Trending Assets

Top investors this month

Trending Assets

Top investors this month

The New Era of Nicotine

Is it weird that the best investment of all time is now practically universally ignored?

A single dollar invested into tobacco companies at the turn of the 20th century would be worth over $7 million today—an annual compound return of over 14 percent for over a century. Nothing else comes close.

But now, with the rising influence of ESG, the amount of available capital willing to invest in the industry continues to shrink, and major financial institutions, controlling trillions of dollars, are leading the revolt. With new mandates to avoid sin stocks, they’ve sold billions of dollars worth of related equities, driving prices down to significantly lower multiples.

Along with abysmally low investor interest and sentiment, the public is very aware of the health consequences of combustible products, and governments have sprung into action with heavyhanded regulation. Headlines and pundits continually tout that the tobacco industry is doomed.

Are they correct?

I don’t think so, and I believe there is compelling data that explains why. In this article, I aim to clear up a few things:

- Are cigarettes a thing of the past?

- The new generation of nicotine products

- The great re-nicotization

- Stakeholder perspectives

- Future growth and profitability

Let’s dive in!

Are cigarettes a thing of the past?

Cigarettes are cheap, easy to make, high-margin, reliable, have a large total addressable market, and create loyal, repeat buyers. They’re nearly a perfect product. But there is an obvious flaw. The well-known health consequences of using combustible products aren’t just bad for users—for producers, there’s a clear downside in the fact that the most ardent customers, on average, live shorter lives and thus can’t keep purchasing the product.

So are cigarettes going away?

No.

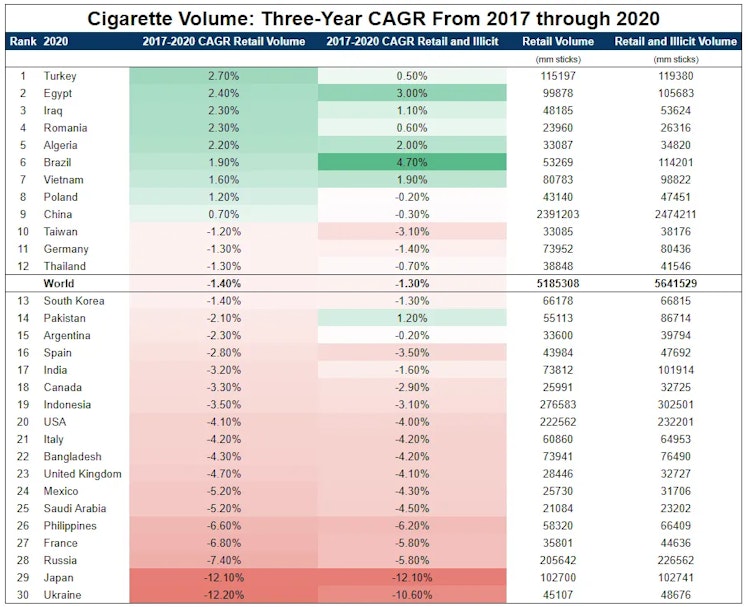

Cigarettes will be a thing of the past, but not yet—volumes aren’t falling as fast as people think.

Retail sales do not capture illicit trade, nor do they cover locally manufactured or nonmachine–manufactured products such as bidis/beedis (India) and papirosy (Russia).

These numbers are for 2017-2020, and fluctuations are to be expected. For example, COVID lockdowns bolstered volumes for many countries, despite having experienced more substantial decreases prior, while other countries experience accelerated declines. Also, the first half of 2022 has been notably impactful for volumes in the U.S. (one of the most lucrative individual countries), with total volumes estimated to have dropped 7.5% year over year, thought to be primarily caused by higher gas prices leading to fewer purchasing trips.

But even volume declines haven’t been disastrous. Price hikes have largely offset cigarette volume declines, allowing ongoing, often growing, profitability. I believe major operators will continue to produce impressive returns from their cigarette brands. But eventually, that parade will come to an end.

With that said, this is only part of the big picture.

Keep reading the full article by following the link below:

invariant.substack.com

The New Era of Nicotine

Headlines and pundits continually tout that the tobacco industry is doomed. Are they correct? I don’t think so, and I believe there is compelling data that explains why.

Already have an account?