would command a significant premium in private secondaries. As a futurist, I am unbelievably optimistic about Palantir's role in the future of artificial intelligence, particularly in commercial applications. It is clear that the product is finding market fit, and believe there is an enormous servicable market within Palantir's grasp.

But, the point still remains... Is Palantir overvalued? Are we mistaking price action for fundamentals? Is management the victim of their own hubris? I'm staying put for now, but would love to hear everyone's thoughts.

Tom

Already have an account?