Trending Assets

Top investors this month

Trending Assets

Top investors this month

$11.6MFollowers

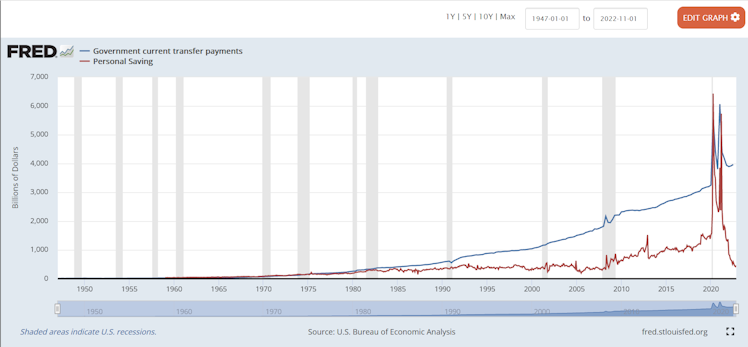

Chart of the Day - the pendulum swings

For all of those market-watchers out there that are calling for a recession, myself included, most are looking at the falling housing market, the negative ISM and ISM new orders data, and the rapid slowdown in autos that we are seeing.

On the plus side, as we just saw, the labor market, measured by the non-farm payroll or the JOLTS measure, still looks very tight. Admittedly the ISM employment and jobless claims measures do put some question into that labor strength though too.

Another chart you have probably seen shared is the rapidly declining savings rate. It has dropped to 2.4% which is the lowest of the last 60 years, even lower than in 2006 during that housing bubble and burst.

There is a stock vs. flow argument here though as you can see in the red line. This is the billions of dollars of savings, not the rate, and this number post Covid spiked to 6 trillion, 5-6x what it was before Covid. Thus, the rate of savings may be lower because the stock of savings, the amount of money in accounts, is higher.

There is another explanation too. Another outcrop of Covid was the government transfer payments to people. These payments doubled during Covid from 3 trillion to 6 trillion and have only pulled back to 4.

In fact, these payments remain at an all-time high and look set to move higher and not lower.

With the latest IRA and govt budget, money to individuals is going back up. The states got involved before the election too with states like California and Illinois sending payments to voters, err I mean residents, right ahead of the election to soften the bite from inflation.

These transfer payments, in addition to the stock of savings, can meaningfully soften the blow on the slowdown in the economy. However, not everyone is privy. Perhaps this is why this recession may feel like a recession of the top 5-10% and not like that of the wider economy.

Perhaps this may mean consumption holds up better than many, myself included, are thinking. This could also mean that inflation could be stickier than we are expecting given the expected falling growth.

It may also mean the Fed stays in play longer than the 50 bps more hikes that are expected in the market right now.

Stay Vigilant

#markets #investing #economy2023 #consumerspending

Already have an account?