Trending Assets

Top investors this month

Trending Assets

Top investors this month

Our next purchase -- CrowdStrike $CRWD

@brianferoldi and I switch off every week picking the stock we'll be putting real money into. This week was my turn. I chose one of my highest-conviction (and currently my largest) holdings: CrowdStrike $CRWD

Here's why:

For starters: this is as mission-driven of a company as you'll ever find.

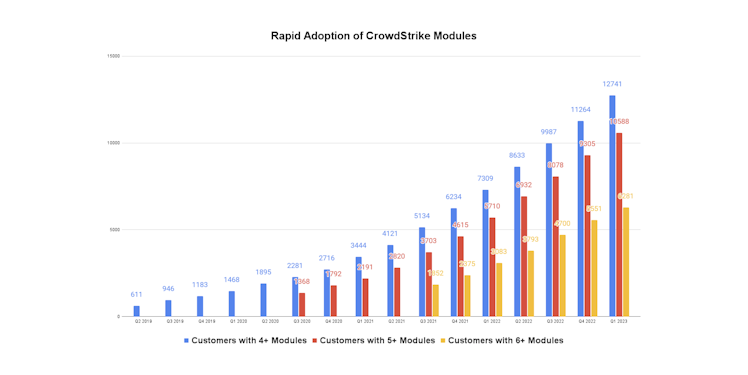

That shows the company has 22 tools and an App Store currently. When it went public less than three years ago, it had half as many. That underscores the optionality baked into CrowdStrike's business model.

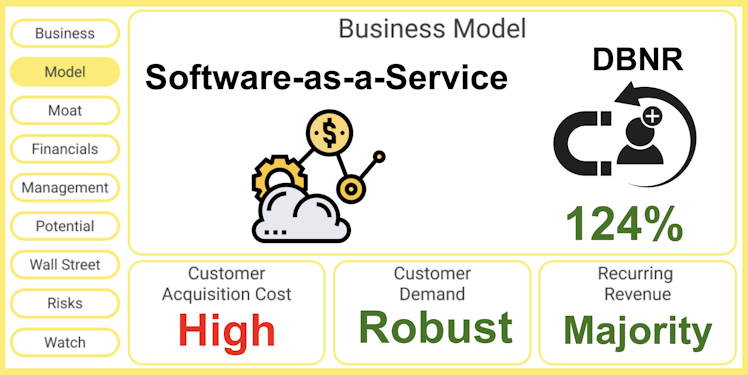

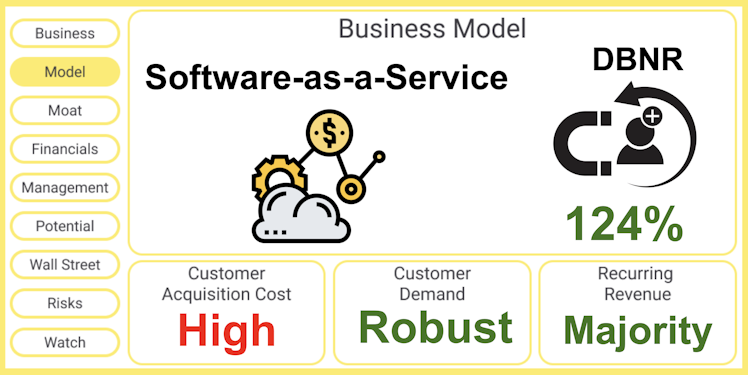

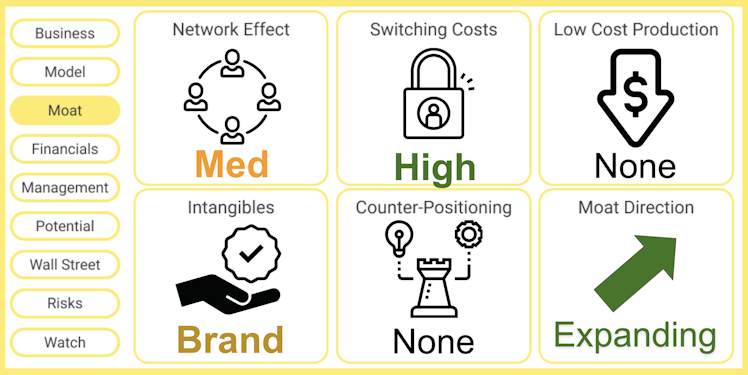

While customer acquisition costs are high, we believe the moat around the company is wide enough that it justifies the spending.

The network effect is enhanced because the more customers $CRWD has, the better its' system is. When one user has a unique breach detected, all other current users receive (relatively quickly) a form of immunity. More users = better protection.

But not only that, the number of customers adopting MULTIPLE TOOLS has gone through the roof -- adding to switching costs.

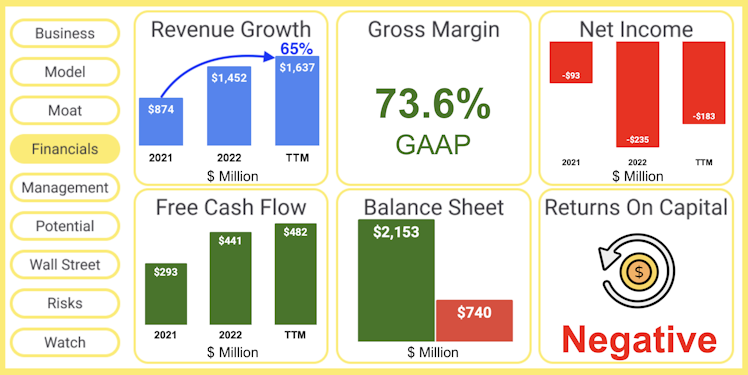

While not "profitable" on a GAAP basis, this is a free cash flow machine with a stellar balance sheet.

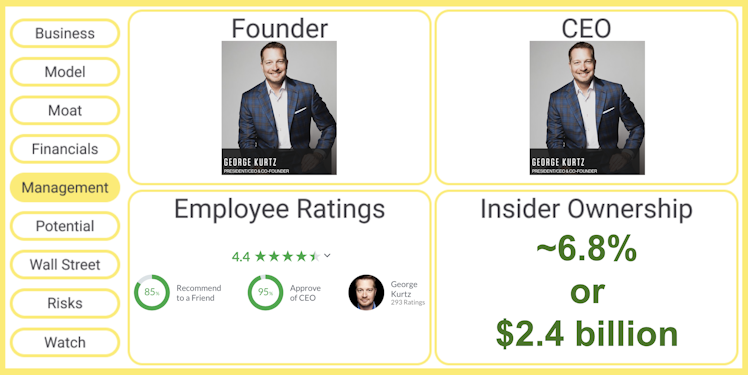

We love the founder-led management team that gets great reviews and has lots of skin in the game

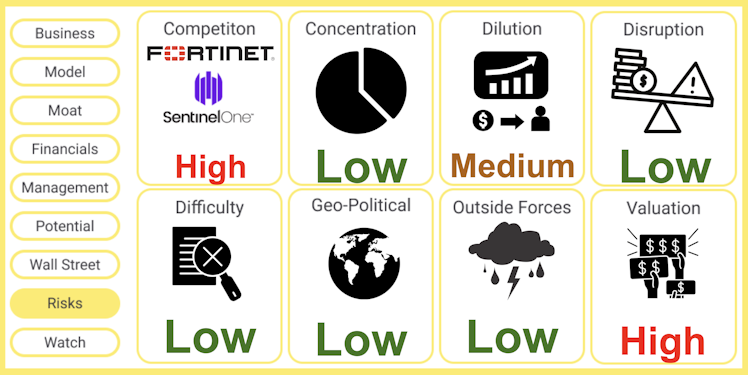

But it's worth acknowledging the biggest risks. Over the short-term: dilution and valuation. Over the long-term: competition and the risk of being hacked.

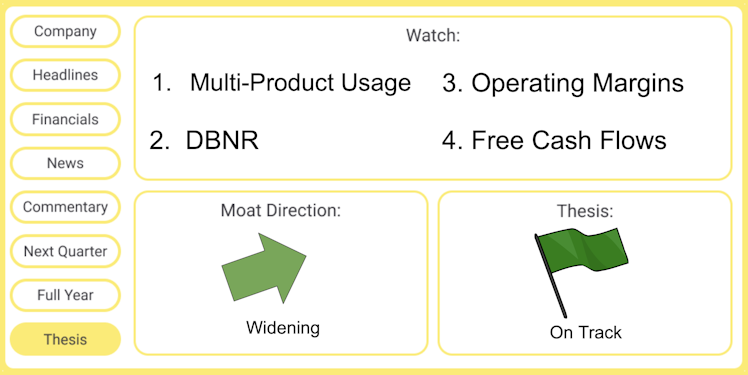

Looking ahead, this is where we'll be focusing our attention

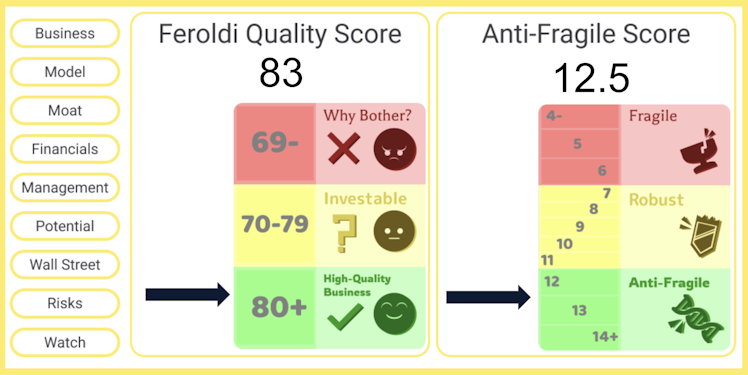

All in all, it's one of the highest scoring companies on both of our frameworks

But what do YOU think of CrowdStrike: both the company and the stock?

CrowdStrike is...

73%A great company to buy today

26%Great..but stock too expensive

69 VotesPoll ended on: 6/23/2022

Already have an account?