Trending Assets

Top investors this month

Trending Assets

Top investors this month

$12.6MFollowers

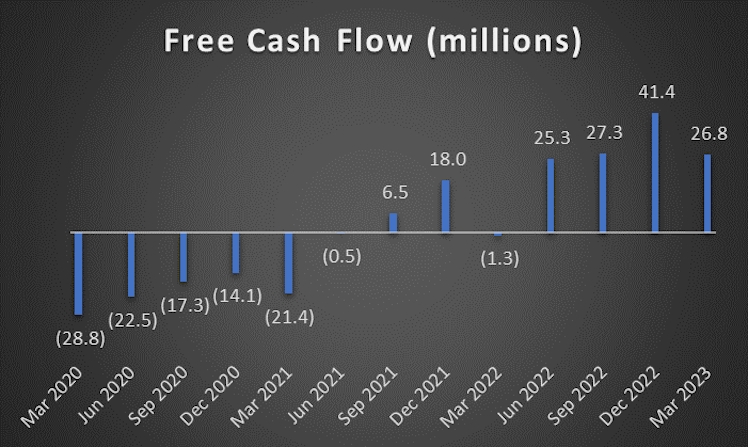

Shockwave Medical ($SWAV) Earning Recap

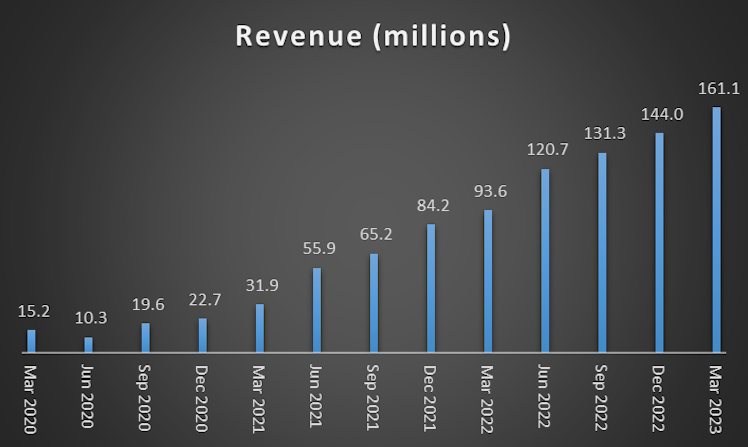

- Revenue increase 72% YoY

- Management increased FY guidance by 6%, from $670M at the midpoint to $710M, the latter representing 45% growth over FY22. I expect management to rise FY guidance each of the next two quarters as well.

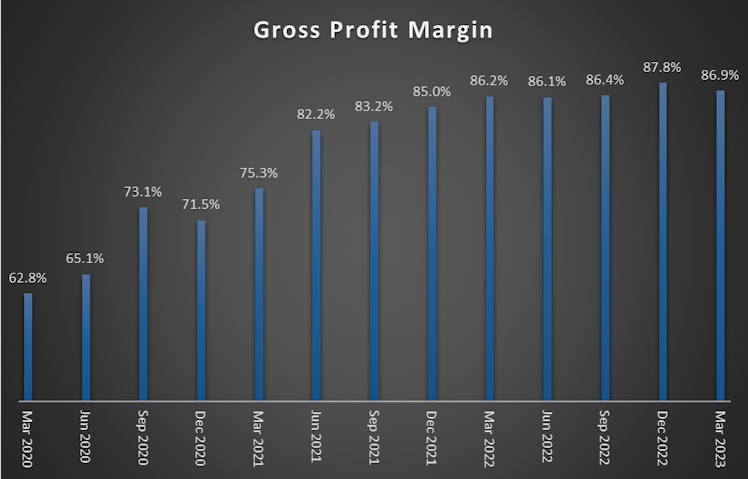

- Gross margins increased 70bps YoY

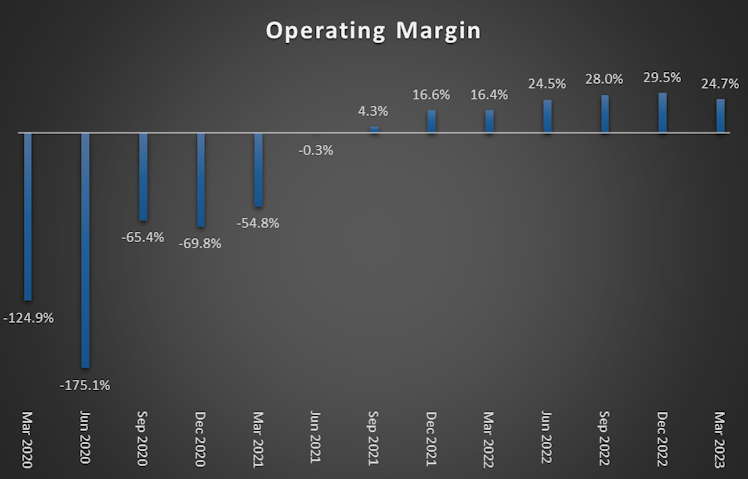

- Operating margin increased 830bps YoY

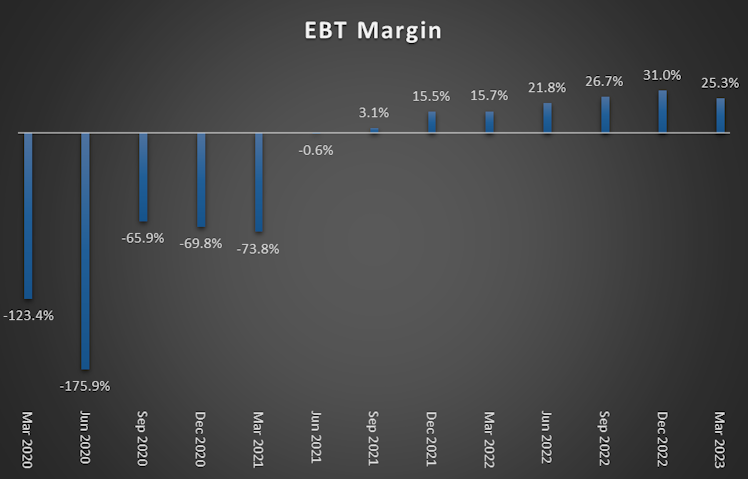

- EBT margin increased 780bps YoY

- FCF increased swung from -1.4% of revenue to +16.6% YoY, to $26.7M

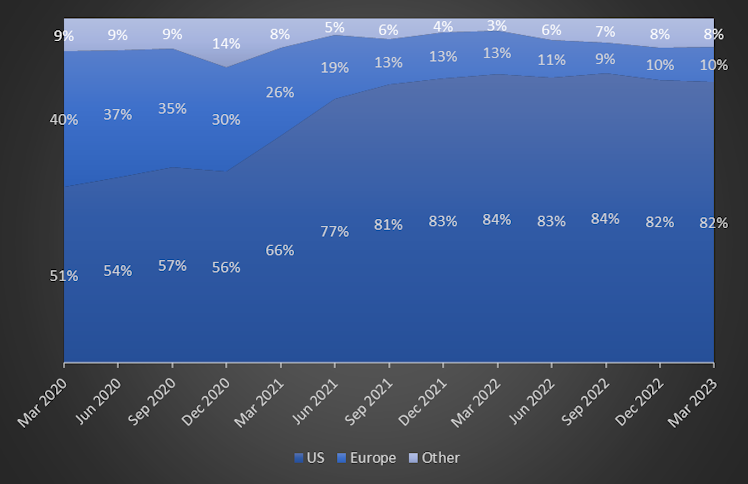

- I'm watching revenue breakdown by geography closely, particularly the Other category. It may not look like much but Shockwave's international expansion is a key growth driver, in particular Japan and China, which management expects to see results from in 2023. The US is obviously their bread and butter right now, up 68% YoY and 89% TTM vs. prior TTM, and Europe is strong as well (35% YoY, 30% TTM vs. prior), but Other was up 334% YoY and is now up 227% TTM vs. prior period.

- On the conference call, management reiterated that the rollout in Germany, Japan, and China is going very well. No actual numbers have been given yet so Other revenue is the thing I keep my eye on (until some of these areas start exceeding 10% of revenue and need to be broken out into their own demographic).

Already have an account?