Trending Assets

Top investors this month

Trending Assets

Top investors this month

A Simple Trade With Almost 0 Downside - $SHLX

The set up is very simple. Shell plc is the majority shareholder of a small subsidiary called “Shell Midstream Partners” [$SHLX ] . In early Feb, Shell Plc offered to buy out the remaining public shares of $SHLX for $12.89/share and take the company private.

I believe precedent deals suggest Shell is likely to come back with an offer in the $14.50-$15/share range in the next ~3 months. On the low end, that is a ~3-5% premium from today’s price.

On top of that premium, investors will be able to rack up $SHLX’s ~$0.30/share/quarter dividend while waiting for the acquisition to finalize, which will add another few percent to the return. All in, I think investors will get 7-10% return in the space of a few months for a deal I think is overwhelmingly likely to happen, with some possible upside if the huge spike in oil/gas prices puts some pressure on Shell to increase their bid.

Some background to understand how we got here, and why I think this deal is likely to happen:

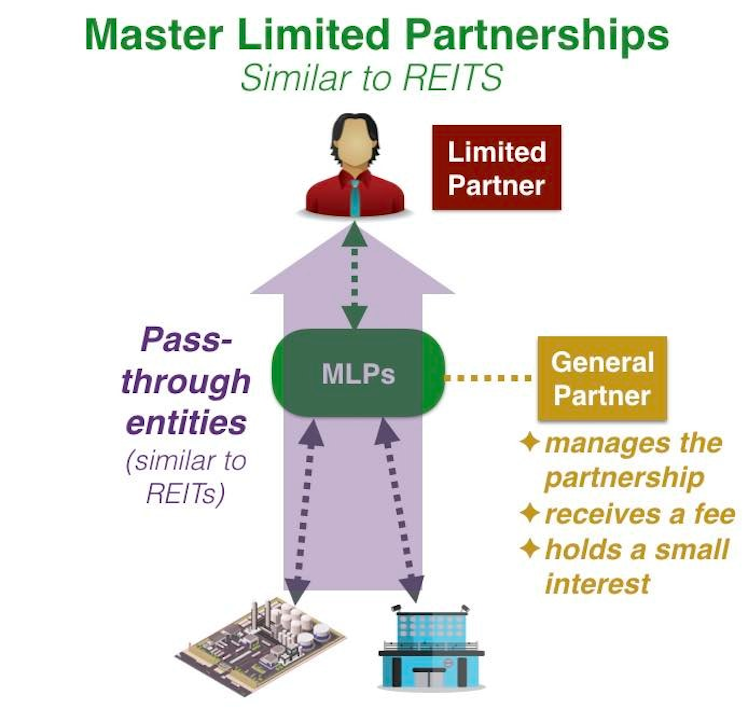

In the mid-2010s, MLPs were all the crazy. Investors loved buying into these because interest rates were low and MLPs offered a high distribution / dividend yield. MLPs took advantage of this craze; investors were valuing MLPs on dividend yield and growth, so MLPs would issue tons of shares at low implied equity costs to buy lots of assets, which generated growth and let them keep growing the dividend. Dividend growth meant the share price would go up, which let them issue more equity, which let them buy more assets….

So, with the market crazy for MLPs, Shell IPO’d SHLX in 2014 at $23/share. SHLX owned a bunch of Shell’s onshore and offshore pipeline assets (as well as a few other assets).

Dividend crazed investors put a huge multiple on SHLX; as the MLP game fell apart, that price proved way too generous and SHLX’s shares have generally languished despite paying a juicy dividend.

So the stock hasn’t worked because investors gave it way too generous a multiple initially, but the company did do what they set out to do: acquire assets and grow the dividend.

SHLX comes public paying an annual dividend of $0.65/share; in 2020, they did a massive transaction to internalize their GP and alongside that basically froze their dividend at ~$1.84/share/year.

Fast forward to 2021, and in July SHLX cuts their dividend from $0.46/share/quarter to $0.30/share/quarter. SHLX is now a broken MLP; their stock is too cheap to issue equity to acquire assets (it’s hard to accrettively acquire assets when your dividend yield is ~10%!), and without accretive access to the equity markets SHLX has no real reason to exist.

In early February 2022, with SHLX continuing to languish at <$13/share (just under a 10% yield), Shell lobs in a no-premium offer to buy the whole company for $12.89/share.

That brings us to today:

SHLX is trading for ~$13.80/share as I write this, a nice premium to the initial Shell bid. On the low end, I expect Shell will up their bid to the ~mid-$14s in the next few months, and shareholders today will walk away with a nice gross profit and an excellent IRR from today’s levels (SHLX will almost certainly continue paying their dividend up until Shell takes them private; with a quarterly div of $0.30/share the IRR gets really interesting if Shell’s bid comes in anywhere above today’s share price).

So it’s a pretty simple set up and thesis. I think the key questions to think about here are:

- Why is Shell trying to take SHLX private / why does it make sense?

- With shares trading at a nice premium to Shell’s initial bid, why do I think there’s more upside to SHLX?

Let’s start with the first question: why is Shell trying to take SHLX private, and why does it make sense?

From a strategy standpoint, Shell would be following in the footsteps of a lot of their peers by taking out SHLX. In the past year, we’ve seen BP take out their midstream MLP (BPMP), and one of the first things Chevron did once they bought Noble was take out Noble’s MLP, NBLX. Reading the proxy for Chevron / NBLX is instructive; Chevron closes the Noble deal in October and begins looking into a take private for NBLX in November.

So Shell would be following in the footsteps of their peers by taking SHLX private; let’s take the question broader and ask why are all these players looking to take out their MLPs? I think it’s a combo of factors:

- First, buying out your MLP is simply good financial engineering. Consider Shell; they’re an investment grade borrower, and they most recently raised LT debt at ~3%. They own almost 70% of SHLX, and they guarantee (or are the lender for) all of SHLX’s debt. Say Shell offered $15/share to buy SHLX (just to get crazy on the premium). They’d be buying the minority equity out at an 8% yield and financing it with super low cost debt. On top of that, with SHLX now internalized they’d be able to cut out millions of SG&A and third party reporting costs. Not a bad trade!

- Second, there’s no real reason for these entities to exist anymore. The initial promise of these MLPs was they’d have a low cost of capital, which they could use to grow accretively. With the stocks now trading for almost double digit dividend yields, there’s no reason to have them separate from the parent company (and incur all the costs of having separate companies).

- Third, MLPs were popular in the early 2010s because getting assets out of the corporate umbrella and into an MLP cut down on the double taxation of having an asset in a corporation (where the corporation would pay taxes on income from the assets, and then the individual would pay taxes on dividends received). Thanks to the Trump tax cuts, a lot of that “double dipping tax shield” has gone away, so there’s a lot less of an incentive for MLPs to be out there.

I’d note that Chevron / NBLX specifically mention all of those reasons for wanting to do a deal in the background of their transaction (see p. 23).

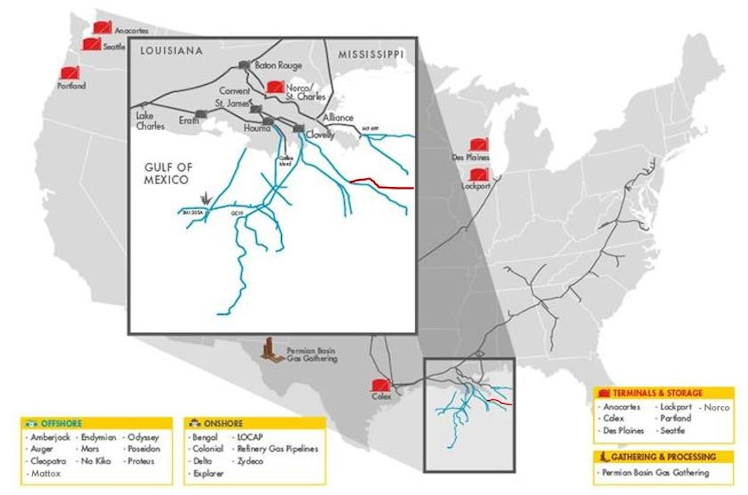

I think there’s one more Shell specific reason for Shell to want to take out SHLX. A lot of SHLX’s assets are crucial offshore infrastructure in the Gulf of Mexico; with oil and nat gas prices where they are currently, it would be very attractive for Shell to increase drilling / production offshore in the long term. Buying SHLX now would simplify their infrastructure plans if they want to increase drilling in the future.

The bottom line: It makes all the sense in the world strategically for Shell to take out SHLX.

Which brings us to the question of price. SHLX is currently trading for ~$13.80/share, a ~7.5% premium to Shell’s initial (no premium) bid.

That’s not a huge premium, but clearly the market is factoring in some sort of topping bid here. Still, I think the market is thinking too low; both $NBLX and $BPMP had larger premiums in their second bids.

- Chevron initially offered $12.47/share for NBLX in early Feb. 2021; they reached a deal in early March at ~$14.27. A 14.4% premium.

- BP initially bid $13.01/share for BPMP in early August; they ended up with reaching a deal in late December with stock for stock offer that valued BPMP at ~$14.75/share A ~13.4% premium.

The trend is pretty clear hear: make an initial bid, and then bump the bid up by 13-15% in a few months to get a deal done.

I expect that’s what happens here; on the low end, that would put Shell’s bid for SHLX over $14.50/share. I think a deal would close reasonably quick; BPMP announced their deal with BP in late December and expects to close this quarter (in Q1), and Noble/Chevron announced their deal in early March and closed it by Mid-May.

Assuming SHLX announced their deal in the next 2 months at the low end of pricing ($14.50/share) and closed by the end of oct, investors would clip one dividend between now and close and would generate a gross spread of just over 6% and an annualized return over 20%.

That’s a pretty sweet return for a deal that is overwhelmingly likely to happen and has basically no correlation to the broader market indices.

There are also a few extra kickers that might force Shell to pay a higher premium than expected to get their deal done:

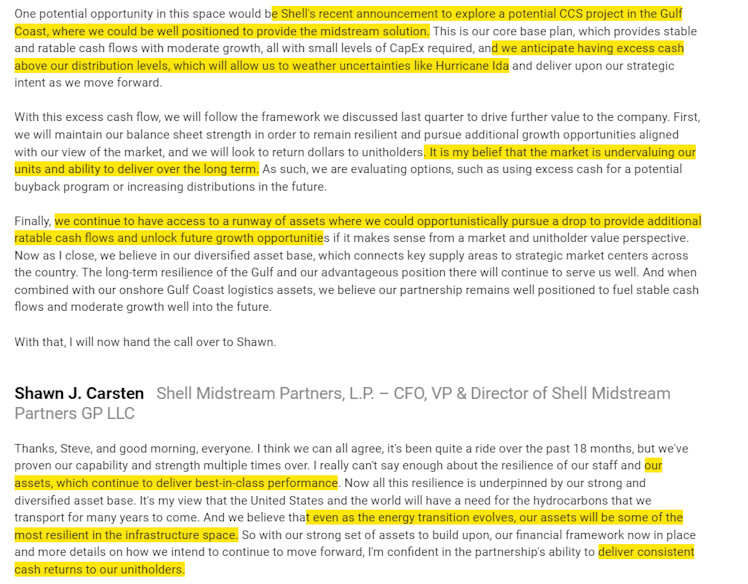

First, check out the clip below from SHLX’s Q3’21 earnings. SHLX’s stock was just under $13/share at the time. That’s a troubling quote for Shell in two ways: it shows that SHLX is critical to their growth plans, and it’s an insider saying the stock is undervalued.

Combined, it could lead the special committee to push a little harder on Shell for a bump in deal price, or it could lead an activist to try to break the deal or sue the company for fiduciary breach if the premium isn’t juicy enough.

Activism is rare in the MLP space given all of the conflicts of controlled MLPs, but it has happened before and courts generally don’t love majority shareholders who control companies (like Shell does SHLX) taking minorities out at unfair prices!

Second, oil and nat gas prices have gone up a good deal since Shell first made their offer due to obvious geopolitical reasons. Again, SHLX’s assets are likely critical to Shell’s plans in the Gulf, and oil and nat gas prices going up should increase the value of those plans. Taking SHLX out now becomes more urgent, and the NPV of taking them out goes up with higher prices. Again, might suggest a larger than normal bump.

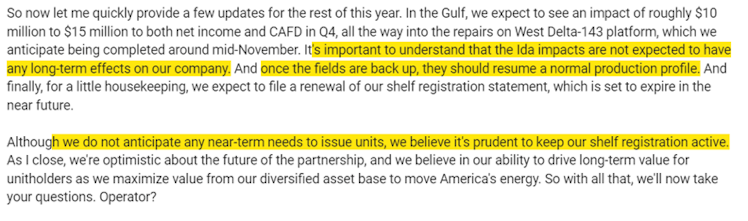

Third, SHLX’s trailing numbers have significant drags. They have an investment in a Colonial Pipeline that is currently not paying a dividend, and a lot of their Gulf assets were impacted by Hurricane Ida.

On trailing numbers, a bid for SHLX at ~$14.50/share looks reasonable. But SHLX might push Shell to give them some value for those items, which again could lead to a larger than normal premium here.

I’m going to wrap it up here:

This is a simple idea; it’s a transaction that’s very likely to happen and one that makes significant strategic sense. I think the returns will be solid with little/no correlation to the broad market indices and the potential for very strong returns is possible if we get value from any of the upside kickers I mentioned.

I love this idea because it’s rare to find opportunities where the sole risk is that you might not make as much money, instead of you might lose all your money.

What’s the downside if I’m wrong and Shell walks away from the deal?

Well, SHLX probably trades back to its pre-offer price of just under $13/share, so the downside isn’t crazy. But since that offer, oil prices are up ~10% along with long term rates rising. SHLX is a yield play dependent on oil/gas prices; I’d suggest they are in a much better fundamental place today than they were just a few months ago before the bid came out. Honestly, I think you could argue the price of SHLX would be around where it is right now even if Shell had never bid on the company.

The Catalyst

Shell raising their bid and completing the acquisition of $SHLX

Already have an account?