Trending Assets

Top investors this month

Trending Assets

Top investors this month

Hello everybody. In this post i am trying to estimate the decisions of $ALPHABET managers. Enjoy!

MEASURING THE MANAGEMENT OF ALPHABET

INTRODUCTION

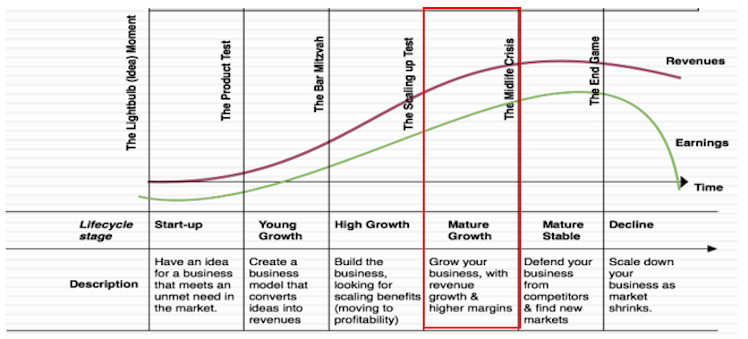

There is no good or bad CEO, there are CEOs that fit best during a specific time in a company. For example, when your company is young and growing fast, you want an overconfident CEO taking risks. But when your company has matured and declined then you need a CEO with calmer decisions.

THOUGHTS AND APPROACH

I often read on social media and hear in discussions that I should invest in companies with particularly good management, and when I ask them how they measure it, I don’t get a clear answer. In this post, I will try to assess the management team of Alphabet running a reverse engineering approach:

First, I will try to estimate in which Corporate Life Cycle Alphabet is, from the profitability metrics, reinvestment rate, capex, debt, and growth. Second, I will attach the appropriate profile of the CEO in this stage of business and finally, I will look at how the managers of Alphabet are disciples under these characteristics.

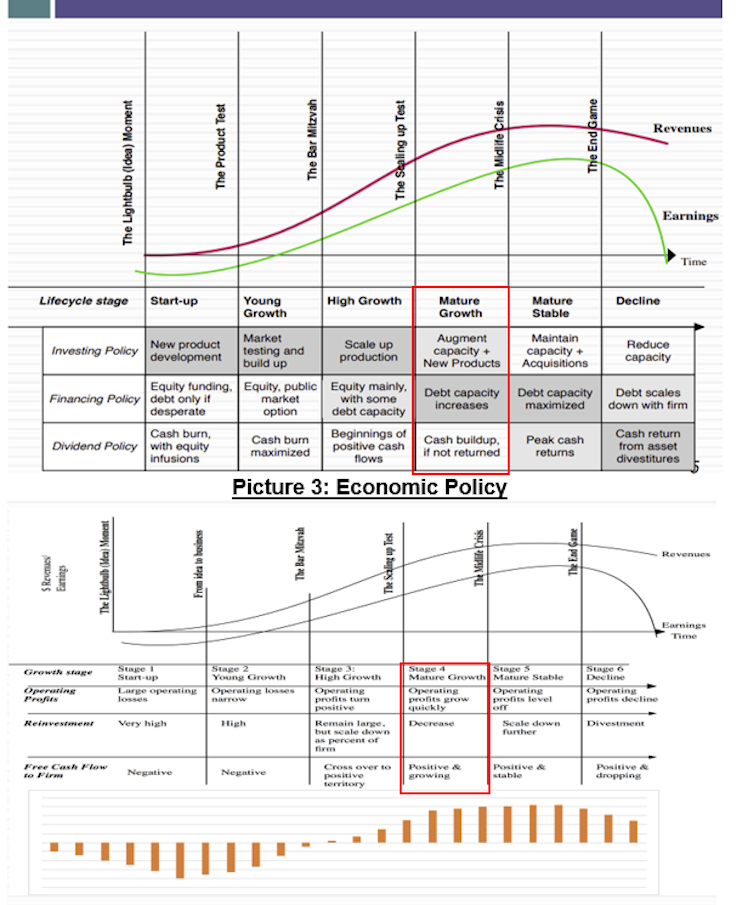

CORPORATE LIFE CYCLE

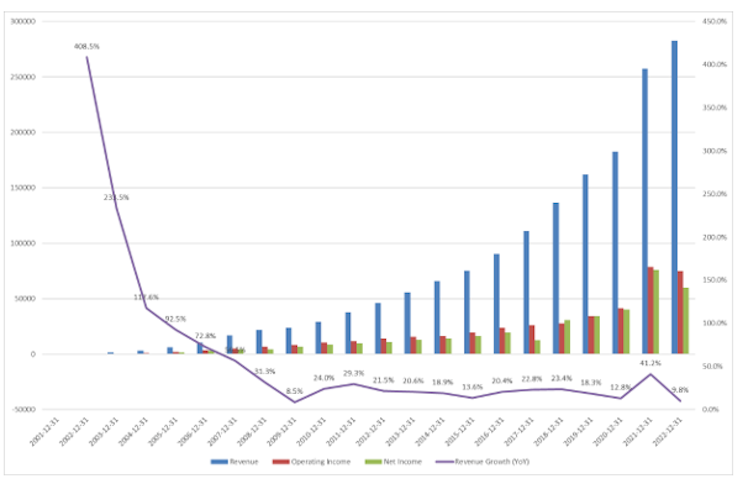

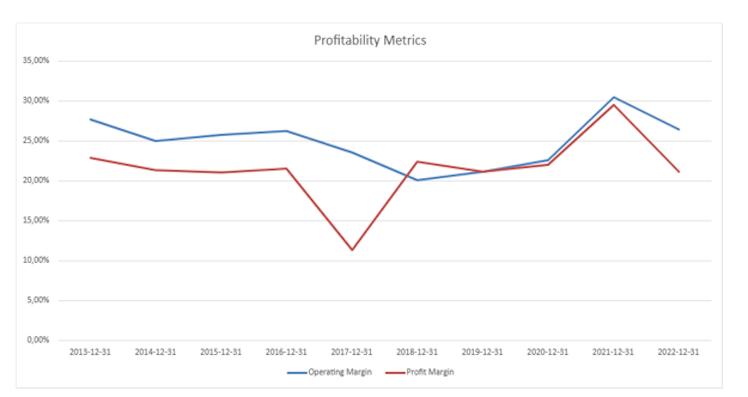

Revenues and Operating/Net Margins: As the diagrams show Alphabet has high revenues that are increasing, not as in the early years of the company, but are high with stable growth between 10% to 40%. Furthermore, looking at operating and profit margins is clear that are very high but stable (between 10% to 30%) which is very logical because is the biggest company in advertising and at the same time trying to compete in cloud services with Microsoft and Amazon. As a result, from revenue and operate/net margins perspective, Alphabet is on Mature Growth phase.

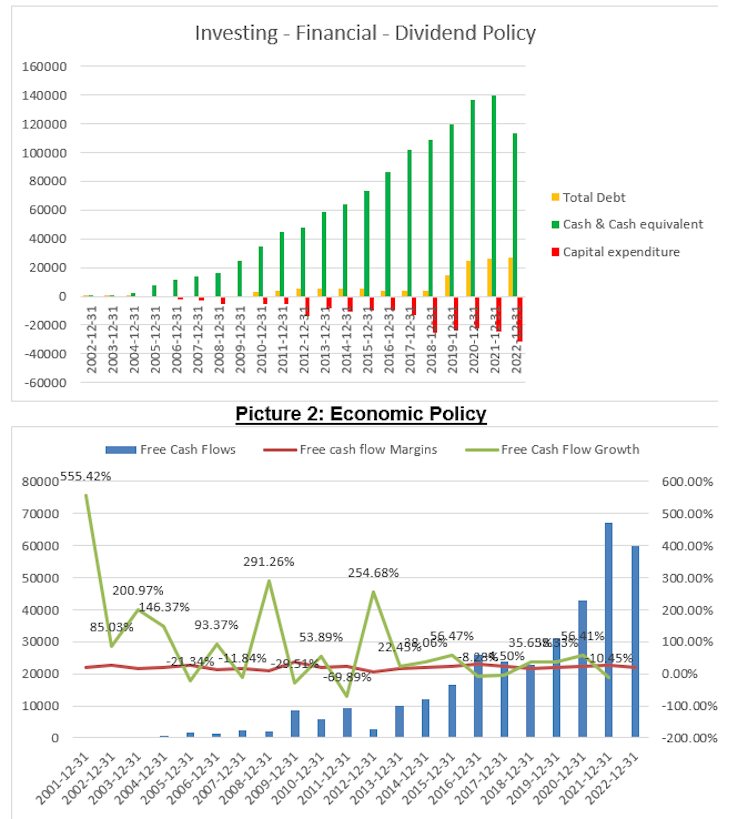

Economic Policy and Free Cash flows:

What we get from the diagrams below is that:

- Cash & cash equivalents are steadily increasing (with no dividends).

- Total debt was scant in the first years but after 2012 has started to increase.

- Capital Expenditures (Capex) also increase as the company ages.

- Free Cash Flows are positive and growing (stable), with margins of approximately 20%.

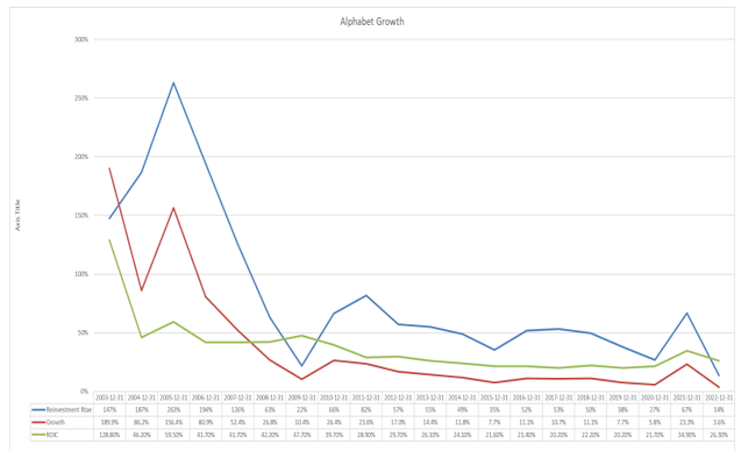

ROIC/Reinvestment Rate and Growth: It is obvious that in the first years of the Alphabet (until 2007) the growth was very high, which is logical because as a young company, you reinvest most of your money and ROIC increasing. But as the years passed, the reinvestment rates are decreasing and ROIC has been almost stable, with a growth (on average) of 10%. However, ROIC on average is 25% and the WACC for Alphabet is approximately 12% which means that the company creates value from its business model.

(Note: I often read that as an investor I should look for companies with high growth which is wrong. An investor needs growth that creates value and derives when ROIC > WACC)

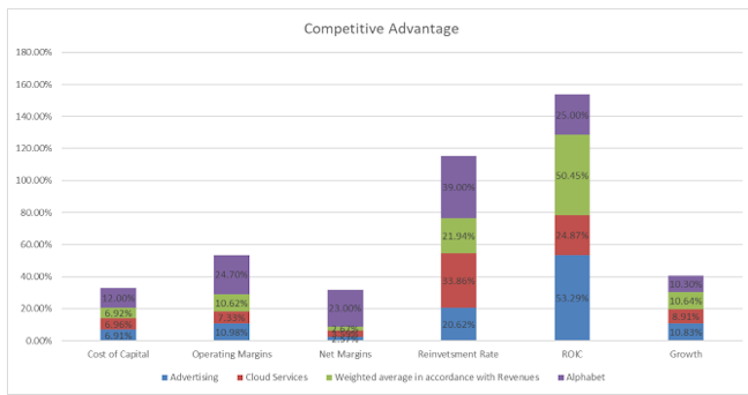

Competitive Advantage: Looking at the revenues from the last 10K, Alphabet is 85% advertising, 10% cloud service, and 5% others (Hedging, Google stores, pixel, etc.) To make the calculation easier I will attach 5% to the advertising sector and I will behave to Alphabet as a company that is 90% advertising and 10% cloud services. Below you will find a diagram where I have measured the average cost of capital, operating margins, net margins, reinvestment rate, ROIC, and growth for the advertising and cloud services sector but also for Alphabet.

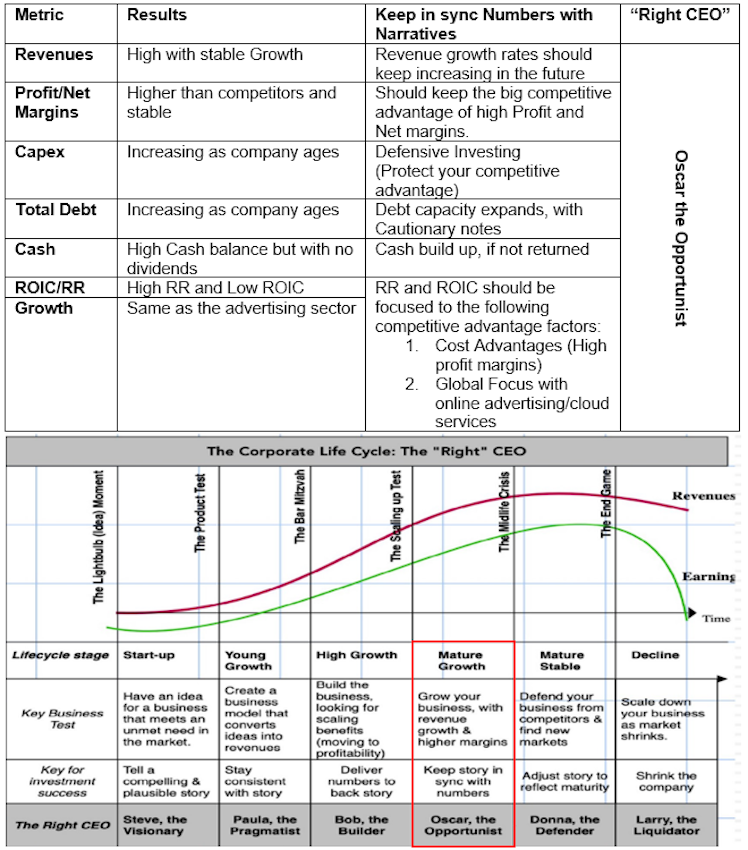

PICKING THE “RIGHT” CEO

Alphabet is a company where revenues are stable but increasing at a high rate and at the same time has higher operating and net margins in comparison to the other two sectors (24% vs 10%). On the other hand, to achieve high and stable margins should reinvest a lot of money, approximately 40%, with a low Return on Invested Capital relative to the two sectors (25% vs 50%). As a result, and looking at the last 5 years, the company has grown at the same pace as the overall advertising sector.

MEASURING THE MANAGEMENT TEAM

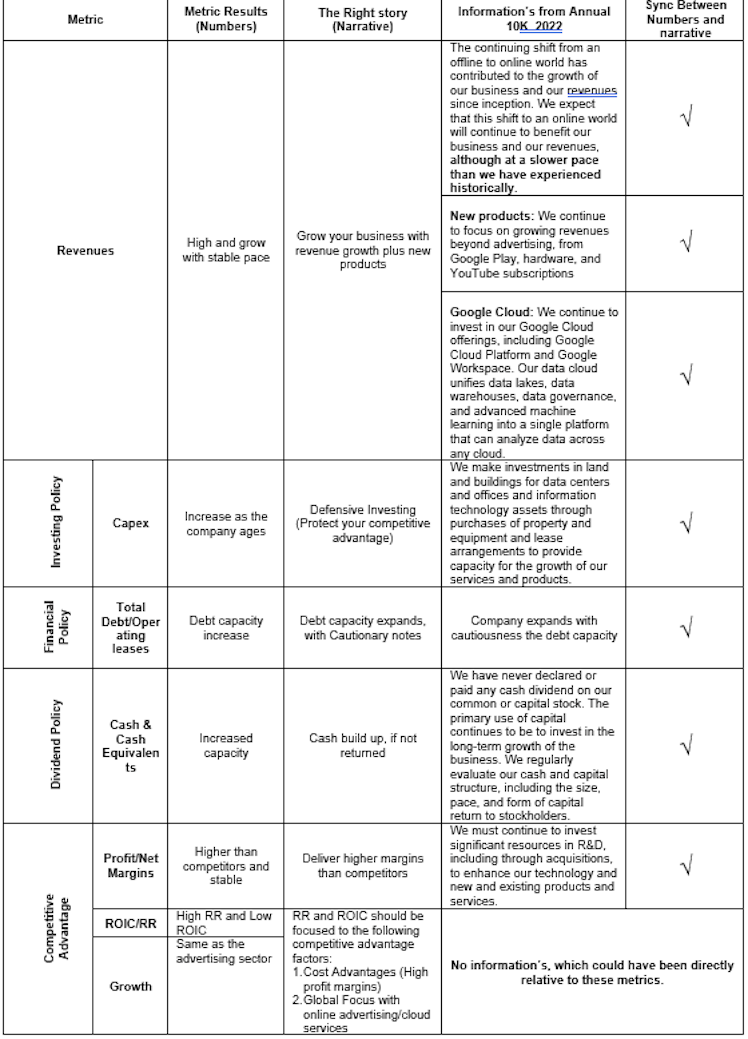

Now that we have finished with the number's (financial metrics), the “Right” CEO is that person who seek for opportunities to the market (for example Bard AI tool, healthcare services, expanding advertising services, cloud centers etc.) and trying to synchronize the narratives with the numbers. Below, i have a table that I illustrate some information’s from Annual 10k 2022 which prove that managers are in synchronize between numbers and the appropriate story for a company, in a Mature Growth phase.

CLOSING THOUGHTS

I believe that a connection between story and numbers can derive efficient results when combined correctly. My initial thought was to run a reverse engineering approach where I measured specific financial metrics that gave me a clear picture of the Alphabet Corporate Life Cycle (Mature Growth phase). The second step was to attach the “utopia” CEO for this phase (Mature Growth) and to examine if narratives (from Annual report) from the current management team are in sync with the narrative of the “utopia” CEO.

As a result, Alphabet is a well-managed company which should expand its products, keeping at the same time the operating margins high and stable even with high reinvestment rates. It is obvious that good times of high growth are back but should keep his competitive advantage, either from high capital expenditures, which will expand the infrastructure and the data centers or with the appropriate balanced between revenues and operating expenses (internal efficiency) that will keep operating margins high and stable. Thank you.

Furthermore, you can check:

My personal blog: https://bluehorizon-invest.com/

My Valuation work on Amazon.com: eanagnostou90.gumroad.com

To support my work with donation: https://ko-fi.com/anagnostouevan

My Patreon Page: https://patreon.com/anagnostouevan

Ko-fi

Buy Anagnostou Evan a Coffee. ko-fi.com/anagnostouevan

Become a supporter of Anagnostou Evan today! ❤️ Ko-fi lets you support the creators you love with no fees on donations.

Already have an account?