Trending Assets

Top investors this month

Trending Assets

Top investors this month

$12.2MFollowers

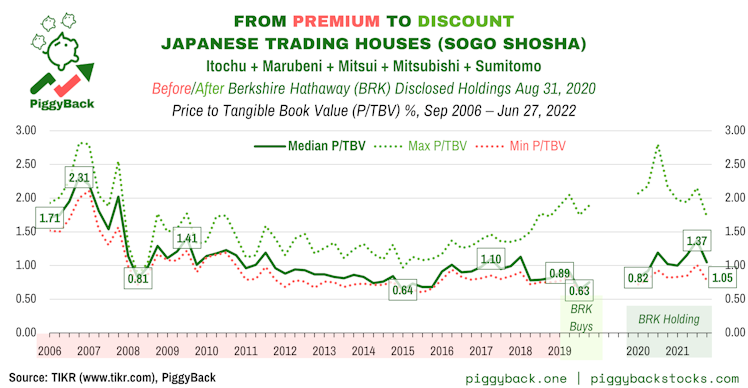

Big In Japan? - Berkshire's 2019– Bet On Japan Inc

It was August 31, 2020. U.S. value investor and businessman Warren Buffett’s insurance conglomerate Berkshire Hathaway $BRK.A $BRK.B sent out a press release. The heading may have surprised U.S.-focused Berkshire-watchers:

“Berkshire Hathaway acquires 5% passive stakes in each of five leading Japanese trading companies”

Berkshire had acquired stakes in Itochu $ITOCY, Marubeni $MARUY, Mitsubishi $MSBHF, Mitsui $MITSY, and Sumitomo $SSUMY. Via regular share purchases on the Tokyo Stock Exchange over “approximately” 12 months.

But why?

As businesses, $BRKA's Japanese trading houses are very exposed to the physical trading of commodities and goods. They are cyclical. They were already recovering from a cyclical commodities bear market of the mid-2010s before Buffett stepped in.

Notice how the ROE% follows commodities?

What about the price $BRKA paid?

Not surprising to the value investing community, Buffett can still wait for opportunistic discounts. Sogo Shoshas got there after the 2010s commodities bear market.

For our takeaways after "piggybacking" Buffett & Berkshire to Japan, please read this week's @piggyback Letter Buffett's Inflation Bet With The House(s)

Disclaimer: All readers are assumed to accept the full version disclaimer at the following link.

www.piggyback.one

LEGAL DISCLAIMER

This disclaimer covers PiggyBack's publications and all related communications. By accessing these publications and communications all readers are assumed to accept this disclaimer in full.

Already have an account?