Trending Assets

Top investors this month

Trending Assets

Top investors this month

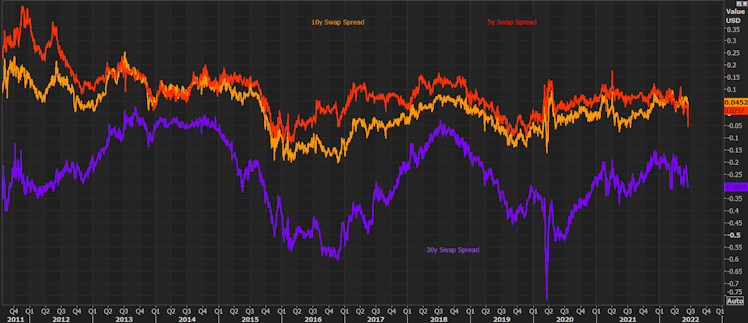

Swap spread and covered interest rate parity

A deviation in covered interest parity. This is most likely due to balance sheet (B/S) constraints, and Repo agreements could reduce B/S constraints however we are not seeing that. This leads me more to the idea that the probability to see a deflation period is high, as those B/S constraints are preventing participants from the arbitrage opportunity. The inability for those swaps to decompress is also telling, and shows that most B/S have been and never recovered after the GFC. Thus liquidity is systematically impaired.

Already have an account?