Trending Assets

Top investors this month

Trending Assets

Top investors this month

Book me in

Low price-to-book stocks outperformed the market. But there’s a catch.

•••

Walter Schloss, a famed value investor, was well known for buying stocks that traded far below book value. “I really have nothing against earnings except that, in the first place, earnings have a way of changing… I find it more comfortable and satisfying to look at book value.” Thanks to this strategy, Schloss returned 21% a year, on average, for 28 years—an incredible result. So, have low price-to-book (PB) value stocks outperformed? The simple answer is yes. But should you sell everything and buy low PB stocks? That depends on whether you want outperformance, can handle volatility, and can stick it out through the cycles.

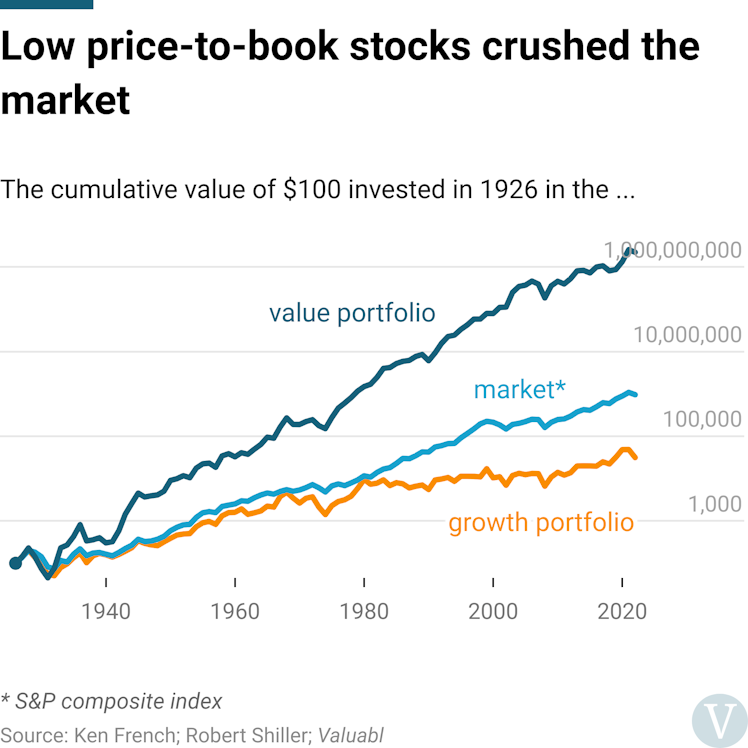

A simple equal-weighted portfolio of low PB stocks outperformed the market. Consider you built a portfolio of the bottom 10% of American stocks arranged by their PB ratios, and you rebalanced this each year. From 1927 to 2022, this portfolio—I’ll call it the value portfolio—compounded at 19% a year. A $100 investment back then would have become $2.2bn in 97 years.

That is a far better result than the market, which grew at 10% a year. It’s also miles ahead of the opposite strategy, which I’ll call growth, in which you bought the most expensive 10%. That low-PB strategy was, in effect, what Schloss did. But he operated when it was hard to get company data. If you could get the data, though, that approach was much less work than many other sophisticated strategies. And you likely would’ve done much better.

Still, you needed the gumption to bear gut-wrenching volatility. While the value portfolio produced killer returns, it was the most volatile. The standard deviation of annual returns was 43%. That’s 13 percentage points higher than the growth portfolio’s volatility and 24 percentage points more than the market’s.

For most non-robots, it would be difficult to handle this return whiplash. An incredible 205% return in 1933 was soon followed by a life-questioning 59% loss in 1937. But if you could stick it out for the long run, the value portfolio was the way to go. Its Sharpe ratio, calculated as the annual extra return above bonds divided by the volatility, is the highest of the three portfolios. With a 21% average excess return and 43% annual volatility, the value portfolio’s Sharpe was 0.5. That’s higher than the market’s 0.4 ratio and much better than the growth portfolio at 0.2. Indeed, the growth portfolio was a stinker. Not only did it give much worse returns than the market, it also had higher volatility.

Still, the value portfolio’s outperformance was cyclical. It didn’t always beat the growth portfolio or even the market. Over that almost century, the value portfolio underperformed the market on a ten-year basis three times. First, in the 1950s and ‘60s. Then again, early in the ‘90s. And most recently, it underperformed since 2015. As with volatility, cyclicality is challenging to handle. Well-meaning investors might abandon hope and sell their value stocks only to see them take off.

Stay the value course. It works.

“The thing about buying depressed stocks is that you really have three strings to your bow: earnings will improve, and the stocks will go up; someone will come in and buy control of the company; or the company will start buying its own stock and ask for tenders.”

— Walter Schloss

•••

This essay was originally published in Valuabl. Valuabl is a twice-monthly newsletter with expert financial analysis in a straightforward style. Subscribe here: https://valuabl.substack.com/

valuabl.substack.com

Valuabl | Edmund Simms | Substack

Curated financial analysis, economic commentary and investment ideas. Helping you make sense of markets and find undervalued stocks. Click to read Valuabl, by Edmund Simms, a Substack publication.

Already have an account?