Trending Assets

Top investors this month

Trending Assets

Top investors this month

Economic Update

Stocks opened lower but have since clawed back some of those losses. Debt ceiling negotiations have continued for another day without a deal. Talks on Monday were described as productive, but there is now just 1 week left to reach a deal before a potential default on June 1.

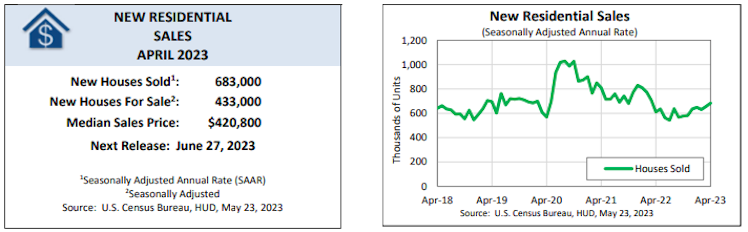

For economic data today, new home sales unexpectedly rose 4.1% in April to annual rate of 683,000, the highest level since April 2022. The prior was revised down to 656,000. The report showed the median sales price was $420,800, down 8.2% from the previous year. The report also showed a home supply of roughly 7 months at current sales rates.

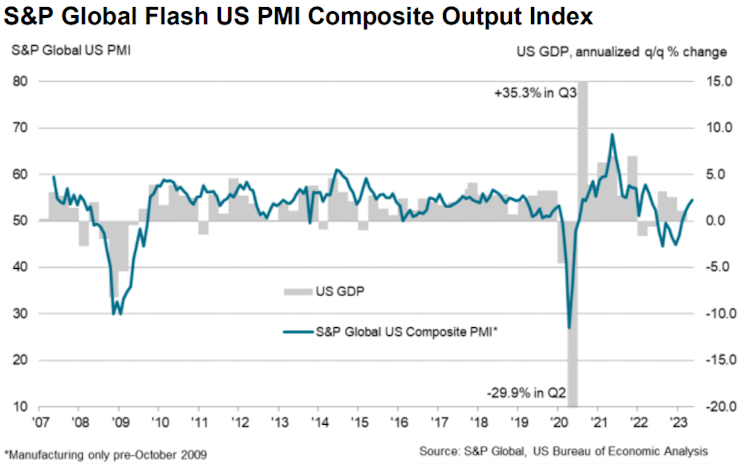

The May flash reading for the S&P Global U.S. Services PMI rose to 55.1, the highest level in 13 months. The Manufacturing PMI fell to 48.5, back into contraction territory and the lowest level in 3 months. The Composite PMI was 54.5, also the highest level in 13 months. Overall, growth output seen in May was the fastest in over a year.

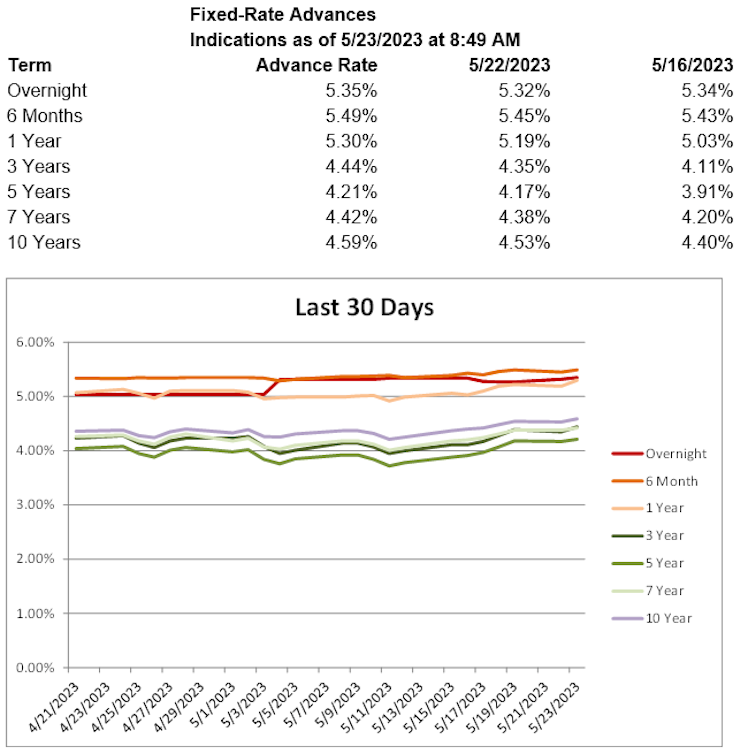

Treasury yields are flatter, with the 2-year T yield up 4.1 basis points to 4.36%, the 5-year T yield up 0.6 basis points to 3.77%, and the 10-year T yield up 0.2 basis points to 3.72%. Advance rates are higher throughout the curve today.

Already have an account?