Trending Assets

Top investors this month

Trending Assets

Top investors this month

It has been a wild ride since the start of the pandemic.

I'll publish a complete update on $DG on Tuesday morning (Monday is a holiday in the U.S.), but one quick thought: I'm pretty surprised to see them reiterate the FY22 EPS guide (I think the market is as well, which is why shares are up 10%+ premarket). We saw significant P&L pressure on both GM's and SG&A this Q (with EBIT -18% YoY), which leaves a lot of work over the remainder of the year to get to DD EPS growth (53rd week helps).

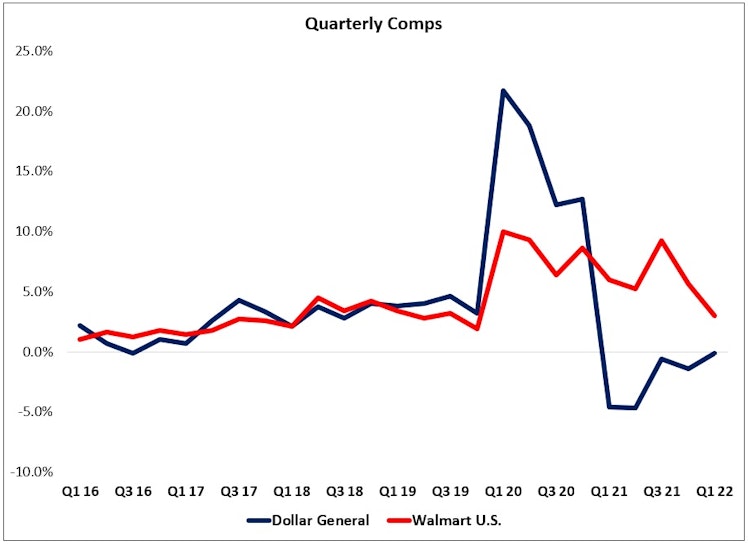

On the other hand, $DG looks well positioned IMO to navigate through this period (relative to retail peers; I'll need to update $WMT, $DLTR, and $FIVE as well). As shown above, they lagged by a wide margin throughout FY21, largely due to business mix. Based on commentary from Walmart and Target, I think we'll see some of that reverse going forward. (A lot of the general merchandise categories that $DG has a small / no presence in are rolling over.)

As always, it's important to keep short-term results in the proper context (assuming you're a long-term investor, as I am). The underlying TSR algorithm for $DG remains in tact, and pOpshelf, Mexico, etc., are important additions to the thesis (optionality). FWIW, the equity traded at ~17x forward in advance of the Q1 results.

thescienceofhitting.com

TSOH Investment Research Service | The Science of Hitting | Substack

Long-term investment research with 100% transparency (prior disclosure of all portfolio changes). TSOH is written by Alex Morris, a former buyside equities analyst and CFA Charterholder. Click to read TSOH Investment Research Service, by The Science of Hitting, a Substack publication with tens of thousands of subscribers.

Looking forward to it, I had noticed that Dollar General rocketed this morning, more so than the broader market.

Anything in particular during the call you felt that catalysed that? Not that it ultimately matters, but.

Already have an account?