Trending Assets

Top investors this month

Trending Assets

Top investors this month

Agora sending mixed signals

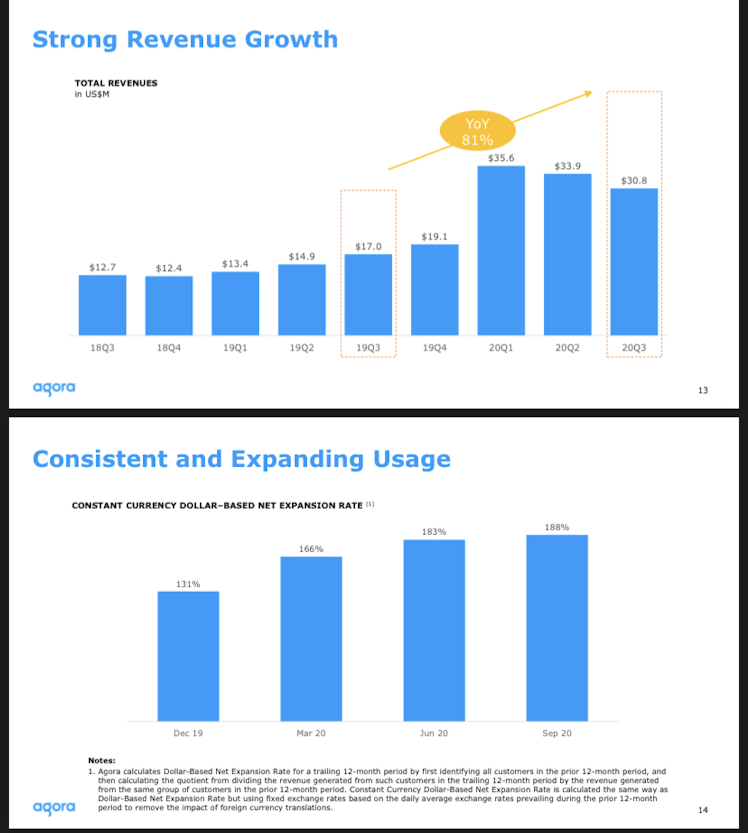

$API reported Q3 earnings, with a mix of good and bad news.

The good:

- Revenue growing 81% YoY — good albeit slowing down from original covid-driven boost

- Net expansion rate is a best-in-class 188% — the acceleration is a strong signal that their end customers are likely growing with Agora

The bad:

- Gross margins dropped from 69% last quarter to 62.5% as a result of expanding to markets with higher infrastructure costs

- Weak guidance on next quarter suggests that their post-covid growth may look less compelling

Still a believer here in the long-term value of real-time video infrastructure though it could be a slowdown in the next few quarters as growth post-covid will come down.

Already have an account?