Trending Assets

Top investors this month

Trending Assets

Top investors this month

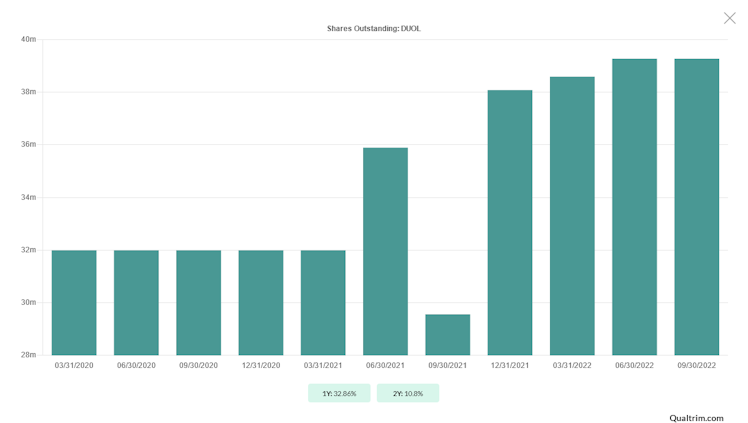

$DUOL Insanity

Sometimes I think companies go public for the sole reason of fleecing investors. While I think Duolingo is a great platform I think it's very hard to defend these two charts:

Stock-based comps well exceed free cash flow. While this is not entirely something new it can also be paired with the dilution.

Duolingo is just destroying any ownership of its business. The company has a lot of promise especially with its expansion into new verticals of education but this dilution is just gross.

Already have an account?