Trending Assets

Top investors this month

Trending Assets

Top investors this month

Our Second Purchase announced...SHOP

@brianferoldi and I are announcing our second purchase for our "From Scratch" investing portfolio. The stock we'll be purchasing: $SHOP.

Shares are down HUGE, but we're big fans of the business. @brianferoldi considers it high quality. I consider it Anti-Fragile. Here's what you need to know.

The company's mission -- "to make commerce better for everyone," checks all the boxes: it is simple, inspirational, and optionable. And it's important to note, it has also been tested in the past and remained squarely in the position as compass for company moves.

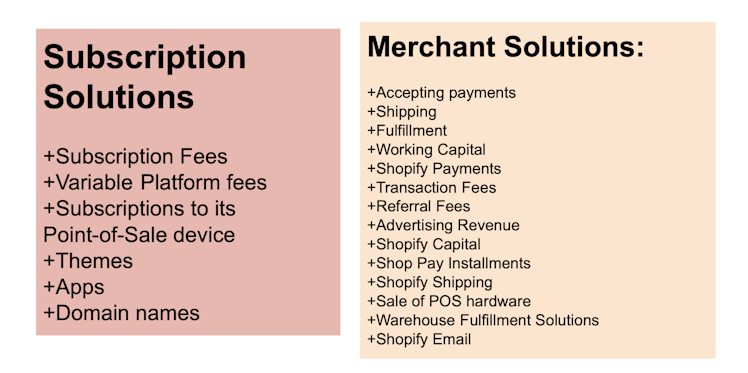

And a merchant can use the platform for...just about anything.

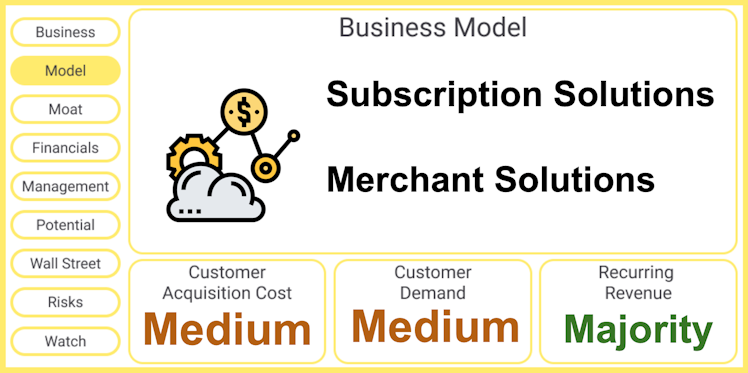

One huge thing we love about the company: dual income streams. Subscriptions have a flat rate, while usage-based merchant solutions grow as merchants grow.

What do these revenue streams actually mean?

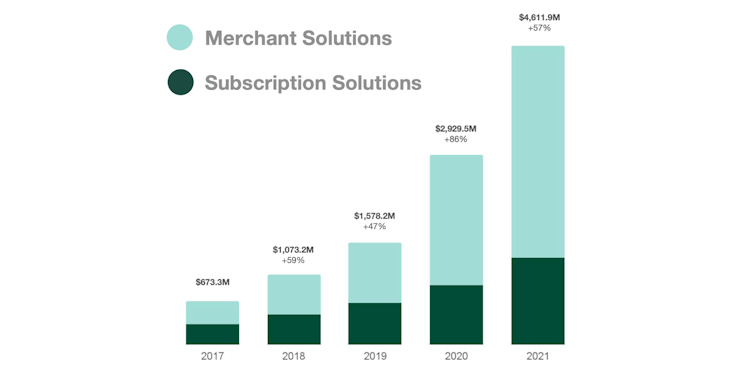

It's worth noting that merchant solutions are growing faster (no surprise, as merchants grow on the platform) but are lower margin. Recently, however, gross profit from merchant solutions eclipsed subscriptions.

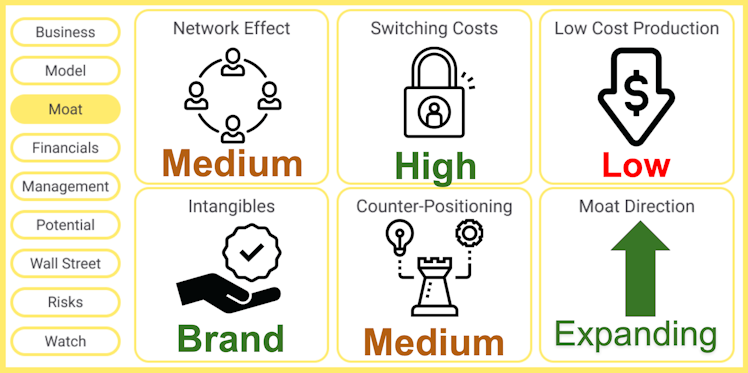

One thing we REALLY LOVE: we believe Shopify has varying levels of ALL FIVE MOATS that we evaluate. This is true for very few companies we've researched.

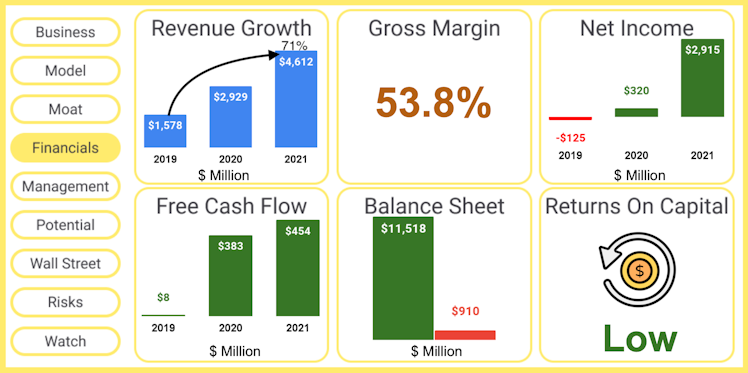

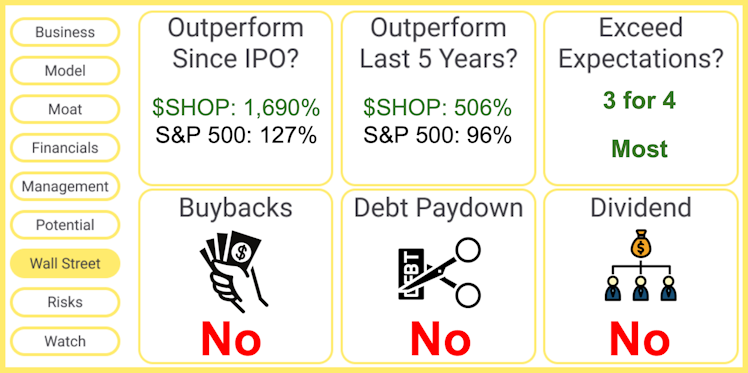

The results have been strong -- and the balance sheet is incredibly well-stocked.

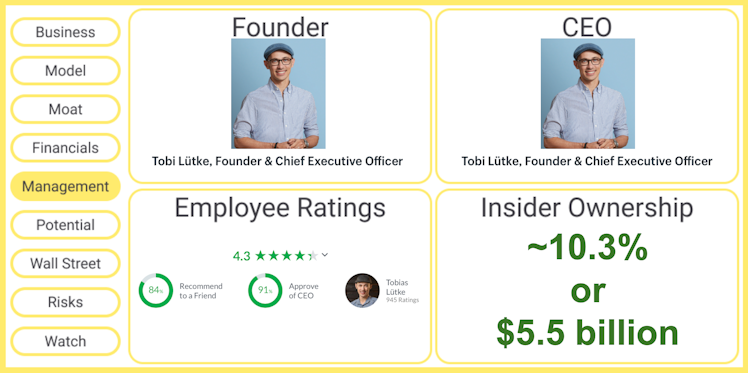

Culturally, there's a TON to like as well.

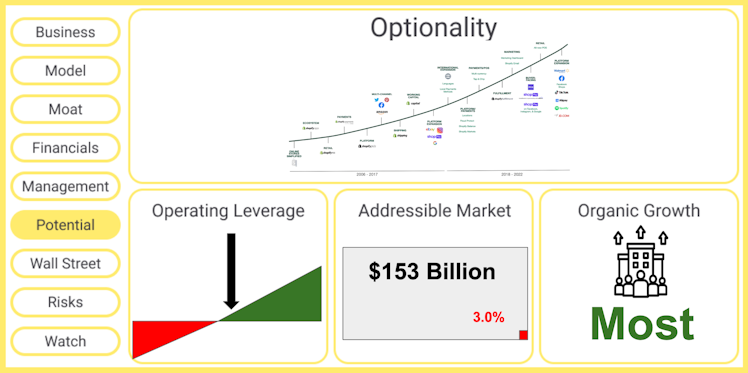

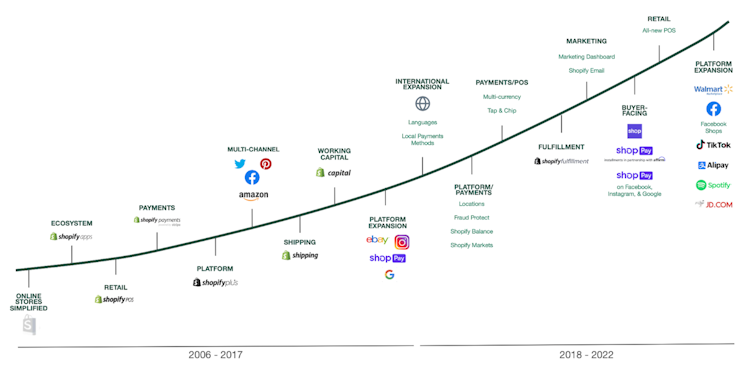

There's tons of room for the company to grow

And outside of Amazon, Tesla, Mercadolibre, as Sea Limited -- few companies have such a history of optionality.

And despite being down HUGE, it's still been a winning investment over the long-run.

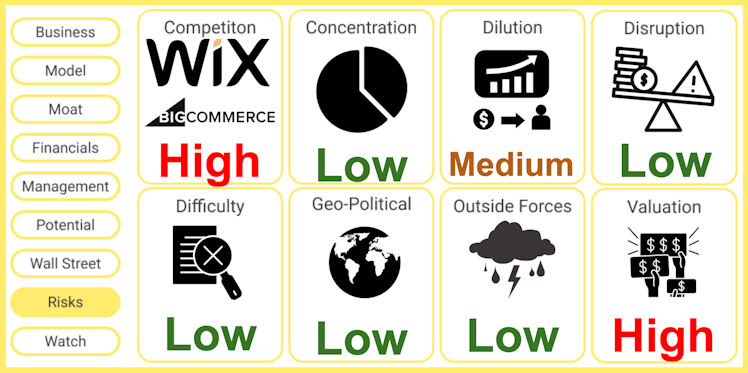

What about the risks? Here's what we see

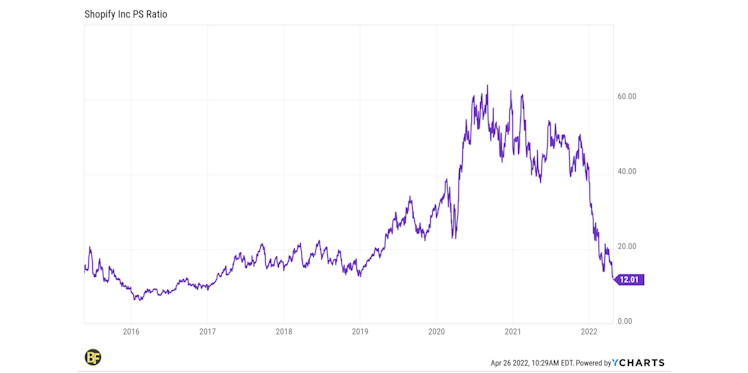

Now, we get a lot of questions about valuation. We really don't spend too much time worrying about it. But we do note that on a P/S basis, SHOP is well within its historical range.

Would you prefer to see all this in video form? We just released it here: https://youtu.be/E3VlixmyPGU

One final note: you may have noticed we haven't made our first purchase of $AXON. That's because Brian and I both have trading restrictions based on our work for The Motley Fool. As soon as we're cleared to buy shares of AXON (and SHOP), we'll be doing that.

What do you think of Shopify right now?

73%This is a GREAT deal

26%Still too expensive...

63 VotesPoll ended on: 5/1/2022

Already have an account?