Trending Assets

Top investors this month

Trending Assets

Top investors this month

Skyline Champion Corporation – A Compelling Investment Opportunity

Every month we share 2 write-ups on companies we decided to examine as potential additions to our portfolio. Although the companies analysed may tick most of the boxes, if the margin of safety is not considered sufficient, we will not initiate a position but rather monitor the stock.

In case we decide to initiate a position at any time, we will share an Investment Thesis memo. For any additions to existing positions we will update you through our Quarterly Portfolio Updates.

The below is an extract from our analysis on $SKY. For the full write-up (in-depth analysis of financials, industry, valuation and more) you can subscribe to our newsletter and get a 40% discount if you subscribe by 28th of February.

Let's dive in.

------------------------------------------------------------------------------------------------------------------------------------------------

1.KEY FACTS

Description: Skyline Champion Corporation (“SKY”, “Skyline”, and “Company”) offers a leading portfolio of manufactured and modular homes, park model RVs, accessory dwelling units (“ADUs”) and modular buildings for the multi-family and hospitality sectors and is considered the second largest player in the industry. The Company employs ~8,400 people and operates through 37 manufacturing facilities in the US and 5 in Canada and 31 sales centers.

Key Financials: Over the period FY15 to Q3’FY23, the Company depicted a revenue Compound Annual Growth Rate (“CAGR”) of 19%, reaching a Trailing Twelve Month (“TTM”) revenue of c. $2.7B and operating income of $566M (margin of 21%). SKY has cash and cash equivalents of $712 million compared to long-term debt amounting to $12 million.

Price & Market Cap (as of 21st February 2023): Its market cap is $3.9 billion with a 52-week high of $73.4 and a 52-week low of $43.04, whereas it currently trades at $68.30.

Valuation: SKY trades at a Next Twelve Month (“NTM”) EV/EBITDA of 9.4 (3 Year average of 14.1) and at a NTM P/E of 17.2 (3 Year average of 26.8).

Note: The Company’s fiscal year (“FY”) is a 52- or 53-week period that ends on the Saturday nearest March 31 (e.g. FY 22 ends on April 2, 2022).

2.BUSINESS OVERVIEW

How SKY was formed?

Skyline Champion Corporation was formed through the merger of Skyline Corporation and Champion Enterprises LLC (parent of Champion Home Builders) in 2018. Champion contributed their shares to Skyline Corporation in return of 47.8M shares in Skyline Corporation representing 84.5% of the common stock of the combined entity.

At the time, Skyline Corporation was the 4th player in the manufactured housing with a market share of 3% whereas Champion was the 2nd largest player with a market share of 14%. Upon the merger the new company had a market share of 17% whereas the current market share is estimated at 20.4%. Both companies have history that goes back to 1950s and with their combined forces and experience, SKY managed to remain a leading company while gaining market share.

Since the formation of the new Company (June 4, 2018) until 21st February, 2023, the Company delivered total returns of 104% (estimated CAGR ~16%).

Product offering

The Company has leading portfolio of manufactured and modular homes, park model RVs, accessory dwelling units (“ADUs”) and modular buildings for the multi-family and hospitality sectors. These are effectively affordable housing options compared to the on-site built houses.

SKY has well-known brand names in the factory-built housing industry including Skyline Homes, Champion Home Builders, Genesis Homes, Athens Park Models, Dutch Housing, Atlantic Homes, Excel Homes, Homes of Merit, New Era, Redman Homes, ScotBilt Homes, Shore Park, Silvercrest, and Titan Homes in the U.S., and Moduline and SRI Homes in western Canada.

The strength of its brands is justified by the America’s Most Trusted® Manufactured Home Builder award that on January 2023 was awarded to Skyline Homes for three years in a row. At the same time Genesis Homes and Champion Homes were also highly ranked. The research for this award is based on 40,000 consumers shopping a manufactured home.

The affordable housing options are cheaper than traditional housing because they are built indoors eliminating weather delays and due to the standardized process that enables manufacturing efficiencies as well as the ability to buy raw materials in bulk achieving lower prices.

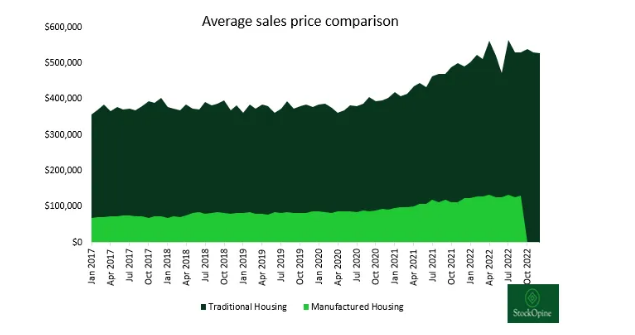

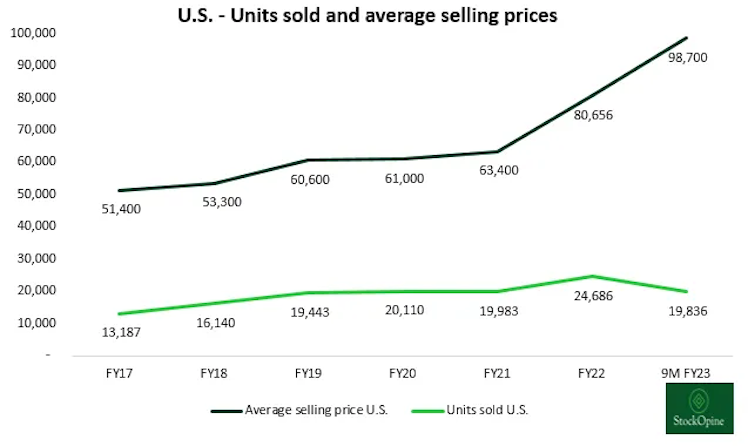

What do we mean cheaper? Well, using the latest available data from Census Bureau the average price for a traditional new home sold in Dec 2022 was $528,400 (including the land) whereas for new manufactured home the average price in Sep 2022 was $130,400 (without land). The below graph shows the price differential since 2017.

Source: Census Bureau, StockOpine analysis. Note: Data for Oct-Dec 2022 is not available

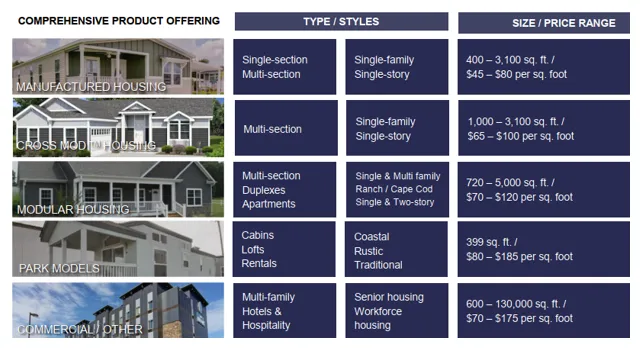

Housing types

Manufactured homes were previously known as mobile homes until the introduction of the HUD code in 1976 when federal standards were introduced regarding Design and construction, body and frame requirements, thermal protection, plumbing and electrical, fire safety and energy efficiency. Their general size ranges from 400 to 4,000 square feet. Manufactured homes are constructed inside climate-controlled building facilities and can be built on either a movable foundation (pier and beam) or permanent foundation (crawl space, basement, and slab) with each type having its own merits in terms of affordability, time to build, seismic activity, floods, heavy frost and wind resistance.

Modular homes are similar in how they are constructed with the key difference that they don’t follow the HUD code but rather all applicable state and local building codes (like traditional site-built homes).

Park model RV resemble mobile homes or tiny houses and can’t have more than 400 square feet size in their floor plan. They are usually temporary homes (seasonal use) created for trailer park settings. These are regulated under the RV Industry Association.

ADUs are a secondary house or apartment that shares the building lot of a larger primary home and cannot be sold separately, however it can offer an extra source of income through rent or to house a family member. Think of a newly graduate who may not be able to afford a new home. ADUs fall under the zoning rules and regulations of each area and although in general these rules are strict about ADUs, many municipalities are encouraging ADU construction with streamlining zoning and permitting thus making ADUs an attractive and affordable option.

Source: SKY Investor Presentation, May 2022

It is worth noting that the majority of SKY’s manufactured products are in accordance with the rules and regulation of the U.S. department of Housing and Urban Development (“HUD”) and are timber framed. Per the latest 10Q, 88% of US sales were derived from manufactured HUD code homes.

Distribution network

SKY’s factory-built homes are distributed through a network of independent and company-owned retailers, community operators, government agencies, and builder/developers. The majority of home shipments (>90%) is through independent distributors/retailers.

Homes sold to retailers are transported to a retail sales center or directly to the home site whereas homes sold to builders and developers are generally transported directly to the home site. Most of the retailers and builders/developers are located within a 500-mile radius to the Company’s manufacturing facilities resulting to cost efficiency and better prices.

It shall also be noted that SKY is one of the few approved manufactured homebuilders for the Federal Emergency Management Agency (“FEMA”) and provides housing assistance requirements following natural disasters and other housing emergencies. The most recent order was received on Feb 2022 for houses worth c. $200M to be completed until September 2022.

SKY also offers the construction services to install and set-up factory built homes by operating home retail business through Titan Factory Direct (Florida, Georgia, Louisiana, North Carolina, Oklahoma, and Texas) and through the 12 Factory Expo retail centers acquired in July 2022 from Alta Cima Corporation. In total, the Company has 31 sales cent rs $. Retail sales are gross margin accretive and the Company seems to be keen to enhance this sub segment.

“As retailers, I think, phase out of the business, there's a lot of aging retailers, there's, a lot of locations and geographies that we can meet, especially more digitally. I think there's, definitely expansion opportunities into retail. Should retailers want to retire or exit the business in some way.” Mark Yost, CEO

Additionally, the Company offers transportation services to manufacturing housing and other industries through its subsidiary Star Fleet Trucking, a logistics business specialized in manufactured homes and RVs.

The end-customers can be people who buy an affordable house (Millennials and Baby Boomers are key buyers), corporations (i.e. need park model RVs for resorts, campgrounds) as well as REITs that own the land and fill it with HUD code homes. Obviously, the increasing rates could impact sales to REITs which are generally highly levered and thus might cut back on their spending. Currently though, there are no such signs.

“We saw strong year-over-year growth in shipments during the quarter to our community REITs and builder developer channels. Additionally, orders from communities and builders were healthy as backlogs of both of those channels grew sequentially from the second quarter levels.” Mark Yost, CEO

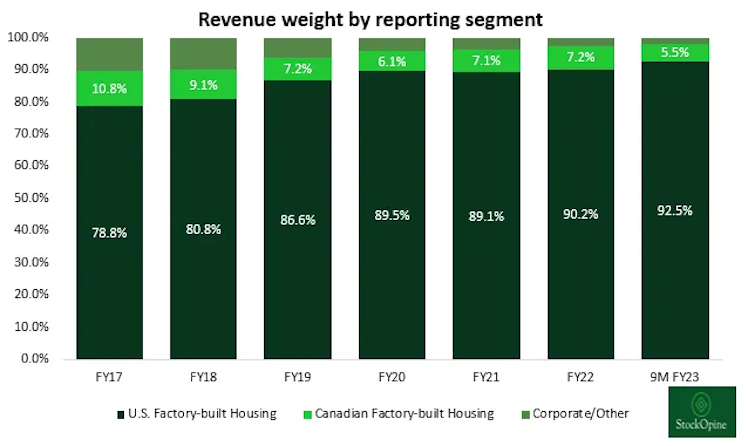

Reporting segments

The Company has 3 reporting segments, namely, U.S. Factory-built Housing, Canadian Factory-built Housing and Corporate/Other (which is immaterial to total revenue). Corporate/Other includes the transportation services of Star Fleet Trucking and intersegment eliminations.

Source: SKY 10K filings, StockOpine analysis

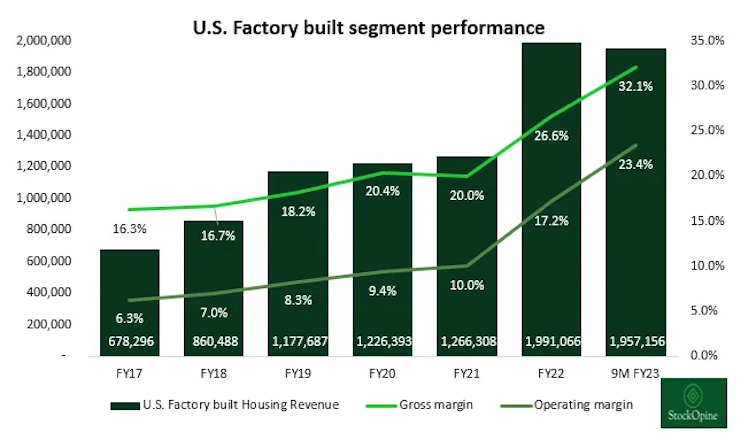

U.S Factory built Housing includes manufacturing and retail housing operation and accounts for 92.5% of sales or $1.96B in the 9M FY23 (90.2% in FY22). The average operating margin for the segment since FY17 until today averages at 11.7%, whereas the current (9M FY23) margin stands at 23.4%.

Source: SKY 10K filings, StockOpine analysis

The improved operating margin is effectively a result of an improved gross margin in FY22 and 9M FY23. Gross margin jumped from 20% in FY21 to 26.6% in FY22 due to operational efficiencies, better leverage on fixed manufacturing costs and higher prices as a result of increasing input costs, whereas for the 9M 2023 it further increased to 32.1%, a result of higher volumes (efficiency), higher prices and sales to FEMA for which prices are higher due to additional specification needs.

Source: SKY 10K filings, StockOpine analysis

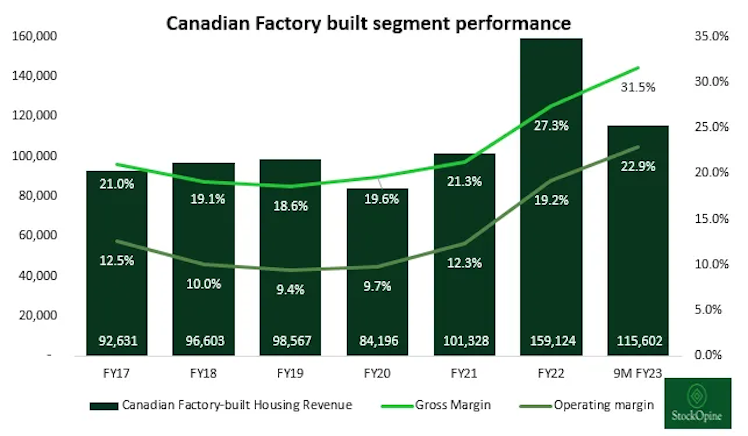

Canadian Factory built Housing is solely manufacturing operations and accounts for 5.5% of sales or $115.6M in the 9M FY23 (7.2% in FY22). The operating margin for Canadian operations since FY17 until today averages at 13.7%, while the current (9M FY23) margin stands at 22.9%. The reason for higher margins is the same as for US operation, i.e. improved gross margin driven by effectively the same reasons (efficiencies and price increases).

Average prices for Canadian homes are higher than US homes (at least 30%) whereas units sold p.a. do not exceed 1,500.

Source: SKY 10K filings, StockOpine analysis

In an aggregate basis the operating margin of SKY exceeds Cavco Industries (“Cavco”) for the years FY21 onwards which demonstrates better leverage gains when volume has increased due to strong demand (more in the “Industry” section).

Manufacturing

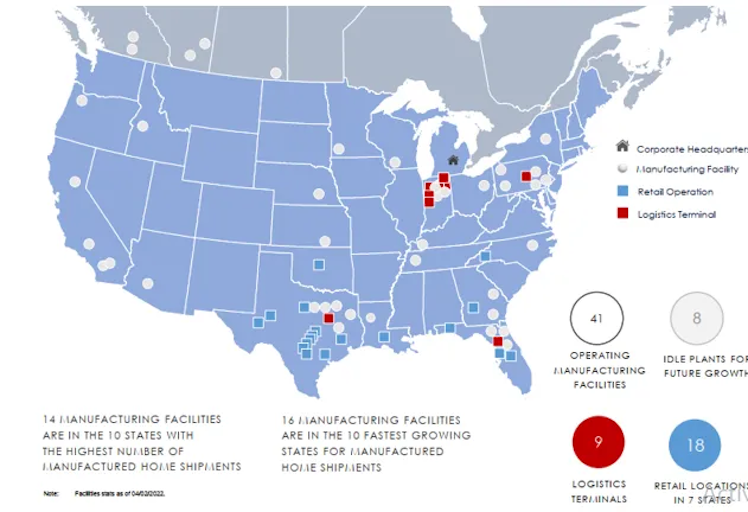

SKY runs 37 (36 in FY22) manufacturing facilities in the US and 5 in Canada whereas the majority of those facilities are company owned. Additionally, the Company owns 8 idle manufacturing facilities that give the ability to increase capacity as demand expands.

The manufacturing footprint further shows the position of the Company within the industry. In FY22 it had 36 US facilities out of the total 141 in the US (i.e. 25.5%) compared to 26 (27 currently) of Cavco.

It shall also be noted that the Company continuously strives for streamlining facilities’ operations and also invests in automation technology that will reduce material waste, labour requirements and improve precision on the construction process.

Source: SKY Investor Presentation, May 2022

Production of a manufactured home takes approximately 90 days but lead times were extended in the last couple of years due to supply chain disruptions and increase in backlog. Backlog starts to normalise, falling from $1.6B at the end of FY22 to $532M as of 31 December 2022 due to cancellation of orders by retailers as an attempt to optimize their inventory, higher production rates and lower net orders.

“Over the past few quarters, we have seen significant progress in normalizing our backlog because of stronger production capabilities, dealer destocking inventories and easing of supply chain challenges.” Mark Yost, CEO

Raw materials

The primary components of manufactured homes include lumber, plywood, OSB, drywall, steel, floor coverings, insulation, exterior siding (vinyl, composites, wood and metal), etc.

SKY sources its raw materials from a large number of suppliers eliminating supply risk. The prices of certain materials such as lumber, insulation, steel, and drywall can fluctuate significantly with lumber and related products experiencing significant cost increases in fiscal 2022. Despite these increases the Company was able to pass higher input costs to customers justified by the higher gross margin (see earlier section) and the higher volumes showing pricing power.

Financing

Financing is a critical component of a decision to buy a home and the type of home. In general the financing process for factory-built homes is different than traditional site-built, has more complications and types of funding and typically unfavorable terms such as higher fixed rate or upfront payment requirements.

Progress is made and is worth noting the financing programs that were rolled in 2020 (Fannie Mae - MH Advantage® and Freddie Mac - CHOICEHome®) specifically for homes built under the HUD code and subject to home features/specifications people can get lending terms similar to those for site-built homes. The Genesis Brand of SKY provides such homes eligible for these programs.

On the Commercial side (i.e. for independent retailers financing) floor plan financing is used or other financing agreements. Floor plan financing is when the financing institution provides the retailer with a loan for the purchase price and has the home as a collateral. Lender also requires SKY to enter to a separate repurchase agreement which obligates SKY to buy back the home at declining price if retailer defaults. Once the end customer buys the home, this obligation is removed.

Contingent obligations for SKY as of 9M FY23 are $399.4M but this risk is mitigated by the resale value and the large number of retailers. For FY22, 39% of sales to independent retailers were financed through floor plan agreements, while 61% under other financing agreements or cash.

Although it may sound scary, at least the credit institution should be better in doing the credit checks and the Company receives the cash earlier (5 to 10 days after a home is sold). In contrast to SKY, Cavco (#3) and Clayton Homes (#1 - subsidiary of Berkshire Hathaway) have in-house financing units, a strength for their business by making financing to their customers easier.

The losses incurred on repurchased homes have been insignificant in recent periods whereas the reserve for estimated losses under repurchase agreements stands $2.6 million at December 31, 2022 which approximates to 0.7% of the total balance.

This completes the Business overview of $SKY. If you made it up to here you will love the full write-up.

---------------------------------------------------------------------------------------------------------------------------------------------------------

Disclaimer: The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision.

stockopine.substack.com

Skyline Champion Corporation – A Compelling Investment Opportunity

Every month we share 2 write-ups on companies we decided to examine as potential additions to our portfolio. Although the companies analysed may tick most of the boxes, if the margin of safety is not considered sufficient, we will not initiate a position but rather monitor the stock.

Already have an account?