Trending Assets

Top investors this month

Trending Assets

Top investors this month

Introduction

"So, how may investors navigate the impending rising rate environment? Historically, highly profitable, well-capitalized firms perform best when financial conditions tighten."

Taken from Institutional Investor (March 2022), this statement outlines an empirically proven strategy for successfully navigating the uncertainty of rising rates and inflation.

Google fits the description perfectly yet suffers from investor uncertainty and trades around a 52-week low. This (temporary) dislocation creates an opportunity for investors to buy a great business at a discounted valuation.

Thesis

- Google has demonstrated exceptional resilience through various economic environments, enabled by durable moats in its core businesses.

- Recent financial performance indicates continued strength; negative analyst revisions

create a catalyst for outperformance in the next year.

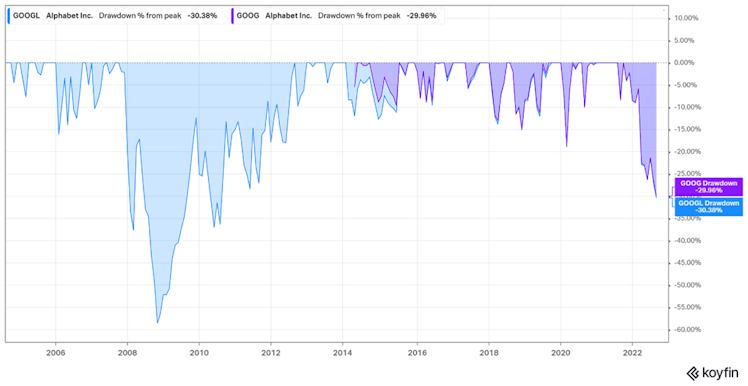

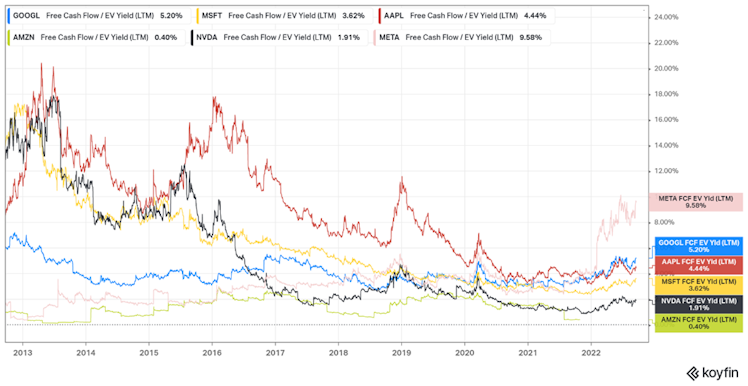

- A drawdown of magnitude and duration not seen in the last decade leaves Google trading at a discount to peers and nearly one standard deviation above its average FCF

yield dating back to 2004. This creates a great buying opportunity.

Resilience and Moat

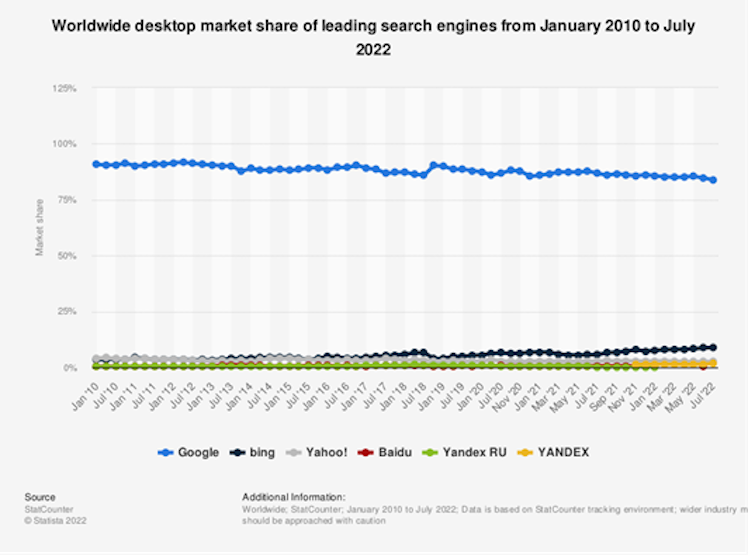

In twenty years, Google has reported just one quarter of revenue declining Y/Y. This type of resilience is enabled through a durable moat. Google Search has maintained monopolistic market share over the last decade, and there remains a lack of convincing catalysts for this to change.

**

**

Among the threats frequently mentioned are:

- Apple’s development of a search engine: While a possibility (though unlikely), it could actually be accretive to Google in the short-term. If Apple were to introduce its own default search, Google would recover the ~$15-20 billion it pays to Apple each year as free cash flow, which could drive a multiple re-rating.

- Regulatory action: Google has long been subject to regulatory probes, and several proposed acts pose a threat. However, in light of the long history of threats in this area and the slow pace of legislation, I believe nothing will materialize in the next year.

For YouTube, the advantage of an 800 million video archive of user generated content creates a tough hurdle for competitors to overcome. The traditional format also caters

to a different use case versus TikTok with longer form videos. Meanwhile, YouTube Shorts is proving to be a capable competitor with over 1.5 billion monthly users less than two years after its launch.

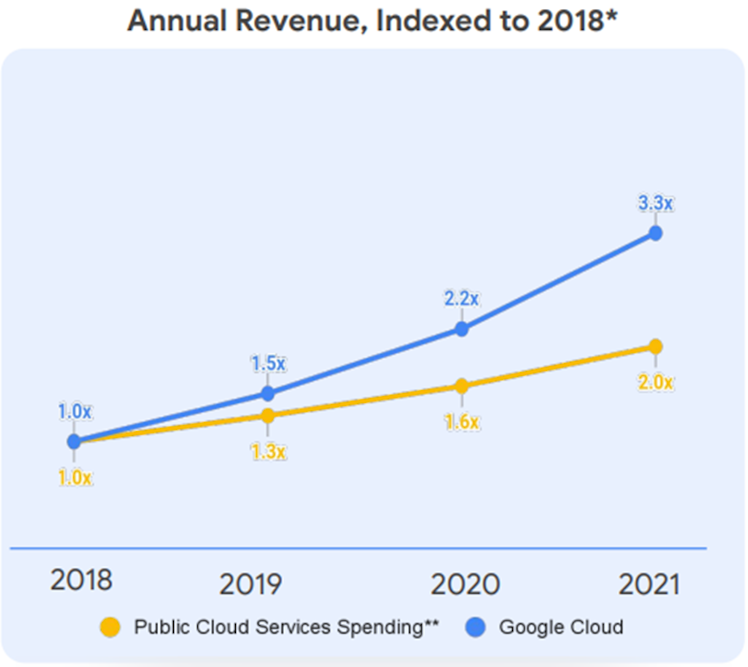

Google Cloud, though dwarfed by AWS and Azure, has demonstrated an ability to gain market share. The cloud transition remains in early stages, with spending expected to double by 2026. While a longer-term tailwind, Google Cloud’s performance continues to be strong and outpaced rivals in Q2.

**

**

Google’s core businesses hold sustainable competitive advantages, which should serve the company in an uncertain environment. Google Search and YouTube remain proven, high ROI advertising channels while Google Cloud benefits from structural tailwinds within cloud.

Revisions as a Catalyst

In the shorter term, a company’s performance against consensus estimates drives the stock price. Recently, analysts have revised EPS estimates for Google significantly downward:

- Q3 2022 revised from 1.49 to 1.27 (-15%)

- Q4 2022 revised from 1.67 to 1.41 (-16%)

- Q1 2023 revised from 1.50 to 1.33 (-11%)

- Q2 2023 revised from 1.61 to 1.39 (-14%)

Google's stock has dropped 30% compared to negative revisions of ~15% (multiple compression). Continued earnings outperformance coupled with a potential multiple re-rating (likely if it beats estimates) create catalysts for outperformance in the next year. Despite the economic environment, I believe Google has a great opportunity to beat estimates, particularly in light of the company’s strong Q2 performance, a period when many advertisers exhibited weakness.

Risks

On a one year horizon, the primary risks seem to be:

- Earnings weakness: While there is a possibility of growing weakness in advertising, I’m confident Google will, once again, prove resilient. History doesn’t repeat, but it certainly rhymes.

- Passive fund flows: Heavy weights in the NASDAQ and S&P 500 expose Google to passive equity outflows amid prevailing uncertainty. Predicting fund flows, however, is a difficult game to play; investing in resilient, highly profitable businesses at depressed valuations is my preferred game.

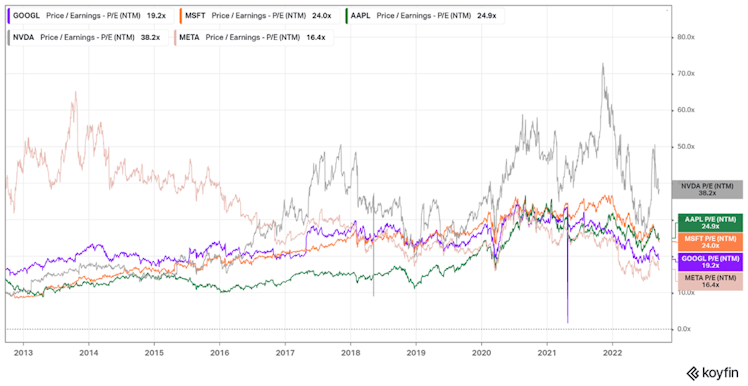

Valuation

Google is undergoing its largest drawdown in the last decade.

So, how much is the market asking for a piece of the business? Compared to peers and historical multiples, it seems reasonable. Reversion to the mean can be a powerful force in markets.

Conclusion

At its core, investing is simple: buy great businesses when Mr. Market offers a bargain. Google trades at a meaningful discount to peers and its historical average FCF yield, yet it remains one of the best businesses in the world.

Already have an account?