Trending Assets

Top investors this month

Trending Assets

Top investors this month

High-Energy (Mining?) Tuesday

ICYI - here's a rough transcript of my High Energy Tuesday spaces; many thanks to two of my favourite Twitter friends for graciously hosting me, so I could talk about mining & metals in what is normally an energy spaces!

Including source links to some of the info I presented.

I have been on twitter a long time & I have learned - having a Twitter account is like being a politician - you will never make everyone happy, no matter how hard you try – personally I have just given up.

I will say, this app continues to reaffirm my faith in humanity much more often than it causes me to doubt it.

However, a word to the wise, there are far more “bad actors” on this platform than most realize. A healthy dose of skepticism will serve you very well.

Some of these bad actors can be really condescending & rude -- and it’s important you’re aware why they use this tactic:

They want to intimidate you, then you are less likely to question them and just assume they are an authority on the matter.

Others can be very charming, you might even consider them a friend, but remember -- Ted Bundy was charismatic too. A serial killer gets his victim in the car, either by force, or by charm.

I once heard a former US President speak, and he mentioned something that always stuck with me:

He knew what he did NOT KNOW and was not afraid to admit it.

By surrounding himself with experts that knew better than he did, he made better, more informed decisions – and that’s what I try and do myself here.

I am incredibly fortunate to have a small circle that I speak with daily – every one of them brings a different perspective– but most importantly, they are wonderful people. This can be a tough gig, and some days you really need friends that can empathize or laugh with you, or someone you can bounce ideas off of, and know that their answers are in your best interest.

I strongly suggest people consider forming a circle of friends that will tell you what you DON’T want to hear --in a way that’s acceptable to you – because as I have often said, echo chambers do us more harm than good.

I have seen that happen repeatedly here, and I think it’s far too easy and comfortable for people to just seek confirmation bias – because it’s upsetting to think you’ve made a poor decision, or to think that this thesis you’ve held a long time and firmly believed in could have been wrong…but if you’re presented with facts that disprove your theory, it’s only going to harm your bottom line if you’re too proud to consider them and change course.

I believe that any success I have had in the junior arena over the past few years is very much thanks to many of the people that I have met here; it is - 100% - nothing that I could have accomplished on my own.

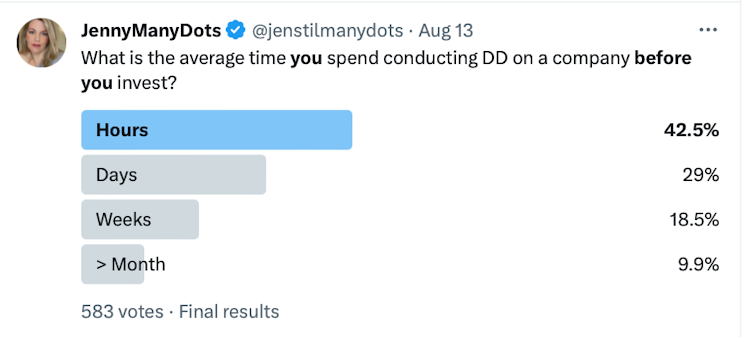

I ran a poll recently - asking people how much time they spend performing due diligence before buying, and the majority answered “hours” not “days” - well to me “hours” is FOMO.

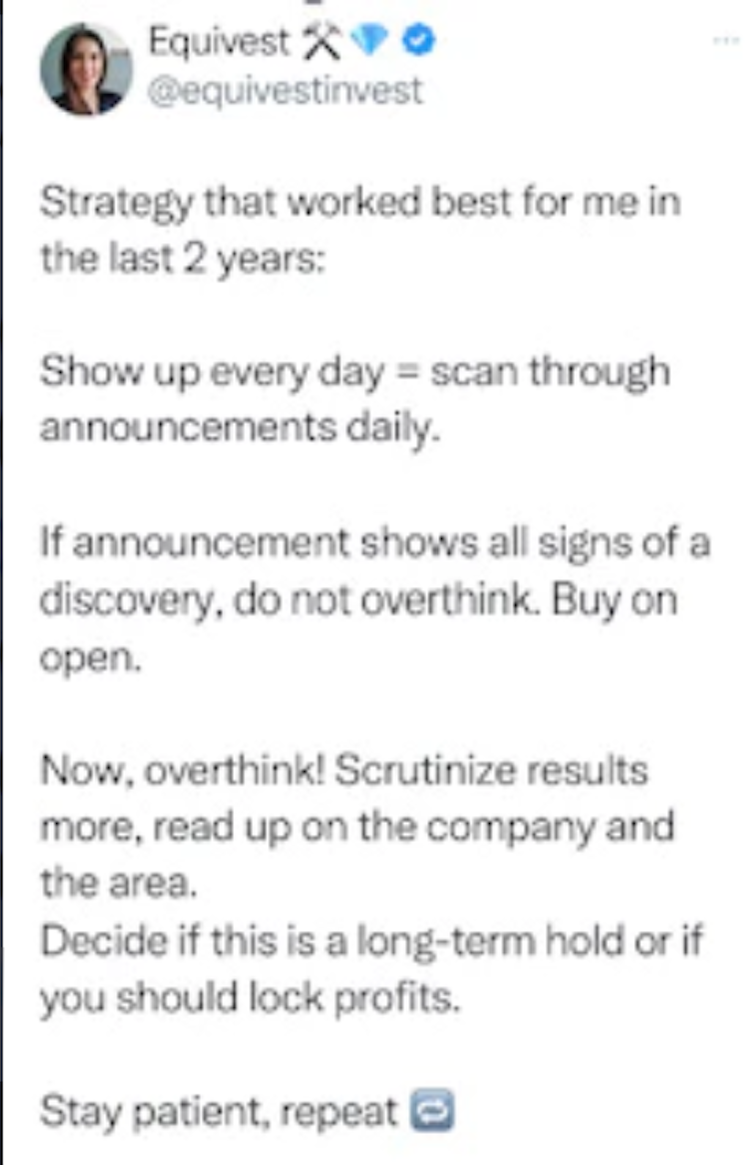

I am posting two tweets from accounts I respect – CEO Technician and Equivest. Their views seem to oppose each other, but both approaches are worth considering.

As CEO Tech said, I need to practice more JOMO (the joy of missing out) because as much as I wish, I don’t have the dry powder to buy everything I like – nor should I.

Equivest mentioned she doesn’t overthink and will buy on the open if the announcement shows the signs of a real discovery – and THEN you can scrutinize and decide if it’s a long term hold, and maybe take some profits along the way – which is exactly what I did with BAY.

Some may have seen my tweets in the last couple weeks about Aston Bay. I was incredibly lucky that worked out for me as a short-term trade; it wasn’t my first “FOMO” trade and I am sure it won’t be my last -- but normally I am much more cautious about tweeting those names, because if I don’t know much about a company then I shouldn’t be talking about it publicly - so I can understand why I faced some judgement over that.

Hopefully I can atone for some of that sin by sharing why I think I made a mistake, regardless of any profit that I luckily made:

If you don’t properly research a company yourself, it’s far too easy to listen to what complete strangers are saying and make your decisions based on that.

Please allow me again, I just want to highlight the word – “strangers” – if you haven’t met someone in real life and they are an anon account, I don’t care if they have 10,000 followers or 50,000, you really need to consider someone’s motivation for being here – I can’t state that enough.

I NEVER buy or sell just based on what I am seeing on Twitter and chat boards, and I didn’t do that with Aston Bay -to be clear. I monitor unusual volumes to see if anything interesting is happening out there (junior mining hub and CEO.ca are great sites for that – you can filter by exchange, share price, market cap etc and see the market movers of the day).

After the BAY press release stating they had made a significant discovery, I researched the management and felt that was a strong enough case to take a position fairly quickly. However - I did NOT research former drill results, the history of the stock, or the jurisdiction – and those are all incredibly important aspects that I should have.

I am out for now and will take the time to properly research the company and might buy back in, if I feel I have built enough personal conviction to do so. If I miss out on another move in the short-term, I’m okay with that --because if it’s what some are suggesting, then there will be time to add as it moves up.

The one good thing that I loved about Aston Bay’s story – the junior mining sector has been dead for a long time. Financings are at a seven-year low, sentiment has been terrible for a good two years it seems, and it needs to be reinvigorated with an exciting story or two. So if BAY works out to be that, then I think it’s a wonderful thing.

CEO Tech recently hosted a space with Luc Ten Have and they made some great points I wanted to mention, for those that didn’t have a chance to catch it:

- regarding ‘paid marketing’ in particular - which I have always been a little suspicious of myself, some promo people, to be honest, are a little bit like snake oil salesman - but NOT ALL of course.

- As Luc mentioned, these companies have no income, they only finance by issuing more paper and their stories must be told. They are not COCA COLA. They don’t have a product for sale at the grocery store to provide revenue to grow. It takes a lot of money to drill, and they have to raise it somehow.

Not all promotors out there will tell an honest story and that’s one of the things that gives the junior mining sector a bad name.

There are plenty of promo people on discussion boards, here on Twitter, or on CEO.ca, as well as a few questionable newsletter writers…

I know we all want to believe everyone has good intentions, but unfortunately that is not the case. I find it really frustrating to see the trust people place in some of these sources – because it’s often not deserved. I can’t say it enough – it’s so critical people do their own research and verify facts – particularly management’s track record.

I’m a big fan of Ian Cassel from the MicroCap Club, and he tweeted the other day that if you don’t believe that management is important when investing in microcaps, just wait a little longer, because you will. Investing in small illiquid companies is an art-form because you are investing in people and I couldn’t agree more.

My best returns have almost always come from reputable people with a history of success and I know Rick Rule has said the same thing. Luc said he considers insider buying a form of promotion and I place a lot of weight on how much skin management has in the game.

HOWEVER, I think it’s most important to watch insider SALES and this is a debate that I have had with people who say management needs money to buy a house or a car – well, do five of them at once? And exactly at the moment that a share price peaked? Again, microcaps in mining are different here than oil and gas majors, where you see a lot more equity-based compensation.

Checking an insider’s history beyond just recent transactions that they have filed is super important IMO. I often see a pattern – share price performance is correlated to insider transactions and sometimes you need to check management’s insider history at prior companies and that means looking back a few years. Surprisingly, this only takes a few minutes but if you make it a habit, I guarantee you will see why it’s a must for me.

Luc was telling CEO Tech that when investing in junior miners, he thinks about how much he can stand to lose, rather than how much he stands to gain - and I think that’s a terrific approach.

I have always tried to make it clear that these penny stocks can easily go to pretty much zero, and I have had the misfortune of being one of the lemmings that falls off the cliff with all the others.

These stocks are so illiquid, if you think it’s easy to get out with minimal losses – I can assure you 100% that it is not.

One of the things I do personally is lurk on CEO.ca:

- I don’t often comment because the trolls there are more vicious than here on Twitter and I definitely don’t listen to the cheerleaders, of which there are many. Instead I focus on the negatives mentioned and then look to disprove them and I’ve found that is very helpful in discovering red flags about a company.

Someone was asking me for a book recommendation the other day and I commented that for the last year or two, I just read as much news as possible from as many sources as possible.

I find that if I take as much as I can in from everywhere, it gives me a bit more of a balanced take on things and by doing that, I formed my own view of the outlook for certain metals.

(kind of like a steady diet of Fox News or just MSNBC, versus both of those and some centrist media too – you’re less likely to have an extreme or one-sided view).

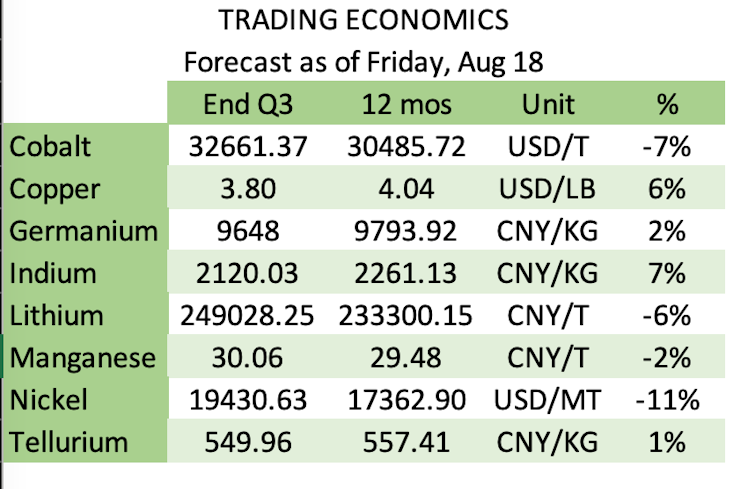

I had a look at tradingeconomics.com (great site for commodity pricing) to see if their forecasts aligned with mine and generally, they did (posting a table in the nest with their data as of last week).

So I’m changing my stance on a few things and what I say might upset a few people, but this is just my opinion from information I have gathered over the past few months. As we all know, commodities can be a wild ride and the big picture is constantly changing.

As John Maynard Kaynes said “when the facts change, I change my mind – what do you do?”

I think it’s a terrible idea to stick with your thesis when facts are trying to slap you in the face!

I am not ashamed to reverse my stance on certain metals, I would much rather do that than go with my pride and potentially take others down with me on a sinking ship.

Again – I am here to express my thoughts, and I am sure that plenty of folks will disagree with them, but I think it’s prudent to exercise caution on a few things…

I just want to share a quick story first from 2018 – when an exec from BHP was speaking at PDAC in Toronto and I think you will come to see the incredible irony here, if not maybe I need to explain it later:

Daniel Malchuk, President of BHP’s Operations said:

To talk about the future though, first we must understand the past. The history of mining and the history of the world are intrinsically linked.

And that history is not always a happy story.

Take the sodium nitrate mines of Chile, for example.

In the 19th Century, Chile was mined extensively for this mineral. At the time it was called ‘white gold’. (maybe some of you know what is currently referred to as ‘white gold’ and it’s not sodium nitrate…)

In the middle of that century, white gold mining became a huge part of Chile’s economy. Sodium nitrate mining grew to such an extent that it provided around half of the country´s income.

Chile had ‘white gold fever’.

Towns were built to support the booming industry. But the industry did not plan for the future or think about its context in broader society.

It did not keep up with technological and societal advances.

It focused only on the short term.

This approach was not unique to the sodium nitrate mines of Chile. Short term thinking has been endemic throughout the mining industry at times.

In the early 20th century, the future arrived. Scientists discovered how to make synthetic sodium nitrate through a chemical process. White gold no longer needed to be mined.

By the early ‘60s, the towns that supported sodium nitrate mines of Chile were abandoned.

The wealth created was temporary. The benefits for society of this incredible boom were lost.

A story to keep in mind, again that was a BHP exec at PDAC a few years ago.

I occasionally have a look at what CATL is up to - based in China, they are the world’s largest EV battery maker, manufacturing approximately 30% of global supply.

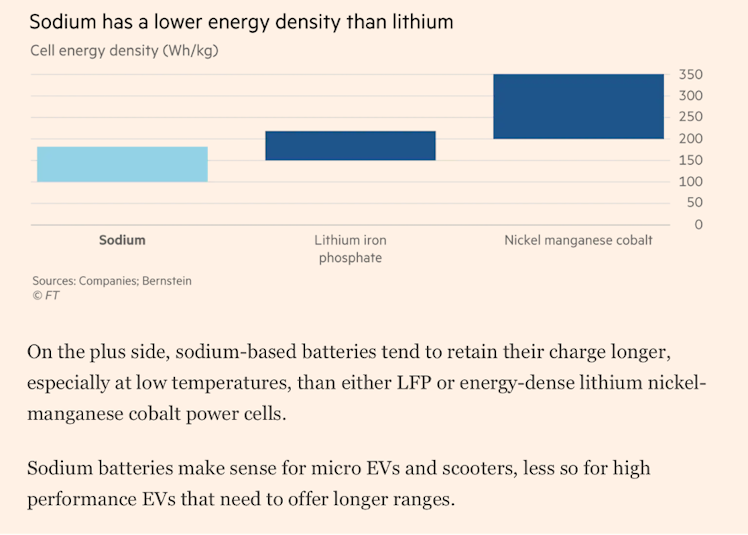

They currently seem to favour the lithium-iron-phosphate battery but the possibility of replacing lithium-ion batteries with sodium-ion should be monitored very closely.

Vanadium seems even more likely to be replaced than lithium - as sodium appears to be a better option for grid-scale energy storage. I joked to someone the other day that Rick Rule broke my vanadium when he mentioned Largo and VAND were his two top picks on BNN.

Initially I saw it as validation (because I was Vanadium Cassandra) that Ross Beaty, Robert Friedland, and then Rick Rule were all fans of vanadium but the fact is - technology is rapidly changing and more cost-effective & efficient solutions are always sought after.

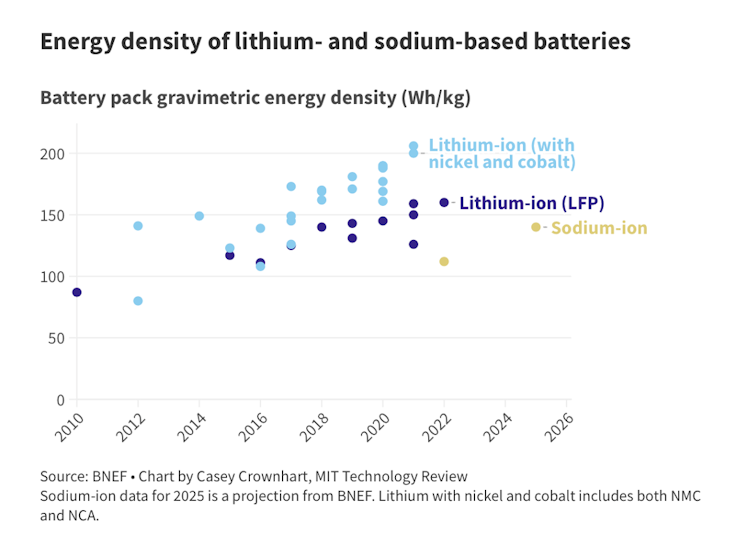

As lithium prices continued to surge throughout 2022, progress in developing sodium-ion batteries surpassed expectations.

Last November, CATL announced that their sodium-ion batteries are anticipated to power EVs in the future. They have discovered a way to use sodium cells and lithium cells in a single battery pack and are now prepared to mass-produce these “mixed” battery packs;

sodium battery cells are so similar to lithium ones – and I think this is a key point - that they can be made with the same factory equipment.

A little background for non-chemists like me, on sodium versus lithium:

There are six chemical elements – alkali metals - that make up Group 1 of the periodic table, lithium and sodium are two of them.

Sodium is the sixth most abundant of the elements, constituting 2.6% of the Earth’s crust – that’s a lot. Lithium, though also abundant, is considerably rarer, forming 0.007% of Earth’s crust.

Sodium currently sells for 1 to 3% of the price of lithium.

The extraction and processing of lithium can have negative impacts on the environment, including water pollution and depletion of resources.

Sodium, on the other hand can be extracted from seawater, which reduces the environmental impact of mining.

Sodium is less reactive than lithium, reducing the risk of fire and explosion – which we know has been a serious concern for lithium-ion batteries.

Sodium-ion batteries can operate at lower temperatures, while lithium-ion can lose up to 50% of their capacity when exposed to below freezing temperatures. Most people in Calgary would tell you, this is one of the reasons they have been hesitant to purchase an EV, as their performance during a cold winter remains questionable.

Batteries contribute significantly to the cost of an EV and sodium-batteries are approximately 20-30% cheaper than lithium-ion -- so such a change would significantly reduce the cost of an EV which has also been a barrier to adoption.

Someone asked me recently about concerns regarding energy density in sodium batteries.

CATL began large-scale commercial production recently of sodium-ion batteries that have an energy density of 200 watt hours per kilogram. To put that into perspective, the LFP battery cells Tesla used in 2021’s Model 3 Standard Range came in at around 200 watt hours/kg so the same.

For those that are skeptical of word coming out of a Chinese company like CATL – how about listening to the CEO of the world’s largest mining company:

BHP’s chief exec Mike Henry said he is confident we will start seeing sodium replace lithium for certain applications and that it would shave off the peak demand for lithium.

On July 27th, the President of BHP Australia addressed the American Chamber of Commerce in Australia and made it clear that BHP would continue to focus on the core minerals of the business - iron ore, metallurgical coal, copper, nickel and potash. Lithium was notably missing.

BHP doesn’t believe it can construct lithium mines at the same large scale and accompanying low costs that have made its iron ore and coal segments so profitable.

They had the same view going back to 2018, when they said they expected profits in the lithium sector to be hit as more supply came online in the wake of cheaper production techniques, saying “the available economic profit in that industry for the next couple of decades really isn’t there”.

And if you don’t believe CATL or BHP – how about the Australian government?

In July the Australian govt’s quarterly report stated that growing global output means lithium is in for a brutal price correction.

2024 will see a dramatic drop-off in contract value for Australia’s spodumene miners with prices declining nearly 40% year-on-year, and falling an estimated 20% further in 2025.

Lithium hydroxide prices in 2023 are forecast to be almost a third below last year’s average, and are expected to decline further next year before easing in 2025.

Unlike lithium batteries, the latest sodium batteries do not require scarce materials like cobalt.

Cobalt is mined mainly in Africa under conditions that have alarmed human rights groups.

The newest sodium batteries also do not require nickel, which comes mainly from mines in Indonesia, Russia and the Philippines.

Personally I have never been a cobalt bull –given the human rights abuses related to it, as well as its expense; battery makers have tried to decrease or eliminate it from battery chemistry for some time.

Perhaps more important to note:

The nickel market is facing a massive supply glut as surging Indonesian production continues to outpace demand.

In March 2021, Tsingshan (ChingShawn) – the largest nickel producer in the world, accounting for about 20% of the global market, announced a breakthrough in making nickel sulphate by converting nickel laterite ores to nickel pig iron, and then further to nickel matte, which is later processed into battery chemicals.

For those unfamiliar, nickel pig iron is a low-grade ferronickel invented in China as a cheaper alternative to pure nickel for the production of stainless steel.

The International Nickel Study Group is forecasting a supply-demand surplus of 239,000 tonnes, the largest in at least a decade - and a significant increase from last year's excess of 105,000 tonnes.

Writing this I was thinking about all of those IEA studies that focused on the increase in demand for nickel and cobalt, and again I thought how much better one is served by considering a multitude of sources rather than just one or two, that you assume are reliable.

I’m not exiting my vanadium, nickel, or lithium picks entirely at this point -- but I have reduced my position sizing for those commodities and would urge caution and suggest people monitor developments closely.

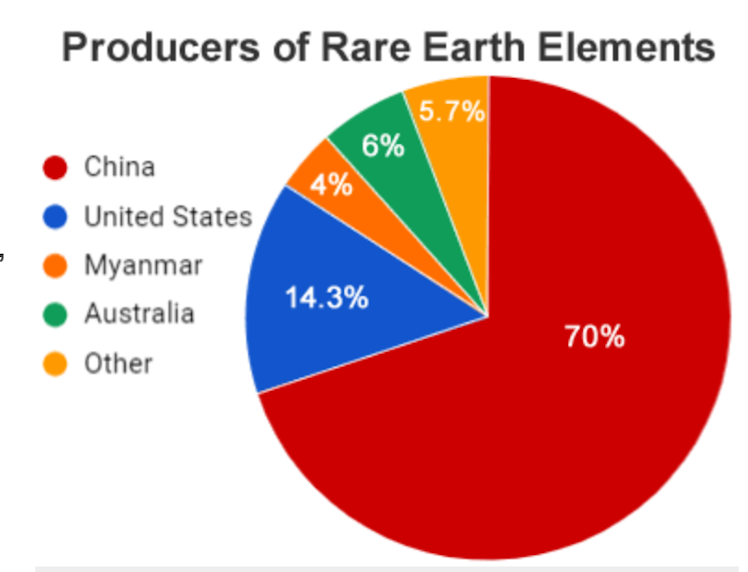

Rare Earth Elements (REE’s) – this is a crucial one people aren’t paying enough attention to.

I often tweet the acronym REEs and am asked privately what it stands for – an indication that people don’t have these niche metals on their radar. They aren’t rare in their presence, rather they are named as such because they are difficult to extract and process, even with today’s technology.

In early August, China started restricting exports of two materials- gallium & germanium - key to the semiconductor industry, as the chip war with the US heats up. These materials are used to produce chips and have military applications.

China produces 80% of the world's gallium and 60% of germanium - making it by far the largest player in the global supply chain.

$TECK is one of the world's largest integrated germanium producers. Germanium-bearing concentrates are processed at their integrated lead/zinc refinery in Trail BC – so yay if you own TECK – bonus rare earth exposure, beyond their copper assets!

REE’s comprise only 17 elements from the entire periodic table, and they play a critical role in national security, energy independence, environmentally friendly technology, and economic growth. Many advanced technologies have components made from REEs such as magnets, cell phones, fluorescent lighting, and batteries. I think almost everyone would be surprised to learn about the REE’s required to make your cell phone – you probably wouldn’t have one without them, and yet barely anyone can name a single REE.

If a single country controls almost all of the production, and makes a firm decision not to export, then the entire supply of a commodity can be quickly cut off. That is a dangerous situation when new sources of supply take so long to develop.

In 2010 China significantly restricted their rare earth exports. That was done to ensure a supply of rare earths for domestic manufacturing and for environmental reasons. This shift by China triggered panic buying, and some rare earth prices shot up exponentially.

Notice the outlook for some rare earth metals in the trading economics table that I posted and you will see indium holds some promise. Most indium is used to make indium tin oxide (ITO), which is an important part of touch screens, flatscreen TVs, and solar panels. This is because it conducts electricity well, it bonds strongly to glass and it’s transparent – so indium is likely one commodity worth looking at and so are several other rare earth’s.

Am I still a copper bull? In the long term, most definitely and I continue to see headlines that support my view. I wrote a post on CommonStock called Copper & GoRozen Greatness –one of my favourite GoRozen research reports was their 2021 - The Problems With Copper Supply - and copper remains their favourite base metal investment (mine too)!

Copper’s widespread applications — from homes and manufacturing to electronics, power generation, and transmission as well as it’s expected role in the energy transition, primarily EVs, and renewables, solar panels, and wind turbines in particular - are more copper-intensive than their traditional counterparts

I know that Goldman Sachs has been a commodity permabull, particularly regarding copper – but they were calling for global copper stocks to be potentially depleted by august.

SMM China Metals data showed that as of Friday, copper inventory across major Chinese markets hit the lowest for the year.

Looking at the supply-side:

Anglo American cut its production estimates for the year because of deteriorating grades at their Chilean mines.

Codelco is the world’s largest copper producer – and is said to be at risk of insolvency with production at a 25 year low. Over the past five years, Codelco’s copper production has dropped 17% and is expected to keep falling until 2025.

Companies spent much of the past decade expanding mines to guarantee shareholders a better return in the short-term rather than finding and developing new copper projects...one of the reasons I am bullish on junior copper exploration companies! We are in dire need of new discoveries.

I am constantly seeing headlines about majors looking to grow their copper portfolio, in May it was announced that Glencore was looking to expand their Peru copper mine at a price of $1.5B USD

I’m seeing increased investment by Chinese and Japanese companies, particularly in Peru – I will talk about jurisdiction shortly.

Looking at the demand side of the equation:

Even if China’s property market falters, we are still looking at a significant increase in that country’s copper demand from growth in their renewable and EV sectors.

Copper demand from India was up 27% in 2022. The per capita copper consumption in India is expected to increase from the current level of 0.6 Kg to 1 kg in coming years.

The average per capita copper consumption in the world is 3.2 kg. If India’s moves towards the per capita copper consumption levels in the rest of the world, India’s copper market has the potential for significant growth. India is forecast to be the fastest-growing economy in the G20.

Regarding Peru - a favourite MinTwit saying of mine is “politicians come and go, but the rocks will always be there”

At a conference back in October, BHP CEO Mike Henry said the company is ready for a strategic shift out of its geographical, advanced-economies comfort zone into “tougher jurisdictions” as part of its plan to increase exposure to commodities such as copper.

Henry said he was confident the company could manage the risks of investing and operating in politically volatile countries.

In his speech at the VRIC, Ross Beaty said “buy when there is blood on the streets because that’s when the real money is made.” It sounds awful if you take that phrase literally but he was correct in that when countries are upended by political chaos, equities are obviously cheaper and if and when things return to normal, then you can see incredible gains.

I don’t believe any jurisdiction is “safe” so to mitigate risk, I personally construct a geographically diversified portfolio.

I am pretty keen on Peru right now, as they are working hard to remove roadblocks that hinder or delay mining exploration and development. Mining investments there are on the rise and June saw a 9.6% increase compared to May.

The first half saw mining investments in Peru reach $1.8B and the hope is that by year end, that figure reaches $4.7B.

They are currently on their sixth president in two years, so political chaos is almost the norm there.

I think it’s important to investigate some of the jurisdiction risks at the level of the local community, because those relationships are of critical importance – if you don’t have local support it’s very difficult to move forward.

Perhaps the saddest situation is in Ecuador, which has now surpassed Colombia in gang-related violence. After the first election round this past weekend, two candidates will now face a runoff election on October 15th.

I hold a few investments in Ecuador and though I am obviously concerned about the conditions there, it’s been interesting to note the activity that continues to take place.

Luminex Resources began negotiations back in February, 2022, and announced yesterday that it had reached a mediated agreement with informal miners at their Condor gold project in southeast Ecuador.

Last week Dundee Precious Metals completed an “investment protection agreement” with the Government of Ecuador, granting them tax stability and certain tax incentives, as well as legal protections including stability of the regulatory framework, and resolution of disputes through international arbitration.

Obviously these agreements can take a great deal of time and situations are complicated – but business can still move forward despite the instability.

As GoRozen says “commodities may not seem to make sense for long periods, but time after time they eventually do. The risk is always that investors become frustrated and get rid of their allocations at exactly the wrong moment.

When I asked DS and Jleqc if there was anything in particular they would like me to cover tonight, they said “anything that excites me”...

There’s always something that does, but I thought I would throw a couple names out there to put on people’s radar. I won’t say much because I really want people to do some digging themselves, and not rely on anything that I say.

There’s a few interesting stories worth looking at and again, I like high risk/high reward so please bear that in mind and DYODD and never invest more than you can afford to lose.

Here’s just some names people might want to check out:

The first one I will mention is Aurania, ARU.v.

Even if you aren’t interested in buying, and again – this one is in the jungles of Ecuador – can’t get much riskier than that, but wow – definitely the most interesting story I have ever read in my time here.

I wrote about it on CommonStock if you are interested in reading my piece, but here’s the skinny on it:

Dr. Keith Barron and his team discovered the Lundin’s Fruta del Norte deposit in 2006 – his company Aurelian saw its share price go from $0.40 to FORTY FOUR dollars.

Dr Barrons is on the hunt for a second Fruta del Norte (on the same trend with a larger land package), and he is hoping to provide shareholders with a repeat.

The story involves ancient maps from the Vatican’s library, the sinking of the SS Central America which carried about $3B worth of gold (today’s dollars) from the San Francisco mint, how to survive a giant centipede bite, and the author of a book about the infamous Bre-X story – which was a basis for the movie Gold with Matthew McConaughey. If you haven’t seen that, I have about 4x now and would recommend watching it.

Another company of interest to me is Cordoba Minerals $CDB.V.

Cordoba is exploring in two world class porphyry copper belts, Arizona & Colombia.

(Ivanhoe Electric/Robert Friedland – 63.27% and JCHX, a mining construction company from China – 19.99%)

It’s tightly held and retail only owns about 16%.

Their Perseverance Project Lies on the Arizona Volcan Arc, a trend that hosts

Freeport McMoRan’s Bagdad copper mine

Origin Mining’s Mineral Park mine

Rio Tinto’s Resolution Project

I have been interested in this one for awhile, but recent insider filings finally made me a buyer.

One I am not sure about, I have a small starter position and am still researching but if you’re looking for exposure to some rare earths, Namibia Critical Metals might be worth a look – that’s NMI.v. Again I like to see some big name backing, and they have a partnership with a large Japanese company (JOGMEC).

The last one, and I have mentioned this one before is:

Camino Minerals, $COR.V

I recently tweeted about calling CEO’s or management of a couple of my duds. I had a call with Jay of Camino around the same time and hope no one thought I considered it a “dud” because it’s probably my favourite holding right now.

I spoke with Jay for 90 mins earlier this month and I was actually hoping that my enthusiasm would be tempered but that was not the case…

I was aware that Jay had co-founded Lithium Americas and knew he had worked with, and continues to work with Robert Friedland but I didn’t realize they had been friends for over 20 years

Jay has also worked closely with Dr. David Broughton of Ivanhoe Mines (Dr. Broughton is currently an advisor for Aston Bay).

…nor did I realize that prior to Lithium Americas, Jay was the President and CEO of Jinshan Gold Mines where he led the development of China’s second largest producing gold mine.

One of the things I like about Camino is the fact that they have three properties of significant potential and though they are all in Peru, they are each uniquely different and located in different parts of the country.

I invested in Camino prior to their signing on with Nittetsu for a JV on their Los Chapitos property, but for me that JV de-risked the project significantly, as drilling and exploration are now funded for the next three years.

I have looked at several companies in Peru and noticed almost all have struggled under the weight of Covid and political chaos the last two years. Many are cheap and I believe Camino is extremely undervalued.

One of the reasons Camino’s share price also suffered, and Jay was apologetic for this, was due to the fact that their largest shareholder – Ken McNaughton was involved with Pretium Resources as their Chief Exploration Officer. In March of 2022, Newcrest acquired Pretium Resources - including 100% of their Brucejack operation – one of the highest-grade operating gold mines in the world.

As some of the political chaos in Peru has subsided and Ken has completed the Pretium transaction, Jay assured me that they are fully focused on Camino and the development of Los Chapitos, followed by Maria Cecilia (for which they are in talks with other JV partners), and later Plata Dorada and potentially more acquisitions. Important to note as well that a lot of Camino’s permits have been granted which is always a big reason for delays.

Again please do your own research, I’m not a professional – but I always love hearing about new tickers and I assume others do too – so these are worth checking out and it’s up to you to decide whether or not you like them! If I have missed red flags, please don’t hesitate to share that with me…because I can’t say I am keen on losing money.

And that’s a wrap!!

TWEET ARTICLES/STATS:

Article from MIT Technology Review on why cobalt & nickel are being replaced or decreased;

Great articles from MIT technology review & NYT & FT

CATL New Product Launch

Sodium-ion batteries from CATL and BYD to be installed in mass-produced cars by Q4 2023

No lithium, no cobalt, no nickel, no graphite and not flammable –

CNBC: How Sodium Might Replace Li-ion Batteries:

SP Global: Emerging Battery Chemistries

the removal of cobalt is an "inevitable trend,"

"we should never underestimate this disruption."

Info about REE's:

SP Global on India:

Already have an account?