Trending Assets

Top investors this month

Trending Assets

Top investors this month

Ally Financial: A Clearer Roadmap

This is an extended preview of today's write-up, exclusively for Commonstock readers. To read the remainder of the post, please subscribe to the TSOH Investment Research service.

From “Past The Peak” (speaking about Ally’s auto loan book): “Is that sufficiently conservative? As always, it’s very difficult to say with anything close to certainty. Personally, as discussed in the deep dive, I take comfort in how this asset class performed during other difficult periods… That said, the world changes and this time may be different (for example, Ally’s shift to slightly higher risk content in auto). I think that concern may be overstated (properly accounted for in reserves), but time will tell whether I’m mistaken.”

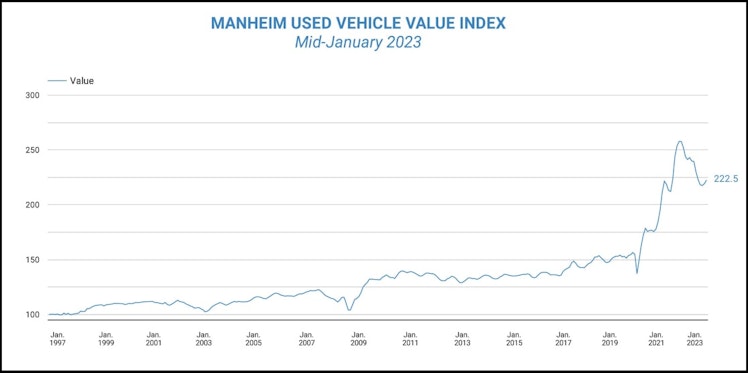

Ally Financial reported its Q4 FY22 financial results on January 20th, and I think it was a big step in the right direction; specifically, management did a good job of addressing some important topics that speak to the current state of affairs in the business, in addition to laying out a roadmap for how they plan to navigate the next 12-24 months. To be clear, a difficult environment still lies ahead for Ally in 2023. After a period of rapidly rising used car prices, we’re now seeing a significant (albeit unsurprising?) move in the other direction. In December 2022, the Manheim Used Vehicle Value Index was down ~15% YoY - the largest decline in the 25+ year history of this data set. (That said, as you can see below, the value of the index as of mid-January 2023 is still meaningfully higher than where it stood in early 2021.)

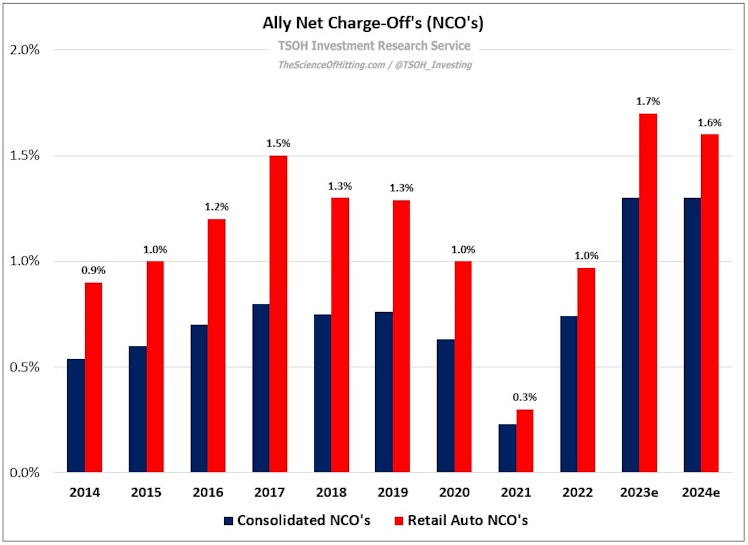

In the fourth quarter, net charge-off’s (NCO’s) in Ally’s retail auto business increased to 166 basis points, pulling full year auto NCO’s to nearly 1% of outstanding loans. As shown below, the company expects NCO’s to remain elevated in each of the next two years, at roughly 1.6% - 1.7% of average loans (and pulling consolidated NCO’s to heights unseen in the past decade).

There are a few important points to address here.

First, a noteworthy assumption underlying the auto NCO estimate for 2023 is the future trend for used car pricing: for the year, management is assuming that used car prices fall another ~13% (a cumulative decline of ~30% from 2021 peak prices), which is more conservative / assumes a worse outcome than other industry estimates. (“The Manheim Used Vehicle Value Index is forecast to be down 4.3% YoY in December 2023.”) Second, Ally ended 2022 with $3.7 billion in consolidated reserves, equal to ~2.7% of average loans (~2x higher than their current estimate of consolidated 2023 NCO’s). Finally, given the decision to temporarily suspend share repurchases in the coming year, the company will also build up some incremental capital as we work through 2023 (rough guesstimate of ~$800 million). As those numbers suggest, management is approaching this period with some conservatism; given the importance of these assumptions, I think that’s a logical step.

And as discussed last quarter, credit risk should be considered in the proper context – specifically, with consideration for the price charged relative to the risk incurred. Retail auto origination yields at Ally were ~9.6% in Q4, up ~260 basis points YoY; as CEO Jeff Brown said at an analyst event in December, “we feel really, really good about the paper we're booking”.

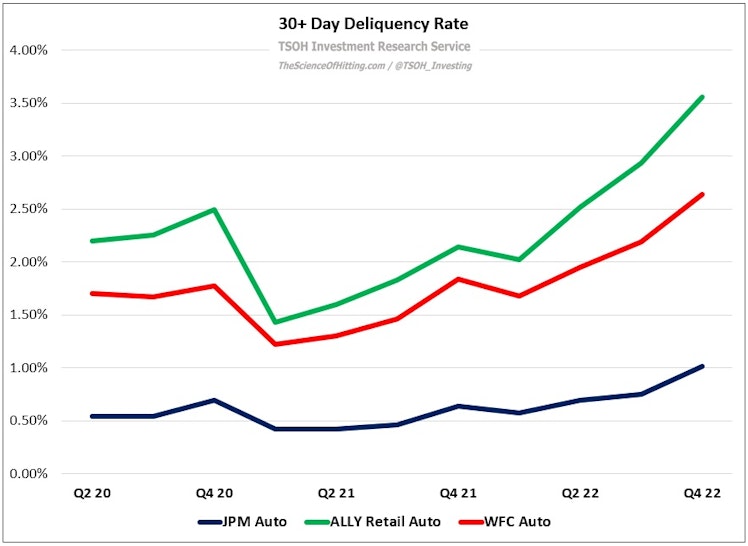

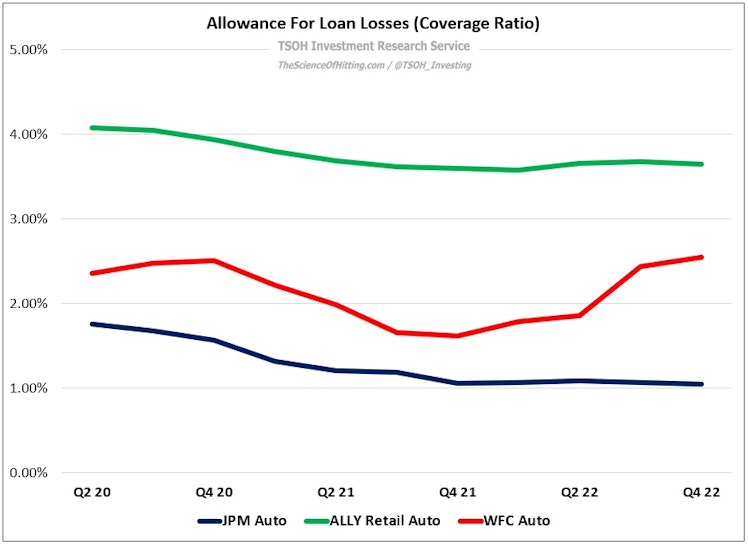

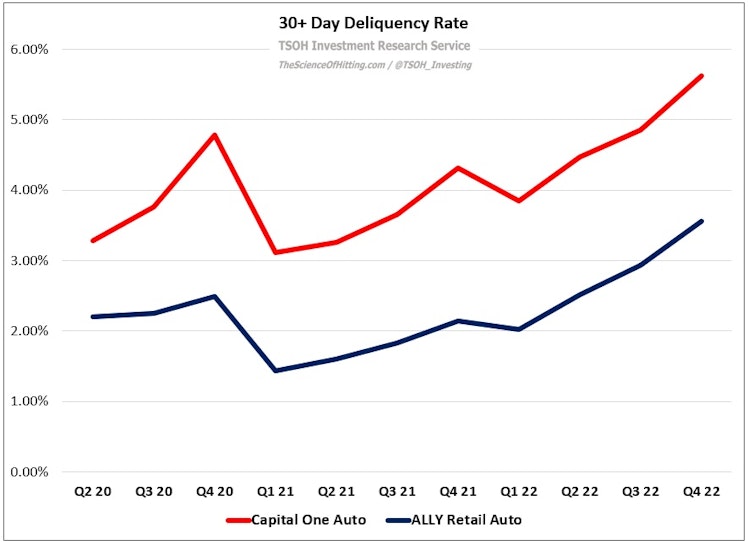

While it’s evident from metrics like NCO’s and the 30+ day delinquency rate that Ally holds a lower quality / riskier book than peers like Wells Fargo and J.P. Morgan, the allowance for loan losses (coverage) aligns with that reality.

Capital One is another interesting comparison: their auto loan book is similar in size to Ally’s (~$80 billion), and their 30+ day delinquency rate averaged ~4.7% over the past four quarters, compared to ~2.8% at Ally (with identical NCO rates in Q4); despite this, Capital One had ~$2.2 billion in allowances for auto loan losses at the end of Q4 FY22, or ~$900 million less than Ally. Long story short, it’s unclear to me from looking at some notable peers that Ally is being aggressive on its assumptions (at least relative to the industry).

(End Of Preview)

thescienceofhitting.com

Ally Financial: A Clearer Roadmap

From “Past The Peak” (speaking about Ally’s auto loan book): “Is that sufficiently conservative? As always, it’s very difficult to say with anything close to certainty. Personally, as discussed in the deep dive, I take comfort in how this asset class performed during other difficult periods… That said, the world changes and this time may be different (for example, Ally’s shift to slightly higher risk content in auto). I think that concern may be overstated (properly accounted for in reserves), but time will tell whether I’m mistaken.”

Already have an account?