Trending Assets

Top investors this month

Trending Assets

Top investors this month

Thinking about getting back into a name I used to own for most of this year but sold it as rates heavily declined in early July.

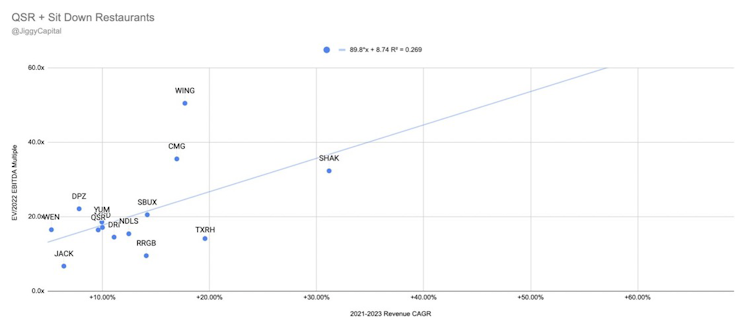

$SHAK growth paired with reasonable EBITDA multiple is quite enticing and relative underperformance of late can bring some ST opportunity.

Here is the broad restaurant space multiple comparison (QSR + sit down) using 2021-2023 Revenue CAGR vs 2022 EV/EBITDA multiple

Already have an account?