Trending Assets

Top investors this month

Trending Assets

Top investors this month

Today $ALLE Is Boring But Tomorrow It Might Be Exciting

Doors & locks have been around for thousands of years as a valued tool to maintain our privacy and protect our personal property. Allegion is a company that focuses on access control security products and solutions, with their brands sold in 120+ countries.

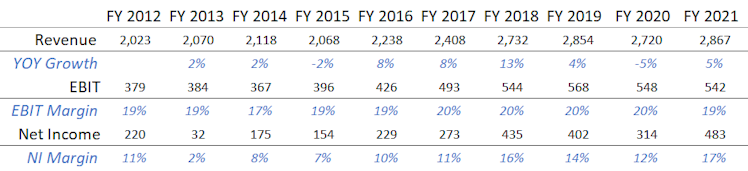

Allegion is a notable player in their end market but it has been such a boring investment the last few years. Tepid revenue growth and little evidence they are on a path to sustainable margin expansion. Over the years they have reduced share count and reduced debt but what will excite investors moving forward?

Adoption of Smart doors & locks should be the catalyst for margin expansion. We have a history of really steady margins, essentially 19-20% EBIT margins every year. Smart doors & locks introduces the possibility to layer on high margin recurring software revenue to the existing business.

Allegion recently completed an acquisition from $SWK for their commercial door division, which includes ~ 130m of annual recurring service revenue (recurring revenue is the very thing that would make Allegion an exciting business).

$LTCH has done a great job of highlighting the value proposition of digitizing doors for property managers and residents alike. I think it's possible to look at Allegion today & co-opt the Latch investment thesis. At their core $ALLE is hardware company trying build out/acquire software while Latch is a software company trying to build hardware or partner with hardware producers.

There are a number of macroeconomic headwinds facing the company but from a historical perspective the company is trading at a low valuation. If you believe in the potential of smart doors & locks then Allegion may be an attractive way to bet on the continued growth of the Smart Home/ Smart Workplace.

X (formerly Twitter)

Chamath Palihapitiya (@chamath) on X

My newest SaaS investment: $TSIA

We just announced this morning that $TSIA is merging with @latchaccess and taking them public. This is the “???” from the tweet below.

One pager is attached.

Already have an account?