Home

Discover

Trends

Leaders

Sign up

Login

Signup

Trending Assets

Top investors this month

Trending Assets

Top investors this month

Fat Baby Funds

$26M

Followers

@fatbaby

05/14/2023

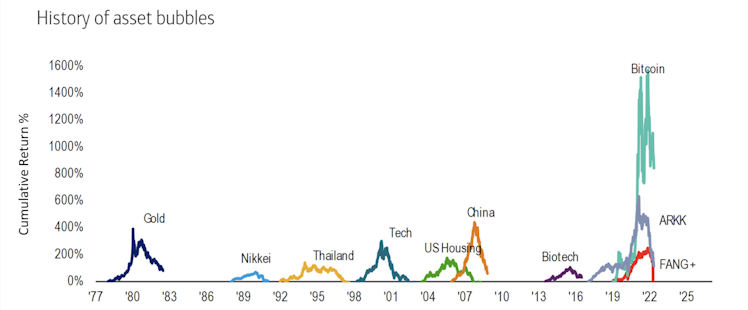

Bitcoin is off the map. A wild chart.

9

0

1

2

3

4

5

6

7

8

9

0

1

2

3

4

5

6

7

8

9

Fat Baby Funds

$26M

Followers

@fatbaby

Related

Join Commonstock

Already have an account?

Log in